Australian Dollar Forecast: Neutral

- The Australian Dollar has been undermined by an unfavourable disparity in rates

- While the RBA backed away from tackling inflation, other central banks have not

- A lower currency could boost the domestic economy but might import price pressures

The Australian Dollar went south after the Reserve Bank of Australia (RBA) blinked in the fight on wealth destroying high and volatile inflation. Their hike of 25 basis points to 2.60% last week is seen as dovish in light of persistent price pressures domestically and globally.

3rd quarter Australian CPI is due at the end of this month and the RBA said in their statement that they expect it ‘to be around 7¾ per cent over 2022’, well above their target of 2–3% over the cycle.

CPI has been above 3% since the 2nd quarter of 2021. Any notion of a ‘base effect’ or inflation being ‘transitional’ would come under scrutiny when wages that are tied to CPI are starting to flow into consumers’ back pockets.

Other central banks are entrenched in the affray to hose down inflation expectations to avoid them becoming embedded.

The Reserve Bank of New Zealand (RBNZ) stood firm in their battle to rein in inflation, hiking the official cash rate by 50 basis points last Wednesday to 3.50%, as anticipated.

The rhetoric from the Federal Reserve has been extraordinarily hawkish going into the weekend. The market is pricing in a 75 basis point hike at the next Federal Open Market Committee (FOMC) meeting in early November.

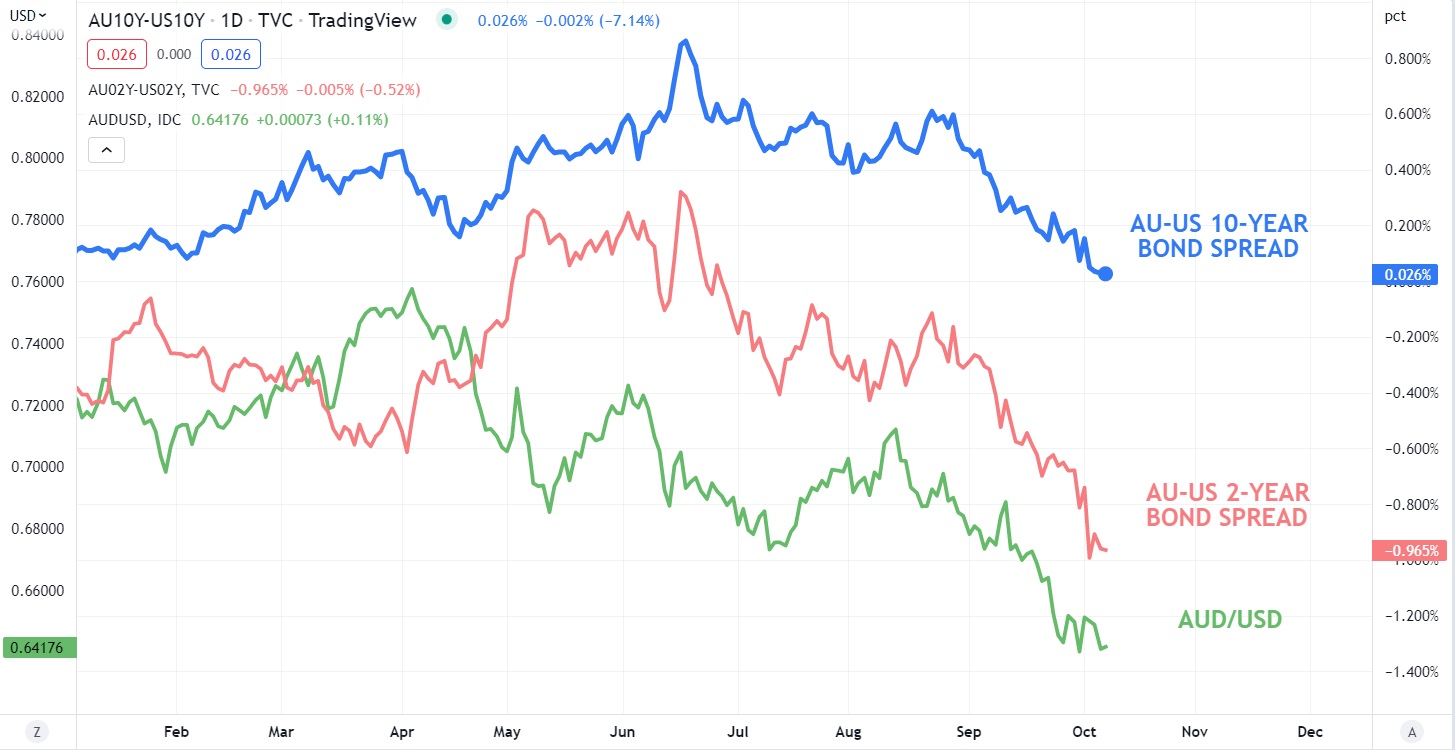

All this has seen yield spreads narrow in favour of the US Dollar more broadly but with the RBA less hawkish than other central banks, AUD/USD has sunk more than most.

AUD/USD AGAINST 2 ANS 10-YEAR AU-US BOND SPREADS

Domestically, the ‘pro-property prices must go higher forever brigade’ have been vocal in crying poor about the recent pull back in house prices across Australia.

According to CoreLogic data, Australian national house prices rose by 25.5% since the start of the pandemic. They have since declined by 5.5% since the peak that was made just before the RBA started their rate hike cycle in May.

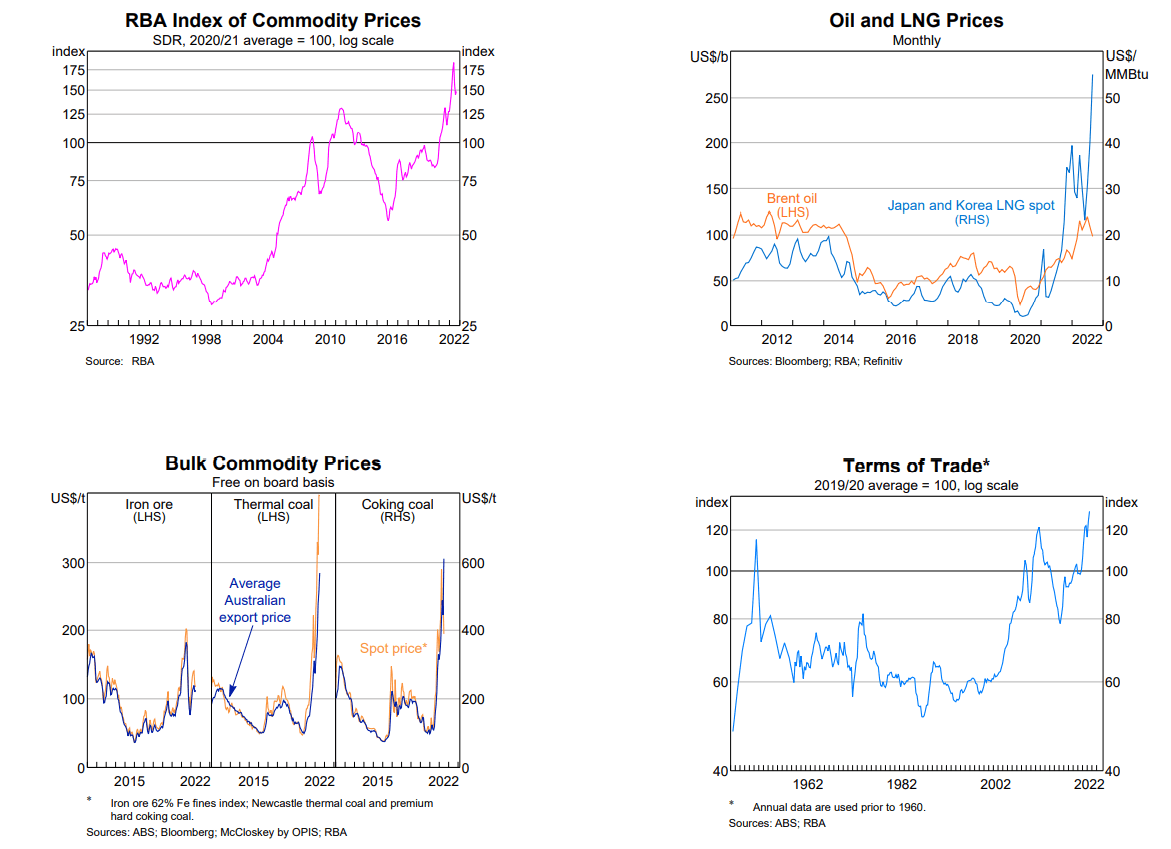

In the background, commodity markets continue to deliver a boon to the Australian economy with around AUD 10 billion being delivered each month.

The chart at the bottom of the page from the RBA paints a very rosy picture with Australian commodity prices and the terms of trade at elevated levels.

From this week, dividends of more than AUD 40 billion that was announced through the last earnings reporting season will be distributed. The ASX 200 could be aided by dividend reinvestment plans over this period.

Most of the worst news might be out of the way for the Aussie Dollar and with the embattled currency looking at 2-year lows further losses will come down to US Dollar movements.

--- Written by Daniel McCarthy, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter