Central Bank Watch Overview:

- Markets are expecting a hawkish FOMC when the September Fed meeting concludes on Wednesday.

- Eurodollar contract spreads and the US Treasury yield curve continue to behave in a similar manner to the 2013/2014 period ahead of actual tapering.

- Fed rate hike odds have risen and stayed elevated since early-August when the July FOMC minutes were released.

US Data Resiliency Supports Taper Hint

In this edition of Central Bank Watch, we’ll review the speeches made during September by various Federal Reserve policymakers. Although Fed policymakers have been in their communications blackout period ahead of their meeting set to conclude on Wednesday, September 22, comments made at the start of the month are still informative.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Taper Talk at Full Tilt

In context of recent economic data, it seems that more “progress” may have been made towards the Fed’s goal of seeing jobs growth return to its pre-pandemic days: August US retail sales proved better than expected; and weekly jobless claims data have not suggested significant volatility in the labor market as unemployment insurance benefits have ended. It is widely anticipated that the September Fed meeting will yield a strong hint that the taper will begin before the end of the year.

September 2 – Bostic (Atlanta president) says “we’ve changed our long-run framework to saywe’renot going to be preemptive in this but rather we’re going to letthe economy continue torun until we see signs of inflation” ahead of hiking rates.

September 8 – Williams (New York president) says notes that “it could be appropriate” to begin tapering its bond-buying program before the end of 2021.

Kaplan (Dallas president) comments that he already thinks it’s time to taper, and that “if I get to the meeting and continue to feel that way, I’d be advocating that we should announce a plan for adjusting these purchases in the September meeting and begin shortly thereafter, maybe in October.”

The Beige Book summarized that the August“deceleration in economic activity was largely attributable to a pullback in dining out, travel, and tourism in most Districts, reflecting safety concerns due to the rise of the Delta variant.”

September 9 – Evans (Chicago president) says “after the deep and sharp downturn in economic activity last year, we have seen strong economic growth. However, challenges abound, as evidenced by widespread bottlenecks in supply chains and labor markets.”

Bowman (Fed governor) notes “if the data comes in like I expect that it will, then it will likely be appropriate for us to begin the process of scaling back our asset purchases this year.”

September 13 – Harker (Philadelphia president) comments that it may be appropriate to begin tapering asset purchases “sooner rather than later.”

Markets Expecting Hawkish FOMC

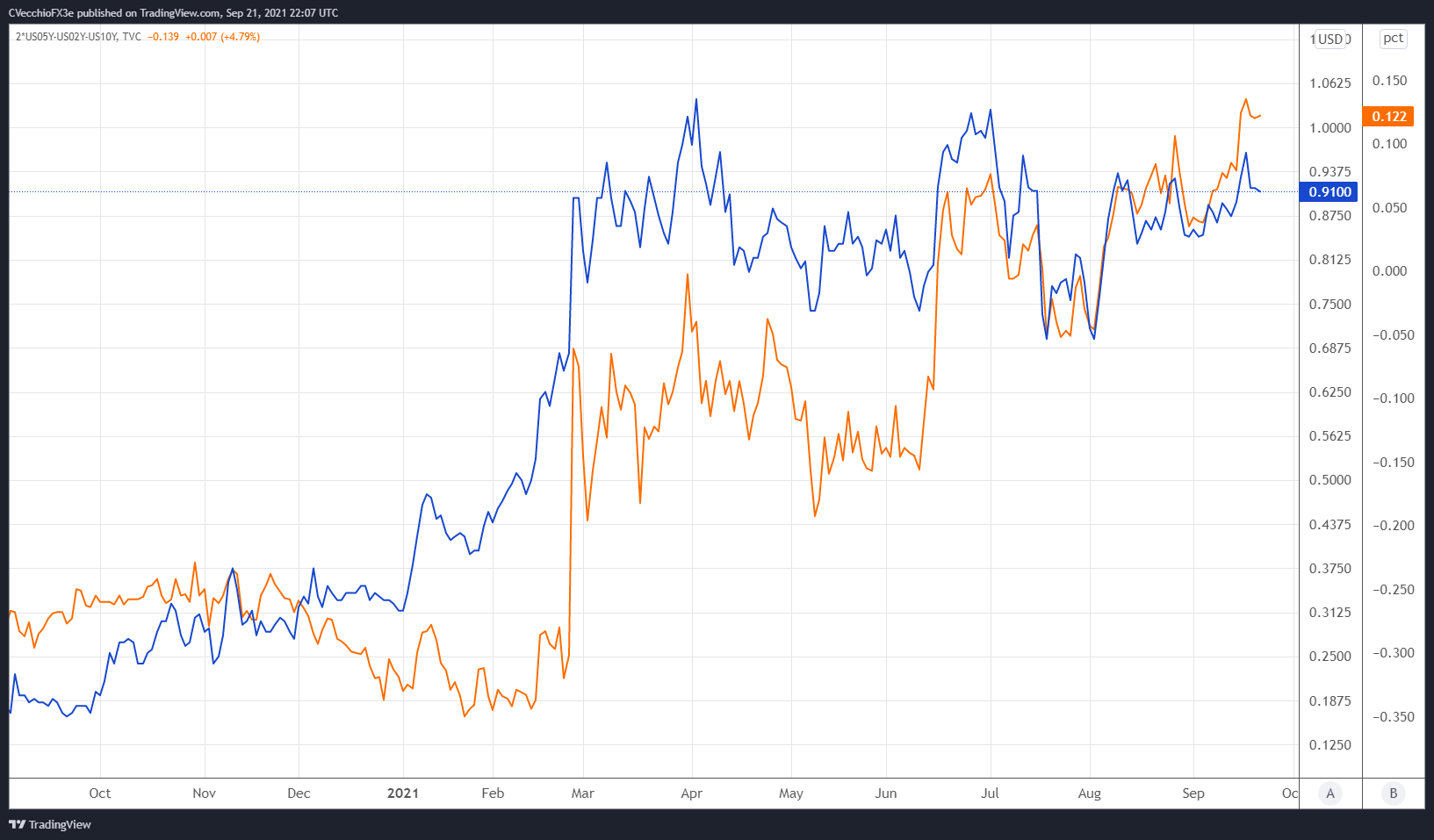

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the September 2021 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (September 2021-DECEMBER 2023) versus US 2s5s10s Butterfly: Daily Rate Chart (September 2020 to September 2021) (Chart1)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

Elevated Eurodollar spreads and evidence that the US yield curve is moving in a manner consistent with the 2013/2014 period that suggests a relatively more hawkish Fed is soon to arrive.

There are 91-bps of rate hikes discounted through the end of 2023 – that’s three hikes plus a 64% chance of a fourth 25-bps rate hike – and the 2s5s10s butterfly has increased to its highest rate since the Fed taper talk began in June (and its widest spread of all of 2021). However, consistent with recent chatter from FOMC officials, the first rate hike looks increasingly likely to arrive in late-2022.

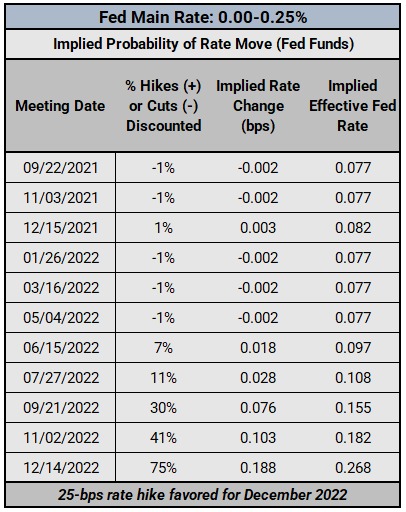

Federal Reserve Interest Rate Expectations: Fed Funds Futures (September 21, 2021) (Table 1)

Rate hike expectations have been rather consistent for two months. Ahead of the July FOMC meeting, markets were pricing in a 68% chance that December 2022 would be the first month that produced a 25-bps rate hike. Now, just ahead of the September Fed meeting, Fed funds futures are pricing in a 75% chance of the first hike arriving in December 2022. Not a significant change, but one that speaks to a more hawkish outlook by market participants.

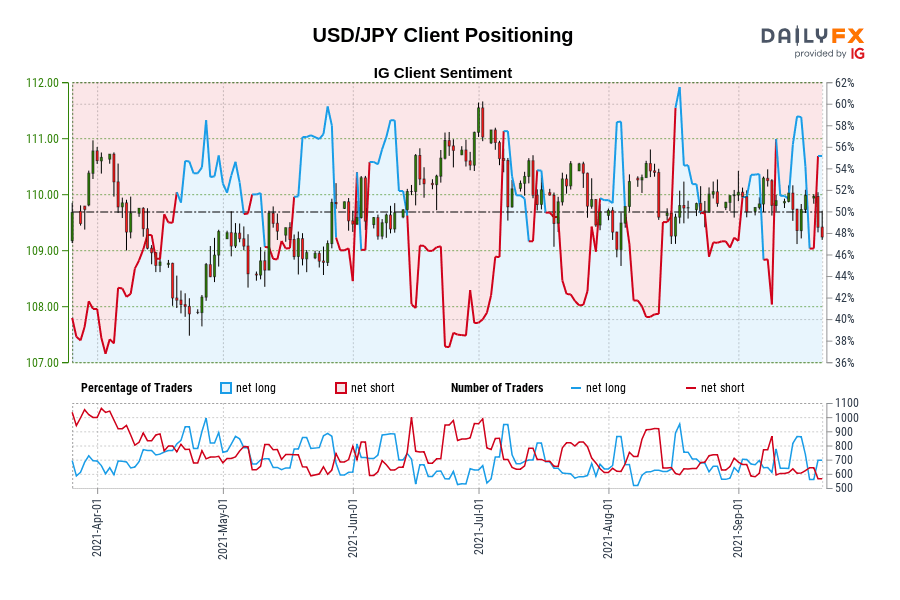

IG Client Sentiment Index: USD/JPY Rate Forecast (September 21, 2021) (Chart 2)

USD/JPY: Retail trader data shows 60.36% of traders are net-long with the ratio of traders long to short at 1.52 to 1. The number of traders net-long is 17.96% higher than yesterday and 0.77% lower from last week, while the number of traders net-short is 13.87% lower than yesterday and 18.43% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/JPY prices may continue to fall.

Traders are further net-long than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/JPY-bearish contrarian trading bias.

--- Written by Christopher Vecchio, CFA, Senior Strategist