Central Bank Watch Overview:

- Rates markets are anticipating the Federal Reserve to hike rates by 25-bps in March, as soon as the QE taper is finished.

- Expectations for a 50-bps rate hike persist, though they have pulled back considerably ahead of the January Fed meeting.

- The commentary around the potential for a 50-bps rate hike as well as the start of QT will likely provoke significant volatility in financial markets.

Here Comes the Fed

In this edition of Central Bank Watch, we’ll review comments and speeches made by various Federal Reserve policymakers in the week ahead the communications blackout window around the January Fed meeting ended. The blackout started on Saturday, January 15, leaving financial markets without any significant policy cues for nearly two weeks.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Remarks Before Communication Blackout

The volatility seen in US equity markets over the past two weeks is rather remarkable, insofar as it has been spurred by speculation by how quickly the Federal Reserve will normalize policy – without any clear indications from FOMC policymakers themselves about how quickly that process with transpire. To wit, the US S&P 500 is down over -9% since the Fed’s communication blackout window began.

January 4 – Kashkari (Minneapolis president) restated his belief that inflation is transitory, while issuing concern over persistently high inflation, saying “Fundamentally, I believe it is more likely we end up back in the low-inflation regime that we were in for 20 years than a new high-inflation regime...However, the costs of ending up in the high-inflation regime are likely larger than the costs of ending up back in the low- inflation regime.”

January 5 – The December FOMC minutes are released and stoke speculation that the process of unwinding the Fed’s balance sheet – quantitative tightening, or QT – could soon begin shortly after the rate hike cycle commenced.

January 6 – Bullard (St. Louis president) said that “the FOMC could begin increasing the policy rate as early as the March meeting in order to be in a better position to control inflation,” and that “subsequent rate increases during 2022 could be pulled forward or pushed back depending on inflation developments.”

January 7 – Daly (San Francisco president) furthered speculation around QT by saying that she “would prefer to adjust the policy rate gradually and move into balance-sheet reductions earlier than we did in the last cycle.”

January 11 – Powell (Fed Chair) struck a hawkish tone at his confirmation hearing, saying that “we will use our tools to get inflation back” and “if we have to raise interest rates more over time,we will.”

January 12 – Mester (Cleveland president) similarly stuck to the hawkish script, saying “the case is very compelling that we remove accommodation,” and “we’ll also be considering what we can do with our balance sheet, to bring the level of assets on our balance sheet down.”

January 13 - Brainard (Fed governor) at her confirmation hearing warned that “inflation is too high, and working people around the country are concerned about how far their paychecks will go.” In turn, she noted that “the committee has projected several hikes over the course of the year.”

January 14 – Williams (NY president) suggested policy normalization was imminent, noting “the next step in reducing monetary accommodation to the economy will be to gradually bring the target range for the federal funds rate from its current very-low level back to more normal levels.”

Rate Hikes Sooner Rather Than Later

Rates markets have dragged forward hike expectations rapidly throughout January, much to the chagrin of risk assets. But regardless of how you measure expectations, it’s evident that monetary tightening is on the horizon by the end of 1Q’22.

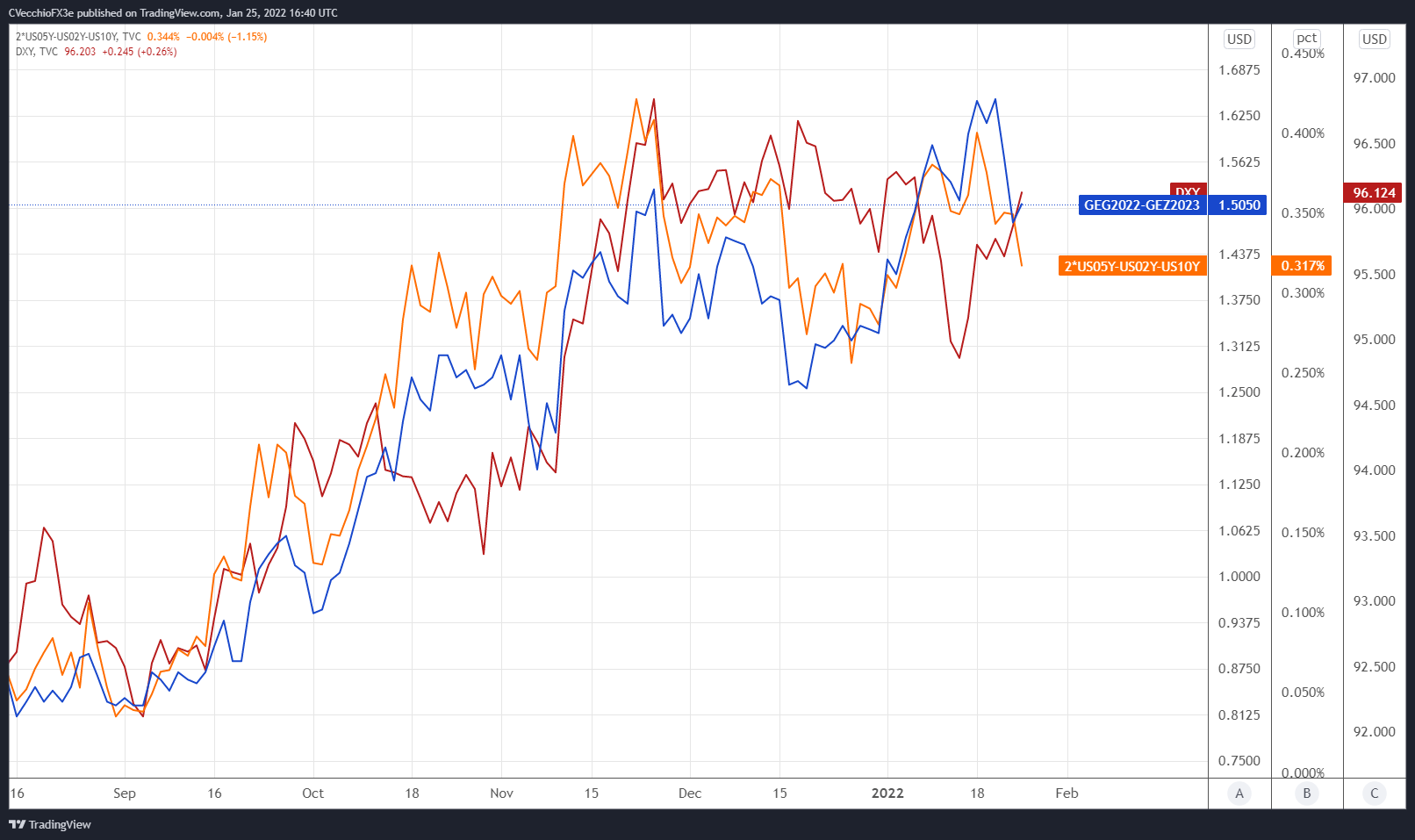

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 2 below showcases the difference in borrowing costs – the spread – for the February 2022 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (February 2022-December 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Timeframe (August 2021 to January 2022) (Chart1)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

There are 150.5-bps of rate hikes discounted through the end of 2023 while the 2s5s10s butterfly is just off of its widest spread since the Fed taper talk began in June. Ahead of the January Fed meeting, rates markets are pricing in a 100% chance of six 25-bps rate hikes and a 2% chance of seven 25-bps rate hikes through the end of next year. Furthermore, expectations for a 50-bps rate hike to start the hike cycle have edged higher in recent weeks.

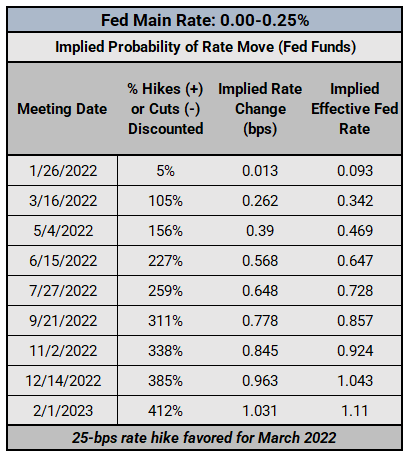

Federal Reserve Interest Rate Expectations: Fed Funds Futures (January 25, 2022) (Table 1)

Fed fund futures have continued to become more aggressive over the course of the month. At the end of December, Fed funds futures were pricing in March 2022 for the first 25-bps rate hike with a 63% chance. Now, one day ahead of the January Fed meeting, traders see a 100% chance of a 25-bps rate hike in March, with a 5% chance of a 50-bps rate hike. May will likely bring the second rate hike, with a 56% implied probability of transpiring.

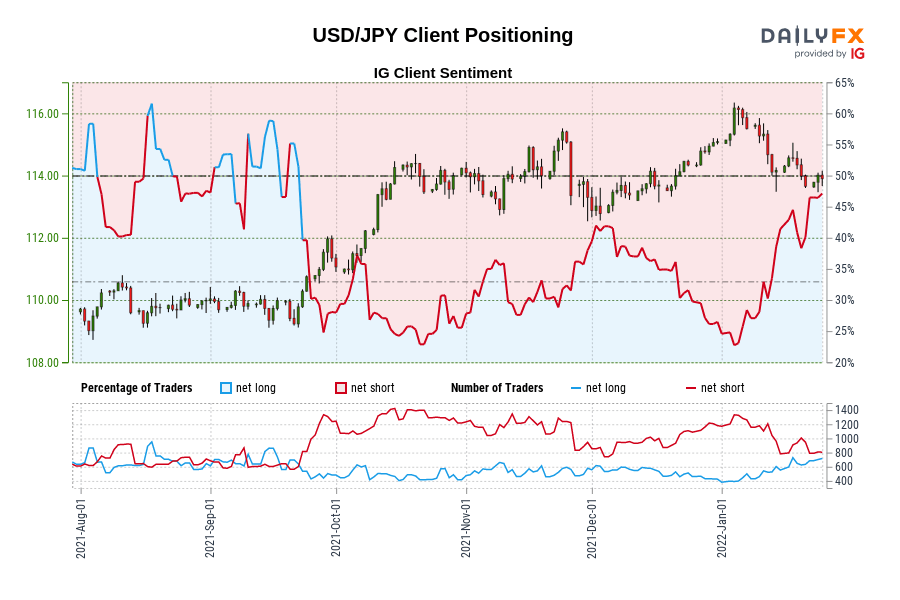

IG Client Sentiment Index: USD/JPY Rate Forecast (January 25, 2022) (Chart 2)

USD/JPY: Retail trader data shows 48.02% of traders are net-long with the ratio of traders short to long at 1.08 to 1. The number of traders net-long is 1.08% higher than yesterday and 17.71% higher from last week, while the number of traders net-short is 2.17% lower than yesterday and 14.33% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Yet traders are less net-short than yesterday and compared with last week. Recent changes in sentiment warn that the current USD/JPY price trend may soon reverse lower despite the fact traders remain net-short.

--- Written by Christopher Vecchio, CFA, Senior Strategist