Talking Points:

- The Fed minutes showed the group is ready to hike in June and expects to start its QE selloff this year

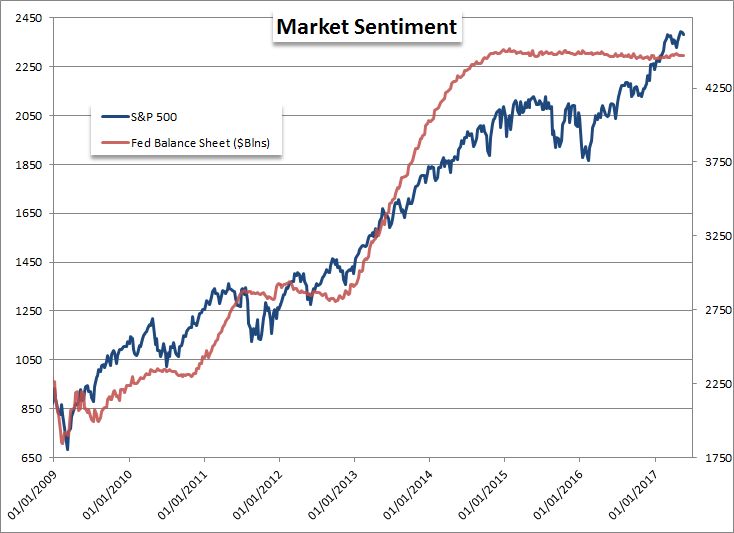

- Despite the upgrade in tightening efforts, the Dollar gained little traction, the SPX crawled higher and VIX sunk to 10

- A China credit downgrade by Moody's raises international risks but perhaps the NATO and G7 meetings will be more pressing

Short interest on EUR/USD has been rising steadily these past few weeks while net short retail positioning has hit its most extreme in at least six months? See the IG positioning statistics on the DailyFX sentiment page.

Risk trends wavered this past session, but certainly wouldn't find its direction despite both scheduled and unscheduled fundamental revelations throughout the session. The question traders and investors should be asking is whether complacency is indeed this deeply set or if the market is just keeping its powder dry for surprises from the key international meetings immediately on the horizon (the NATO and G7 summits). Either way, the market is refusing to break from its volatility fast. The S&P 500 has extended its slow speculative advance to a five-day climb - its first since February) to a 'technical' record high. Meanwhile, from the VIX volatility index, the retreat has brought it back to the 10 level. This puts us back into the record-setting low range that adds 'extreme' moniker to exceptionally low activity levels. This is equal parts complacency and speculative pressure to force the quiet trade. This adds significant risk to an exposure that is already barren of return.

This past session's lack of progress comes as something of a surprise considering there were a few remarkable developments on the fundamental backdrop. The first development early in the trading day was rating agency Moody's downgrade of China (and later Hong Kong). This carries serious practical risk, but a veil of confidence can minimize the threat in the near-term. A downgrade in credit quality for the world's second largest economy can further spur capital flight from this carefully controlled financial system and nudge up the percentage of bad loans on a system that is arguably flirting with a bubble. Nevertheless, neither the Chinese Yuan (USD/CNH) nor Hong Kong Dollar (USD/HKD) budged. That isn't too surprising given the authorities' control over these exchange rates. Later, in the US session, the FOMC minutes continued to lay the path towards a more substantial withdrawal of easy policy. The transcript of this month's meeting showed not only that support for a near-term rate hike - perhaps as early as June 14th - but it showed most officials supported a start in QE reductions this year. Given the market's reaction to the groups taper years ago, what will an actual selling of assets translate into?

Grand Dollar and risk trends aren't the only fundamental themes on display. This past session had both headlines and some volatility in isolated corners. Among a range of central bank activity, the aggressive doves in the ECB and BoJ offered little to move on while the otherwise neutral BoC's (Bank of Canada) in-line call led to a strong USD/CAD slide. For truly remarkable performance, we look to Bitcoin which continues to soar to record highs. Reports of adoption by Fidelity in a retail capacity and agreements on pursuing scalability has added lift to this already ebullient market. Looking ahead to tomorrow, the attention may once again turn back to the concentrated, high-profile themes. Populism and protectionism will be back in the headlines - for better or worse - with the second day of the NATO summit. US President Trump made very disparaging remarks about the defense relationship on the campaign trail and tension remains high. The President will also meet with European Union leaders Juncker and Tusk to account for the US-European economic relationship. Oil traders should also keep tabs on the OPEC gathering which will test a very active oil market. We discuss event risk and market activity in today's Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE