JAPANESE YEN, LEVERAGED LOANS, FED RATE HIKE - TALKING POINTS

- Japanese Yen outlook bullish on “high” risks in $3 trillion leveraged loan market

- Low interest rate regime prompted firms to issue and purchase high-yielding debt

- Fed rate hikes on the horizon could undermine stability of credit-dependent loans

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

The Japanese Yen may get a boost if market-wide risk aversion grips investors amid turbulence in the US$3 trillion leveraged loan market. With the Fed intent on raising rates in 2022 and halting its bond-purchasing program, loans made under an easy-credit regime may be in trouble. As a result, the appeal of the anti-risk JPY and haven-linked US Dollar may rise.

LOW INTEREST RATES FUELED BOOM IN CORPORATE DEBT MARKET

To avoid a credit crunch during the pandemic, the Fed took aggressive measures to suppress rising yields via rate cuts and unprecedented quantitative easing (QE). The Fed purchased investment-grade corporate debt in addition to the more common outlays for Treasury bonds and mortgage-backed securities to soothe liquidity concerns.

Monetary authorities took another unorthodox step: the Fed expanded its asset-purchasing program to include so-called “junk bonds”, which have a comparatively higher probability of default. It should be noted, the central bank only purchased so-called “fallen angels” - bonds with high credit ratings before the pandemic that had a downgrade thereafter - and not debt that was sub-investment grade before the viral outbreak.

In addition to buying corporate debt on the secondary market, the Fed also purchased ETFs that were structured to provide exposure to junk bonds. While this helped quell liquidity concerns as intended, it also compounded the multi-year trend of firms issuing increasingly-risky debt in rising volumes. An OECD report from 2 years ago found that:

“Just over half (51%) of all new investment grade bonds in 2019 were rated BBB, the lowest investment-grade rating. During the period 2000-2007, only 39% of investment grade issues were rated BBB…In 2019, only 30% of the global outstanding stock of non-financial corporate bonds were rated A or above and issued by companies from advanced economies.”

Trading Strategies and Risk Management

Global Macro

Recommended by Dimitri Zabelin

When interest rates were low - or in some cases, negative - investors became starved for yields. Naturally, risky corporate debt was an investment avenue to drive down because the roads were paved with easy credit. However, the prospect of higher rates, combined with poor underwriting standards means this road is likely to get a lot bumpier ahead.

The legendary investor and co-founder of Oaktree Capital Management Howard Marks wrote about this credit-debt sequence in his book Mastering the Market Cycle. Based on his analysis – which echoes the broad-based consensus of market macroeconomists - a period of jubilance is frequently followed by an interim of reckoning. In this interval, high volatility often boosts havens and anti-risk assets.

To learn more, be sure to follow me on Twitter @ZabelinDimitri.

It's akin to musical chairs: everything is great until the music stops playing and you’re left without a chair. Adding to the metaphor: the bigger they are, the harder they fall. A recent report by the Federal Reserve Board, Federal Deposit Insurance Corporation and the Office of the Comptroller of the Currency solidified these concerns.

Officials found loans with “weak structures” that include aggressive repayment schedules, shaky covenants, and high leverage. The Fed is not sounding the alarm alone. Earlier this month, the Chair of the European Central Bank's (ECB) Supervisory Board, Andrea Enria, warned banks that authorities will raise capital requirements unless they reduce exposure to high-risk loans.

FED RATE HIKE PLANS LIKELY TO STOKE VOLATILITY

At the most recent Fed meeting in January, the Federal Open Market Committee (FOMC) held the Federal Funds rate in the 0-0.25% rnage. However, with multi-decade high inflation figures, the Fed also signaled incoming rate hikes and an intention to aggressively reduce its balance sheet.

Some board members, such as James Bullard, have advocated for what many consider a bold approach: a full percentage point in rate hikes over the course of the upcoming three FOMC meetings. This means that at one of these meetings, the target rate would go up not by the standard 25 basis points but by double that, or half of a percentage point.

Trading Strategies and Risk Management

Volatility

Recommended by Dimitri Zabelin

With investors used to ultra-loose credit conditions - and many floating-rate loans issued during that time - a sharp increase in yields could have a ripple effect. Furthermore, with higher borrowing costs and a cooling down of the economy, firms with already-thin profit margins and high debt become increasingly vulnerable to default.

Non-bank and financial institutions with exposure to these loans will then be on the hook for taking losses on debt which offers little to no protection for the lender. These so-called “covenant-lite” loans make up the bulk of corporate debt that has been issued over the past several years.

WHY DO FX TRADERS CARE?

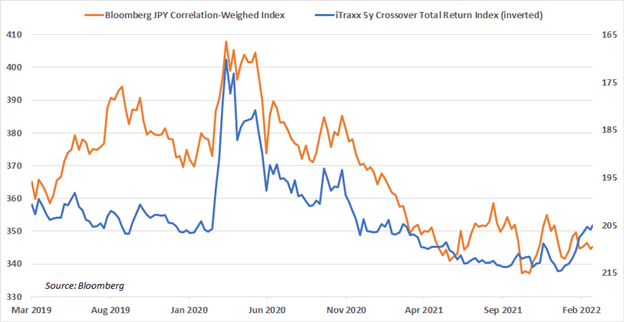

Volatility in credit markets has historically proven to spill out into other asset classes. While past performance is not indicative of future results, the data provides a compelling narrative. Overlaying a correlation-weighted currency index of the Japanese Yen with a credit default swap (CDS) tracker of sub-investment grade corporate debt in Europe shows a significant relationship.

When credit spreads sharply widened - meaning, investors were demanding a higher yield for the increased risk of default - the Japanese Yen generally rose against a basket of other currencies. In these kinds of scenarios, investors prioritized minimizing losses over generating returns amid bouts of market-wide risk aversion.

Looking ahead, the addition of idiosyncratic shocks - like the conflict in Ukraine – on top of the risks associated with Fed tightening could exacerbate these dynamics. To protect against future volatility, traders may increase their exposure to liquid, low-yielding assets at the expense of comparatively riskier, higher-yielding securities. In the G10 FX space, the Japanese Yen is typically in such circumstances.