US Recession Watch Overview:

- Although US Treasury yields have risen in recent weeks, 4Q’20 growth expectations have slid. A double dip recession may or may not be avoided in 1Q’21, depending upon the timing of US fiscal stimulus.

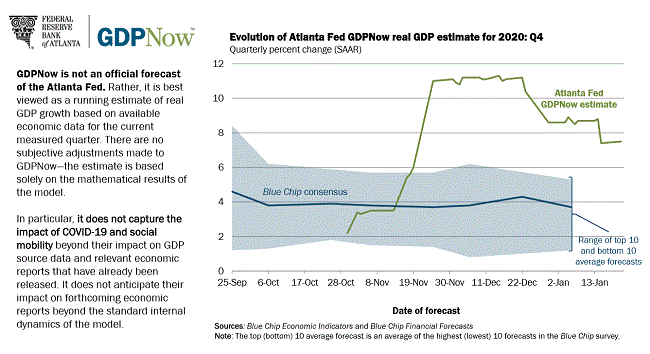

- The New York Nowcast estimate for 4Q’20 GDP is at +2.58%, while the Atlanta Fed GDPNow model is pointing to loftier+7.5% growth.

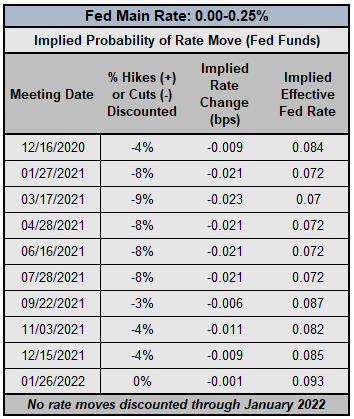

- Rates markets continue to forecast no change in the Federal Reserve’s main interest rate through January 2022; the Fed has pledged to keep rates low through 2023.

Making Sense of US Economic Data

On Thursday, the 4Q'20 US GDP report will be released. A Bloomberg News survey is calling for US GDP to come in at +4% annualized in 4Q’20 after surging by a record +33.4% in 3Q’20. Depending upon where you look, estimates vary significantly. The New York Nowcast estimate for 4Q’20 GDP is at +2.58%, while the Atlanta Fed GDPNow model is pointing to loftier+7.5% growth.

But the fact of the matter is that Bloomberg consensus forecasts and the regional Fed bank forecasts have been coming down for the past several weeks, reflecting a deceleration in US growth as the coronavirus pandemic entered its darkest days. Even though the next tranche of US fiscal stimulus was agreed upon at the end of the Trump presidency, it is still possible that 1Q’21 US GDP comes out in negative territory (but we won’t find that out until April).

Atlanta Fed GDPNow Q4’20 US GDP Estimate (January 26, 2021) (Chart 1)

Rising US initial jobless claims, weakening ISM and PMI surveys, and disappointing consumption figures all point to a US economy that has decelerated in recent months. No surprise, this deceleration has mirrored the sharp rise in coronavirus infections, hospitalizations, and deaths.

But the prospect of another $1.9 trillion in US fiscal stimulus pushed by US President Joe Biden, now that Democrats have full control of Congress, has helped put a floor under falling growth expectations. If policymakers on Capitol Hill are able to get another tranche of stimulus passed in February, then additional government rescue funds could help the US economy avoid a double-dip recession in 1Q’21.

Fed Driving the Narrative, Still

The January Fed policy meeting set to conclude on January 27 is the first of the Biden presidency. Beyond that, who cares? After much ado about a potential tapering of its QE program, Fed officials took to the airwaves in mid-January to hush a potential taper tantrum. The first meeting of the year, without a new Summary of Economic Projections, may offer little by way of tangible policy shifts to provoke volatility.

Federal Reserve Interest Rate Expectations (January 26, 2021) (Table 1)

The Fed has pushed back against rising expectations of a more hawkish central bank, tamping down taper tantrum concerns with a bevy of speeches in mid-January. As long as Fed Chair Jerome Powell is at the helm, the FOMC will stay the course, with the intent of keeping interest rates low through 2023. Fed funds futures are pricing in a 100% chance of no change in Fed rates through January 2022. As such, traders may see the January Fed meeting come and go with much ado about nothing.

Using the US Yield Curve to Predict Recessions

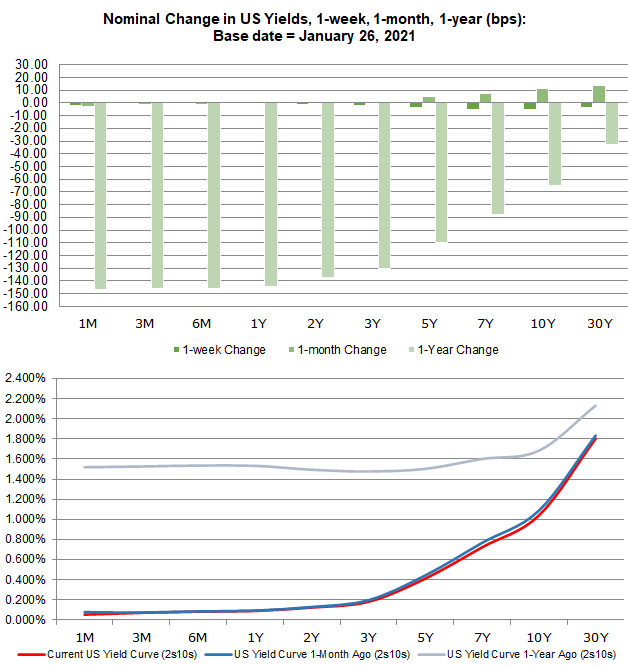

The commentary on the US Treasury yield curve remains ‘wash, rinse, repeat.’ The US Treasury yield curve remains normalized – long-end yields are higher than short-end yields. Historically, the relatively faster rise by long-end yields compared to short-end yields occurs during times of expected economic expansion, so traders may be prone to interpret the yield curve movements as a sign that market participants believe that the worst period of uncertainty around the coronavirus pandemic is over.

US Treasury Yield Curve: 1-month to 30-years (January 26, 2021) (Chart 2)

The Fed’s efforts to flood the market with liquidity have depressed short-end yields, helping keep intact an artificially steep of the US yield curve. Eroding US economic data momentum alongside alarming COVID-19 data would suggest that the near-term growth environment is not as certain as the US Treasury yield curve would suggest. We’re still of the belief that the combination of a steeper US yield curve and a US Dollar failing to rally is a fundamental red flag.

A Refresher: Why Does the US Yield Curve Matter?

Market participants use yield curves to gauge the relationship between risk and time for debt at various maturities. Yield curves can be constructed using any debt, be it AA-rated corporate bonds, German Bunds, or US Treasuries.

A “normal” yield curve is one in which shorter-term debt instruments have a lower yield than longer-term debt instruments. Why though? Put simply, it’s more difficult to predict events the further out into the future you go; investors need to be compensated for this additional risk with higher yields. This relationship produces a positive sloping yield curve.

When looking at a government bond yield curve (like Bunds or Treasuries), various assessments about the state of the economy can be made at any point in time. Are short-end rates rising rapidly? This could mean that the Fed is signaling a rate hike is coming soon. Or, that there are funding concerns for the federal government. Have long-end rates dropped sharply? This could mean that growth expectations are falling. Or, it could mean that sovereign credit risk is receding. Context obviously matters.

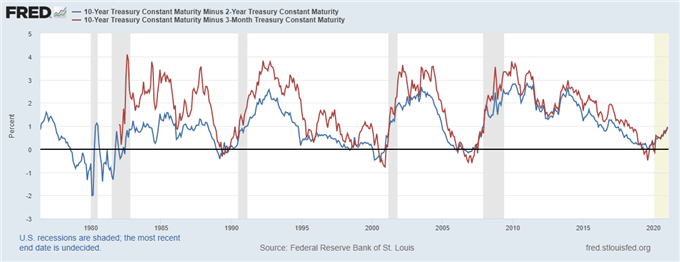

US Treasury Yield Curves: 3m10s and 2s10s (1975 to 2021) (Chart 3)

There is an academic basis for yield curve analysis. In 1986, Duke University finance professor Campbell Harvey wrote his dissertation exploring the concept of using the yield curve to forecast recessions. Professor Campbell’s research noted that the US yield curve needs to invert in the 3m10s for at least one full quarter (or three months) in order to give a true predictive signal (since the 1960s, a full quarter of inversion has predicted every recession correctly).

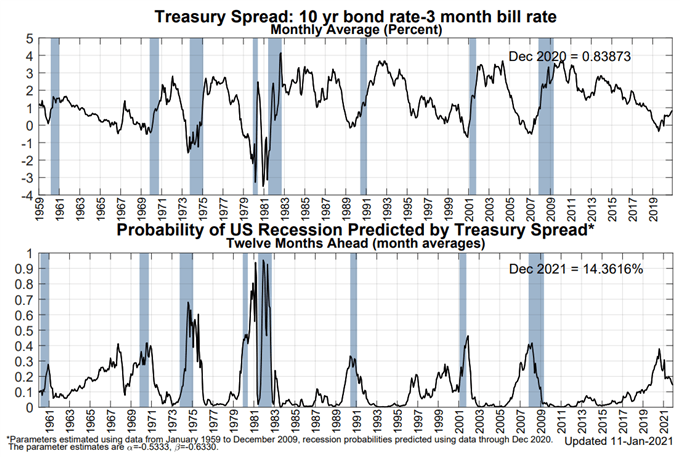

NY Fed Recession Probability Indicator (January 26, 2021) (Chart 4)

In aggregate, there is currently a 14.4% chance of a US recession in the next 12-months, per the NY Fed Recession Probability Indicator. Recall that this tracker never eclipsed 40% during the spring, even as 2Q’20 GDP was, quite literally, the worst quarter in US economic activity. Once more, the US yield curve is hiding the truth, masking what will likely be more weakness at the end of 4Q’20 and into early-1Q’21.

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist