Talking Points:

•he surge from Netflix on its earnings beat was washed out Thursday, and broader risk signaled casting off a bullish bias

•At the close of the two-day EU Summit, there is positive resolution for neither Italy nor Brexit which adds Euro and Pound weight

•Dollar is climbing as it takes advantage of counterpart weakness, Chinese GDP and Canadian CPI are key event risk ahead

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 4Q 2018? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Netflix Earnings Has Helped Signal a Shift in Speculative Biases

The Netflix earnings from earlier this week have played a particularly useful role for those active in the markets. For those trading NFLX shares and derivatives specifically the response to the corporate update, the market's course is no doubt frustrating. In after-hours trading immediately after the news hit the wires, the stock's price soared 17 percent. The next day, the anticipated bullish gap was in place, but there was no follow through to signal speculative momentum was roused. Then, through Thursday's session, further retreat would fully flush any remnants of the speculative charge the news had initially supplied. And, if the company's own stock couldn't take advantage of the encouraging development, it should surprise no one that there was little enthusiasm to spill over to the broader financial markets. Some may see this as little surprise as the broader market should theoretically find little strength in a single company's earnings report. However, for those that have been following these markets over the the past years, this lack of influence is surprising. There has been a bullish bias behind the markets for the better part of a decade; and on this charge, investors developed an affinity for earnings season and FAANG performance. As sentiment chugged higher, disappointing news was reasoned away while encouraging developments leveraged further rally. While the lack of response around this particular stock's reporting should only be interpreted so far, it certainly does show the markets are not set to respond to any and all positive news. What's more, the collective drop in risk assets this past session which pushed the Dow and S&P 500 back towards their long-term trendlines, the EEM emerging market ETF to a fresh low and an extension of the Yen cross index's slide suggests disappointing turns may find traction in markets. While we can take our pick for fundamental troubles, a more active global concern these past 48 hours arose out of the EU Summit.

S&P 500 Chart (Daily)

Euro and Pound Left to Suffer at the End of the EU Summit

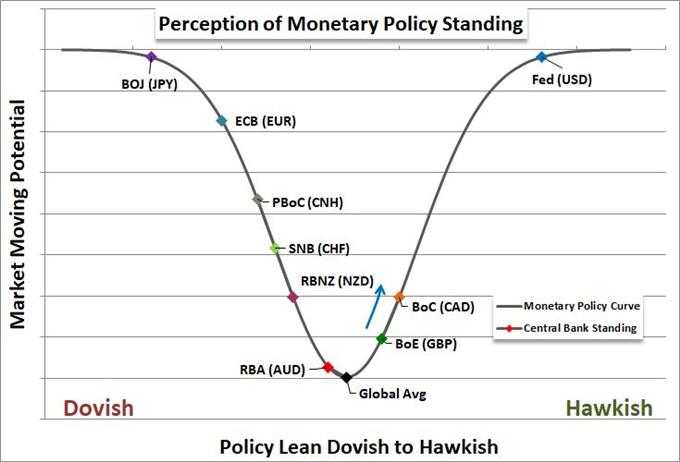

The two-day gathering of the European Union's leadership closed Thursday evening with a very distinct lack of progress on two key issues: the stand off with Italy over its budget and the impasse with the United Kingdom over its withdrawal from the Union. That does not doom either issue, its respective capital markets or currencies; but it does at least reset the clear countdown to a specific confrontation on these matters. While there were a number of issues no doubt addressed during the official discussions and on the sidelines, one of the key topics was the Brexit. Leaders and chief negotiators on both sides have suggested significant progress has been made and they expect a 'good' deal, there remains important points for which the two sides simply can't seem to find a breakthrough. After the Summit, Prime Minister Theresa May was once again encouraged by the discussions but said the EU's proposals for the border remain unacceptable. Sometimes there is speculative strength borne of complacency in fundamental ambiguity, but this is less likely to be the case with the Brexit situation. There a deadline to meet (March 29) and considerable work that needs to be done on both sides before that date *after* the draft agreement is made. As time marches on and they remain at odds, the Sterling will likely feel the pressure build. However, there will also be opportunity for newswire developments to charge short-term bullish interests along the way. As for the Italian budget stand off, the market will determine the level of tension on a situation that is unlikely to find a happy resolution in the near term. With the Italian-German yield spread at a five-and-a-half year high (over 320 basis points), we know where to look for tension on the Euro.

Italy-Germany 10-Year Yield Spread Overlaid with EURUSD (Inverted)

Dollar Leverages its Schadenfreude to Override Budget and Rate Concerns

If both the Euro and Sterling are struggling with systemic risks, where is global capital going to flow? While the Japanese Yen is the third most liquid currency and a speculative target when risk trends slide, the US Dollar stands to draw much of the benefit through its sheer size alone. It certainly has a litany of systemic issues to deal with, but at the moment, they are not as pressing as the global need to find alternatives to the troubled European currencies. The Greenback's strength is not universal - a quick look to USDJPY signals the Yen is leveraging more of the short-term safe haven appeal - but capital flow motivated by liquidity can overwhelm most other considerations. While the DXY rebound tracks the USD-favorable EURUSD and GBPUSD range moves, I am not confident in the currency's ability to leverage the next key break - much less the trend that we would look for thereafter. On the Dollar's own docket, the St Louis Fed President James Bullard attempted again to throw cold water on rate expectation again when he said current levels of interest rates were appropriate and further hikes could add to recession risks. On the more systemic side of things, the President's recent remarks that department heads should be prepared to cut spending 5 percent across the board adds another hurdle to growth as the relentless growth in the deficit threatens the country's credit rating and financial market calm. Keeping tabs on the correlation between the Dollar, 10-year US Treasury yield and S&P 500 would be wise.

GBPUSD Chart (4 Hour)

The Caveats for Market Movement in Key Event Risk Ahead

Looking at the economic docket for the final trading day of the week, there is plenty of event risk to draw attention. Yet, just because the market pays attention doesn't mean it will necessarily respond with significant movement. Both the heads of the Bank of Japan (BoJ) and Bank of England (BoE) are due to speak, but neither will likely tap the nerve that would elicit a strong move from the Yen or Pound respectively. The Euro-area and Italian trade reports seem to speak to the trade wars and Italian financial pressure that we have seen stirred so recently. However, these indicators are likely to fall short of the influence needed to systemically alter the established expectations. In terms of sheer headline potential, the Chinese 3Q GDP and the host of September figures (jobless rate, industrial production, fixed assets, etc) will command a considerable amount of news column inches; but its sway over the markets has been consistently drained. There is a well-founded concern over the veracity of the data whose readings are unrealistically restrained in month-to-month and quarter-to-quarter changes. It is possible that the Chinese authorities will allow for a significant change which would signal a sensitive market, but it is a low probability. In contrast, the Canadian consumer inflation report (CPI) is far more restricted in its influence, but it carries far more weight where it counts. With the NAFTA negotiations closed, the Loonie can once again focus on interest rate expectations. And with the markets pricing in another rate hike this year while the Bank of Canada (BoC) is due to determine rates next week, there is plenty to work with. We discuss all of this and more in today's Trading Video.

Probability of a Rate Hike by Year End (Overnight Swaps)

If you want to download my Manic-Crisis calendar, you can find the updated file here.