AUSTRALIAN DOLLAR FORECAST: BULLISH

- The Australian Dollar turns to local CPI for clues on RBA action

- China’s PBOC easing boosted an all already hot commodity market

- Fed hawkishness appears priced into USD. Will AUD/USD benefit?

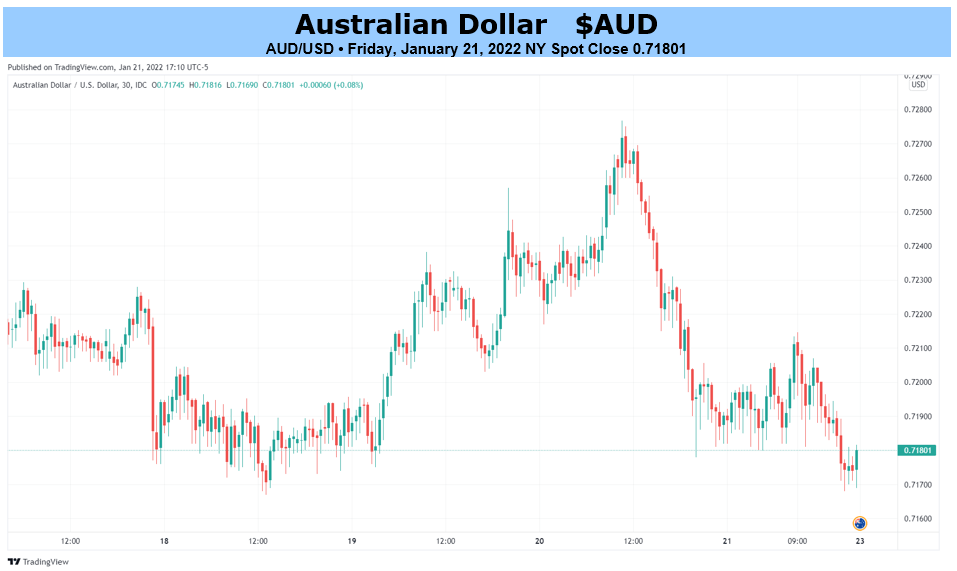

After being held hostage to mostly external factors so far this year, the focus for AUD/USD will likely turn to domestic factors this week.

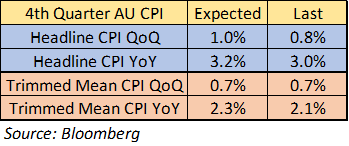

The all-important 4th quarter CPI numbers are due on Tuesday and the RBA will meet for the first time in 2 months on 1st February.

On the face of it, these numbers shouldn’t present too much of an issue for the RBA. If they come in close to expectations, they will not be forced to act too aggressively.

The mandated inflation target is 2-3% over the business cycle. They have previously stated that “The central forecast is for underlying inflation to reach 2½ per cent over 2023.” Underlying inflation is the trimmed mean measure.

However, any upside surprise may trigger the market to anticipate a more hawkish RBA. They have previously indicated that the asset purchase program will be reconsidered at the February meeting.

Aside from CPI, employment is another key component for the RBA to consider and data out this week showed a robust jobs market in December. 64.8k jobs were added for the month, in line with expectations. This is as the unemployment rate was better than anticipated, dropping to 4.2% from 4.6% previously.

An inflation print close to forecasts is likely to lead to market expectations of the RBA reducing, or potentially eliminating, the asset purchase program.

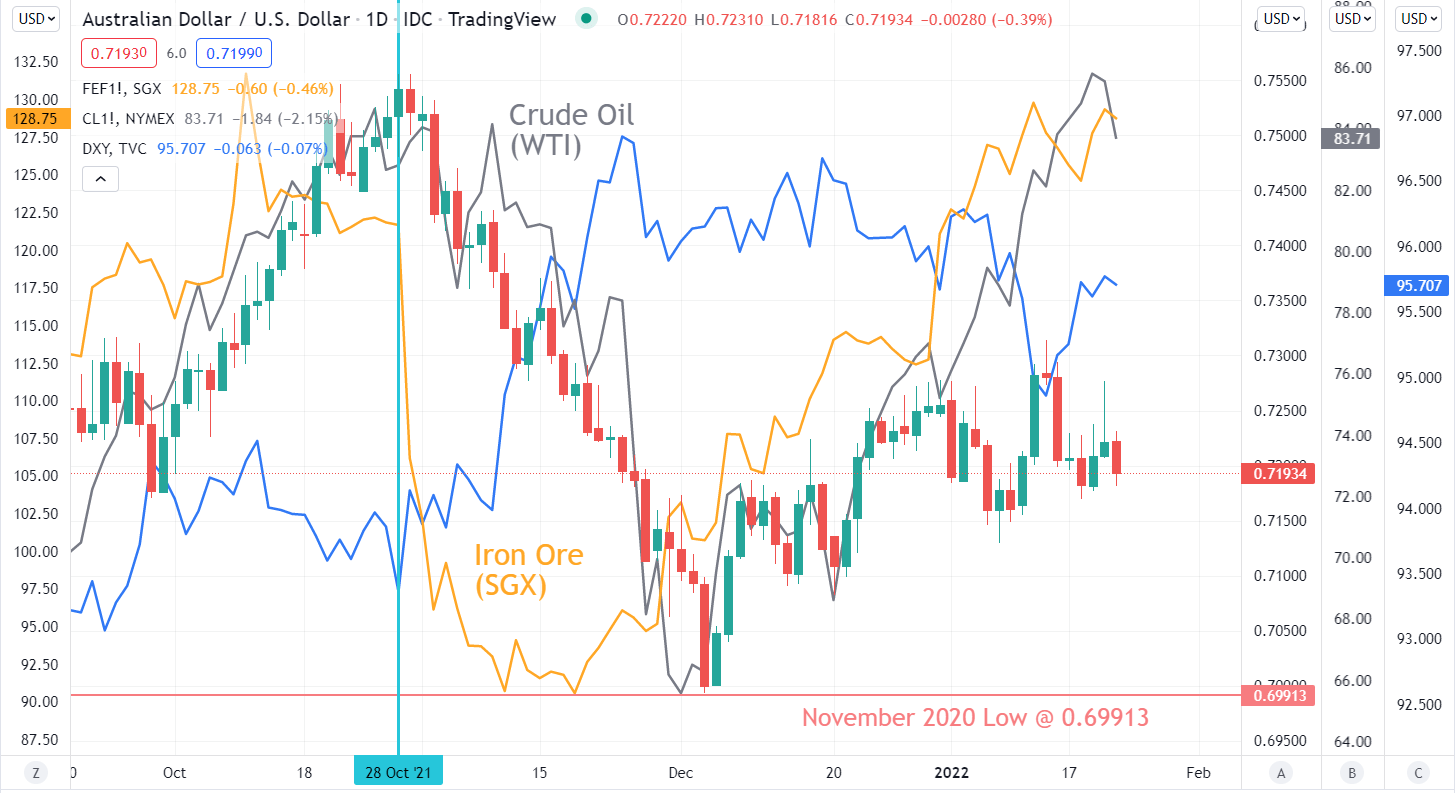

This week saw the Peoples Bank of China (PBOC) ease monetary policy by adding liquidity and cutting several key borrowing rates. A zero case Covid-19 policy and concerning developments in their property sector prompted the action.

This saw iron ore and other ferrous metals charge higher. Energy commodities, gold, copper and aluminium continue to trade at elevated levels, adding to Australian export dollars.

For now, as long as AUD/USD remains in the low 70’s, the terms of trade will likely continue to surge, supporting the domestic economy even further. If the AUD/USD appreciates, then that will cause the terms of trade to mean revert.

Of course, the US Dollar will continue to play a role for AUD/USD and the Federal Reserve will be meeting this week. The market is keenly watching for further guidance on the rate hike timeline and the pace of the Fed balance sheet roll off.

Despite a pullback to end the week, US Treasury yields have soared into 2022, dragging G-10 yields up with them. The 10-year spread of Australian Commonwealth Government bonds (ACGB) to Treasuries has begun widening again.

Further widening of this spread would be supportive of AUD. Elevated commodity prices and a potentially hawkish RBA may also help to underpin AUD/USD.

CHART - AUD/USD, IRON ORE (SGX) AND CRUDE OIL (WTI)

--- Written by Daniel McCarthy, Strategist for DailyFX.com To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter