Receive the DailyFX US AM Digest in your inbox every day before US equity markets open - signup here

With US equity futures turning lower before the open in New York, the US Dollar has been able to claw back some of its losses onset by the first FOMC meeting helmed by Fed Chair Jerome Powell. Despite the FOMC hiking rates by 25-bps, the hawkish tilt in the Summary of Economic Projections proved to be less hawkish than what traders were hoping for. Elsewhere, after initially trading higher on the back of the Bank of England’s Monetary Policy Committee’s 7-2 vote to keep rates hold (two dissenters calling for a 25-bps hike), the British Pound has seen a round of profit taking after a strong week thus far. Finally, the news wire remains perhaps the most important source of event risk given the grace period for the Trump administration’s tariffs coming to an end tomorrow.

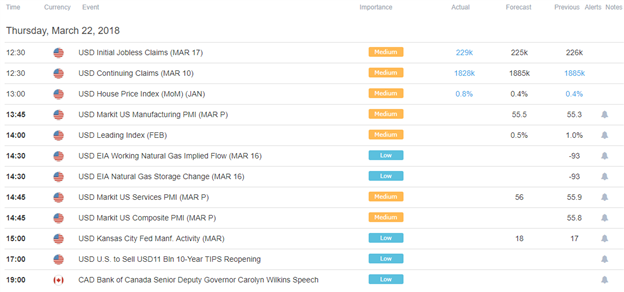

DailyFX Economic Calendar: Thursday, March 22, 2018 – North American Releases

The North American economic calendar will see its typical high volume flow of releases today, with the weekly US jobless claims figures already having been released (and still pointing to considerable strength in the US labor market). Later today, the February US Leading Index will be released, which is set to come in at +0.5% from +1.0% (m/m) – a sign that US growth momentum may be cooling. Similarly, the preliminary March US Markit PMIs will be released at 9:45 EDT/13:45 GMT.

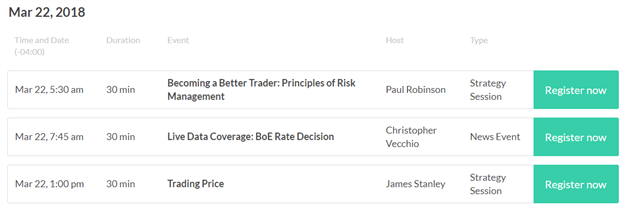

DailyFX Webinar Calendar: Thursday, March 22, 2018

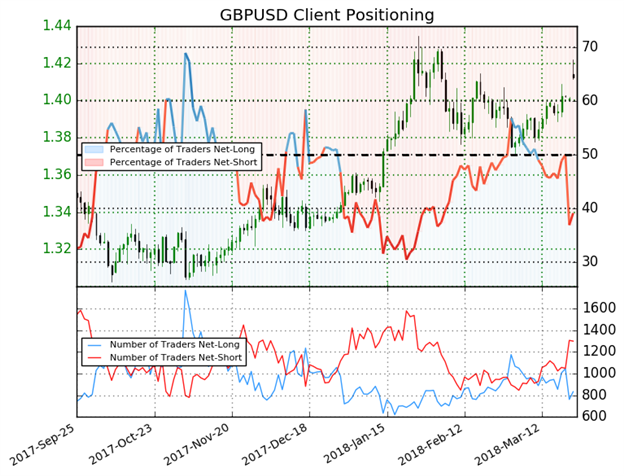

IG Client Sentiment Index Chart of the Day: GBPUSD

GBPUSD: Retail trader data shows 39.1% of traders are net-long with the ratio of traders short to long at 1.56 to 1. The number of traders net-long is 18.9% lower than yesterday and 15.2% lower from last week, while the number of traders net-short is 14.7% higher than yesterday and 14.1% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests GBPUSD prices may continue to rise. Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger GBPUSD-bullish contrarian trading bias.

Learn more about the IG Client Sentiment Index on the DailyFX Sentiment page

Five Things Traders are Reading

- “BoE Is Slightly More Hawish Despite Holding Rates, Markets Look Towards May Meeting” by Dylan Jusino, Research Assistant

- “USD Reeling after Fed’s Dovish Hike; GBP a Buy on Dips around BOE” by Christopher Vecchio, CFA, Senior Currency Strategist

- “NZD/USD Technical Analysis: NZ Dollar Trend Points Downward” by Ilya Spivak, Senior Currency Strategist

- “Crude Oil Prices May Retreat as Trump China Tariffs Sour Sentiment” by Ilya Spivak, Senior Currency Strategist

- “Gold & Silver Pop on Fed, USD Tank; Charts Need More Work for Clarity” Paul Robinson, Market Analyst

The DailyFX US AM Digest is published every day before the US cash equity open - you can SIGNUP HERE to receive this report in your inbox every day.

The DailyFX Asia AM Digest is published every day before the Tokyo cash equity open - you can SIGNUP HERE to receive that report in your inbox every day.

If you're interested in receiving both reports each day, you can SIGNUP HERE.