Central Bank Watch Overview:

- The BOE looks ready to steam ahead with several rate hikes in 2022, as rates markets are currently pricing in at least four moves by December.

- There remains a disconnect between ECB rhetoric and market pricing, as policymakers continue to suggest that no rate hikes will arrive in 2022.

- Retail trader positioning suggests both EUR/USD and GBP/USD rates have bullish trading biases in the near-term.

Sense of Unease Spreads

In this edition of Central Bank Watch, we’ll cover the two major central banks in Europe: the Bank of England and the European Central Bank. The start of 2022 has produced meaningful moves in global bond markets, as traders expect a mild economic fallout from the COVID-19 omicron variant against the backdrop of persistently elevated inflationary pressures. And while this may mean a more aggressive Bank of England over the course of the year, there is a growing disconnect between what the market expects the European Central Bank will do versus what the ECB says it is going to do.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

UK Economy Ready for Hikes

The final BOE policy meeting of 2021 produced a 15-bps rate hike, which came as a surprise to traders as rates markets were pricing in roughly a 50% chance of a hike. But with UK inflation rates at there highest level in a decade and accumulating evidence that the labor market is steadily improving, both BOE policymakers and rates markets believe that more policy tightening is ahead. While the BOE has been quiet thus far in 2022, there is reason to believe that activity will pick-up in the coming weeks ahead of the first meeting of the year in February.

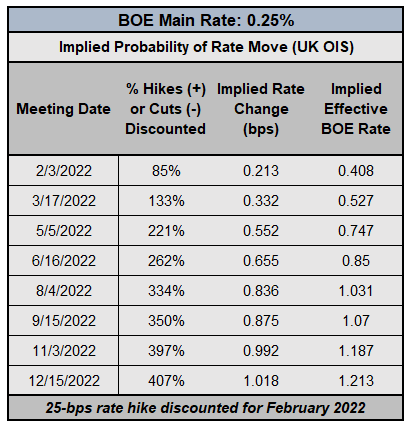

Bank of England Interest Rate Expectations (January 12, 2022) (Table 1)

As has been the case for the past month, rates markets are discounting February 2022 as the most likely period for when rates will rise next, with an 85% chance of a 25-bps rate hike; this is an increase from a 66% in mid-December. Moreover, rates markets have discounted a fourth rate hike in 2022, up from three in mid-December. The timing of the next BOE rate hike aligns neatly with the release of the Monetary Policy Committee’s next iteration of the Quarterly Inflation Report (QIR).

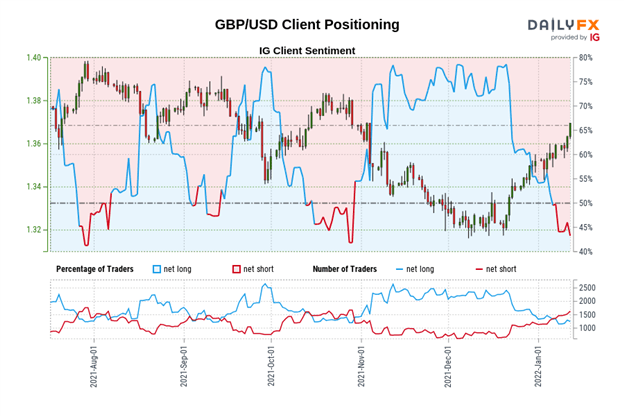

IG Client Sentiment Index: GBP/USD Rate Forecast (January 12, 2022) (Chart 1)

GBP/USD: Retail trader data shows 40.42% of traders are net-long with the ratio of traders short to long at 1.47 to 1. The number of traders net-long is 12.60% lower than yesterday and 20.88% lower from last week, while the number of traders net-short is 11.76% higher than yesterday and 21.30% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests GBP/USD prices may continue to rise.

Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger GBP/USD-bullish contrarian trading bias.

Someone is Wrong

ECB policymakers have been beating the same drum for the past several months: no rate hikes are coming in 2022. The final policy meeting of 2021 noted that the Governing Council believed that “monetary accommodation is still needed for inflation to stabilise at the 2% inflation target over the medium term.” ECB President Christine Lagarde has called the current rise in inflation as a “hump.” More recently, ECB Governing Council member Olli Rehn said that “supply-side problems do not yet lead to sustained inflation unless wage inflation is strongly triggered,” while noting that wage inflation has not been strongly triggered and thus higher inflation is likely to recede.

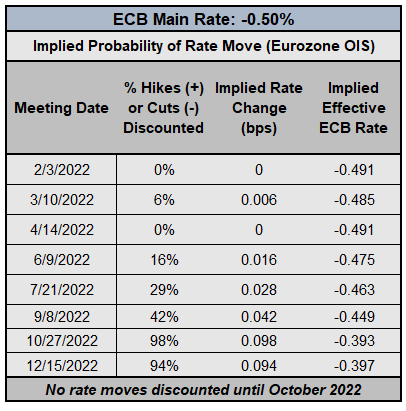

EUROPEAN CENTRAL BANK INTEREST RATE EXPECTATIONS (January 12, 2022) (TABLE 2)

As the ECB repeatedly signals that it will not back-off its accommodative policy efforts anytime soon, market pricing around the projected path of ECB rates may still be too hawkish. Rates markets are now pricing in a 98% chance of the first ECB rate hike to arrive in October 2022, up from a 67% chance in mid-December. The current Euro rally may be providing a selling opportunity as ECB rate hike odds are likely to fall back over 2022.

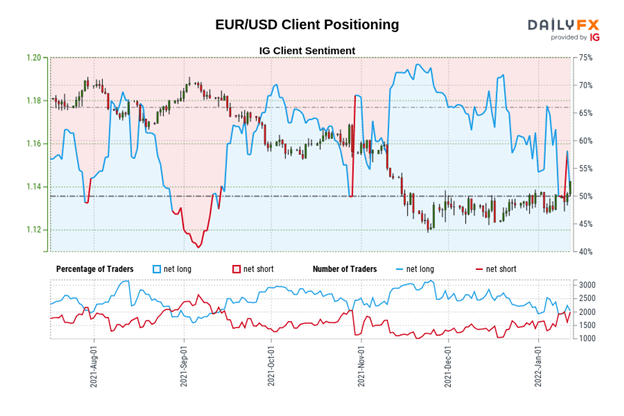

IG Client Sentiment Index: EUR/USD Rate Forecast (January 12, 2022) (Chart 2)

EUR/USD: Retail trader data shows 52.38% of traders are net-long with the ratio of traders long to short at 1.10 to 1. The number of traders net-long is 3.77% lower than yesterday and 6.99% lower from last week, while the number of traders net-short is 15.41% higher than yesterday and 19.23% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests EUR/USD prices may continue to fall.

Yet traders are less net-long than yesterday and compared with last week. Recent changes in sentiment warn that the current EUR/USD price trend may soon reverse higher despite the fact traders remain net-long.

--- Written by Christopher Vecchio, CFA, Senior Strategist