Central Bank Watch Overview:

- Rates markets are certain that the Federal Reserve will hike rates this week.

- Expectations for a 50-bps rate hike have dropped considerably since the Russian invasion of Ukraine.

- Financial conditions are at their tightest levels since late-2011, which may give the FOMC reason to take a ‘soft hawkish’ tone.

Fed Meeting on Wednesday

In this edition of Central Bank Watch, we’ll review comments and speeches made by various Federal Reserve policymakers prior to the communications blackout window around the March Fed meeting ended. Despite Russia’s invasion of Ukraine, there was a continued hawkish undertone among most policymakers, even if chatter around a 50-bps rate hike has cooled off.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

25-bps or 50-bps in March?

Fed policymakers have taken a hawkish tone in the month leading up to the March Fed meeting, with several officials noting their openness (and preference) for a 50-bps rate hike to start the rate hike cycle. However, there is a clear schism in the commentary once Russia’s invasion of Ukraine began, with several policymakers noting the negative implications for US growth, which may warrant a more measured approach over the coming months. One thing is clear though: rate hikes are coming fairly consistently over the next few months.

February 18 – Brainard (Fed governor) talked up the possibility of a balance sheet runoff starting toon, suggesting “we have a recovery today that is much stronger and faster than in the last cycle…it will be appropriate to commence that runoff in the next few meetings.”

February 21 – Bowman (Fed governor) suggested that a 50-bps rate hike might be appropriate if inflation rates continue to press higher in the coming months.

February 22 – Bostic (Atlanta president) said that Fed policy was positioned as if there was an emergency ongoing, which there isn’t, and thus it’s time to “moveoff the emergency stance.”

February 23 – Daly (San Francisco president) said that “inflation is too high, and inflation pressures have begun tospread outside of sectors most directly affected by pandemic-related disruptions.” As such, “It is time to move away from the extraordinarysupport that the Fed has been providing during the pandemic andbring monetary policy in line with the challenges of today.”

February 24 – Mester (Cleveland president) warned that Russia’s invasion of Ukraine could pose a problem to the US economy, and that “the medium-run economic outlook in the U.S. will also be aconsideration in determining the appropriate pace at which toremove accommodation.” Nevertheless, “barring an unexpected turn in the economy, I believe it will be appropriate to move the funds rate up in March and follow with further increases in the coming months.”

Waller (Fed governor) said that he supported a 25-bps rate hike in March, and potentially even if a 50-bps rate hike, but the situation in Ukraine warranted careful monitoring.

February 25 – Bullard (St. Louis president) noted that he believed “it will soon be appropriate to raise the targetrange for the federal funds rate,” and downplayed the impact of the Russian invasion of Ukraine on the US economy.

February 28 – Bostic noted that he favored a 25-bps rate hike in March, but wouldn’t dismiss a 50-bps rate hike if the “month-to-month change in inflation…continues to persist at elevated levels.”

March 1 – Mester warned that Russia’s invasion of Ukraine “has implications for the economic outlook - adding upside risk to inflation even as it puts downside risk to the growth forecast.”

March 2 – The Fed’s Beige Book hinted that the US economy had “expanded at a modest to moderate pace since mid-January,” but was vulnerable to a slowdown should inflation pressures remain elevated.

Powell (Fed Chair) confirmed that a 25-bps rate hike was coming in March, but also that “to the extent that inflation comes in higher or is more persistently high than that, then we would be prepared to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings.”

March 3 – Powell reiterated his support for a 25-bps rate hike in testimony to the Senate Banking Committee.

March 4 – Evans (Chicago president) hinted that he supports seven 25-bps rate hikes in 2022, saying “if we were to do 25 basis points at each meeting, which maybe more than I think is essential, but if we did it at eachmeeting, we’ll end the year at 1.75% to2%.”

The First of Many Rate Hikes

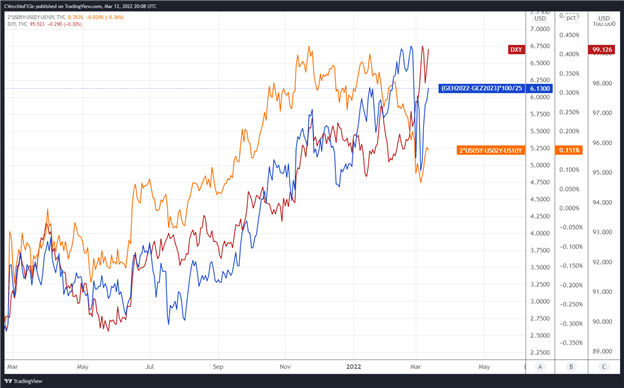

It is effectively set in stone that the Fed will hike rates by 25-bps at their meeting this week. We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the March 2022 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (March 2022-December 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Timeframe (March 2021 to March 2022) (Chart 1)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

There are six 25-bps rate hikes discounted through the end of 2023. Rates markets are pricing in a 100% chance of six 25-bps rate hikes and a 13% chance of seven 25-bps rate hikes through the end of next year. The 2s5s10s butterfly has begun to widen in recent weeks, evidence that markets are refocusing on what the Fed will do and less on the market implications around Russia’s invasion of Ukraine.

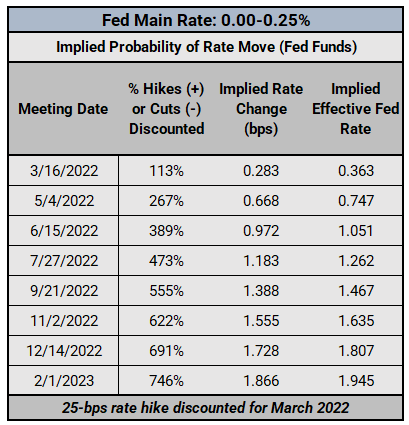

Federal Reserve Interest Rate Expectations: Fed Funds Futures (March 15, 2022) (Table 1)

Fed fund futures have become less more aggressive in recent weeks, ever since Russia invaded Ukraine. Ahead of the March Fed meeting, traders see a 100% chance of a 25-bps rate hike, with a 13% chance of a 50-bps rate hike. This is down from its peak in early-February, when there was a 48% chance of a 50-bps rate hike.

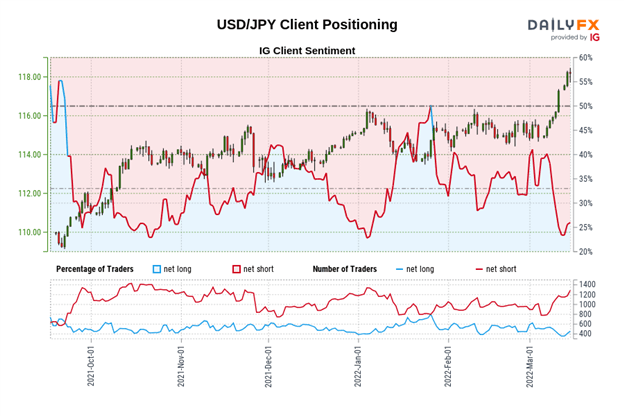

IG Client Sentiment Index: USD/JPY Rate Forecast (March 15, 2022) (Chart 2)

USD/JPY: Retail trader data shows 22.42% of traders are net-long with the ratio of traders short to long at 3.46 to 1. The number of traders net-long is 9.91% lower than yesterday and 17.70% lower from last week, while the number of traders net-short is 7.20% higher than yesterday and 39.94% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/JPY-bullish contrarian trading bias.

--- Written by Christopher Vecchio, CFA, Senior Strategist