Australian Dollar, AUD/USD, Jobs Report, FOMC, Oil Prices - Talking Points

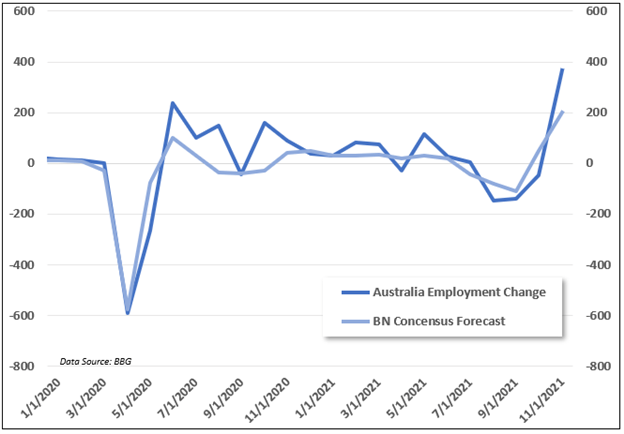

- Aussie economy adds a strong 366.1k jobs in December, beating expectations

- China’s Foreign Direct Investment (FDI) on tap as traders eye BoE, ECB

- AUD/USD at a pivotal junction as prices battle formidable resistance level

The Australian Dollar remained firm against the US Dollar following today’s employment report. Australia saw a gain of 366k jobs for December, beating the 200k Bloomberg consensus forecast. That pushed the unemployment rate down to 4.6% from 5.2%. Analysts expected the unemployment rate to cross the wires at 5.0%, according to a Bloomberg survey. Also encouraging was a tick higher in the participation rate, which shows more workers entered the workforce. AUD/USD held its overnight gains following the rosy report.

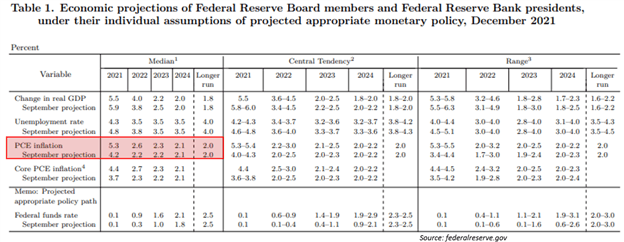

A risk-on sentiment gripped markets overnight after an initially volatile reaction to the Federal Reserve rate decision. The yield curve flattened on the initial reaction but subsequently reversed course once Fed Chair Powell took the podium. Mr. Powell’s statement that the central bank would hold off with any rate increases until the labor market tightens further appeared to smooth concerns over a much more hawkish dot plot, which projects where respective FOMC members see rates in the coming years. The Fed sees PCE inflation at 2.6% in 2022 in its updated projections, up from September’s 2.2% projection.

Crude and Brent oil prices moved higher overnight after traders turned bullish on a larger-than-expected US inventory draw, according to government data. The Energy Information Administration (EIA) reported crude stocks for the week ending December 10 fell by 4.6 million barrels. Analysts were expecting a 2 million barrel draw. However, the inventory reduction appears to be driven by foreign demand rather than domestic, with exports increasing and storage levels at Cushing, Oklahoma firming.

This morning, New Zealand’s third-quarter gross domestic product (GDP) growth rate crossed the wires at -0.3% on a year-over-year basis. Economists saw the Kiwi economy contracting at a deeper 1.6% on concerns that Covid lockdowns through Q3 would have a larger drag on consumer demand. NZD/USD saw a slight boost to strength following the report. The island nation will see a business confidence report for December later this week from ANZ Bank.

Asia-Pacific markets are likely to see an extension of the post-FOMC strength seen in the US trading hours, with the event risks of the Fed and Australian jobs report in the rearview mirror. Later today, Australia will report HIA new home sales (Nov). Tonight in the European session, the Bank of England (BoE) and European Central Bank (ECB) will report their own rate decisions.

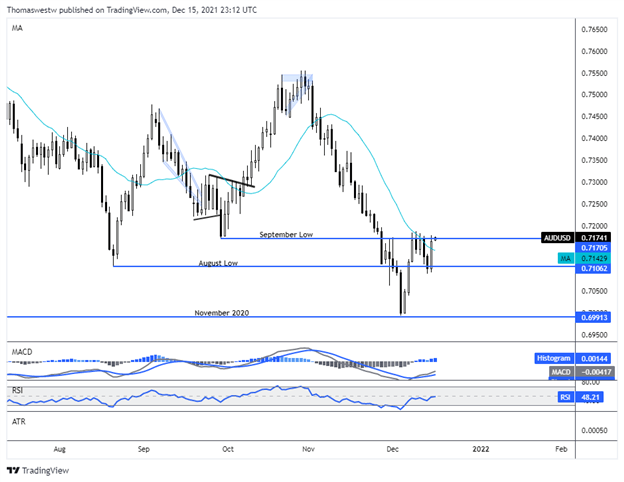

AUD/USD Technical Forecast

AUD/USD is currently probing above a pertinent level of resistance stemming from the September swing low at 0.7170, a level that has capped upside action over the last week. If prices manage to hold above resistance, it could lead to a subsequent rally in the currency pair. Alternatively, a reversal lower would target the August low at 0.7106, with the 20-day Simple Moving Average (SMA) providing possible intermediate support.

AUD/USD Daily Chart

Chart created with TradingView

--- Written by Thomas Westwater, Analyst for DailyFX.com

To contact Thomas, use the comments section below or @FxWestwater on Twitter