Receive the DailyFX US AM Digest in your inbox every day before US equity markets open - signup here

US-led airstrikes across three Syrian bases associated with chemical weapons capabilities had been the main headlines from over the weekend. President Trump later indicated that it was ‘mission accomplished’, conseuqently, reducing the risk of more action being required. As such, this has led to a relatively muted affair across financial markets, with US equity futures beginning the week on the front foot, rising a modest 0.5%.

GBP: The Pound is leading the charge this morning, having made a break above 1.43 and is now looking towards the post-Brexit high at 1.4345. Seasonal demand continues to keep the Sterling bulls happy, EURGBP back at 0.8650, however, another test of 0.8600 seems possible. UK data will be in focus, which could provide the green light for the Bank of England raise the bank rate next month, currently OIS markets are pricing in a 73% chance.

NZD: The high-flying Kiwi has hit a slight stumbling block ahead of 0.7400, which coincides with softening commodity prices. Domestic data will come into focus with inflation figures for Q1, Y/Y reading expected to dip from 1.6% to 1.1%, moving towards the lower end of the RBNZ’s 1-3% inflation target range. Renewed buying interest in AUDNZD after finding support last week at 1.0500 has also kept the pressure on NZD.

EUR: Broad Dollar softness has provided a helping hand to its major counterparts, in particular the Euro. This also comes alongside buyers at the 50DMA (circa 1.2330), setting up a near-term test of the psychological 1.24 handle. However, no sign of a breakout of the pairs recent range amid the persistent moderation in Euro-Area economic data.

Oil: Crude oil futures falling some 1% today amid slight unwind of geopolitical risk after President Trump signaled job done after US-led airstrikes, however, escalation could keep oil prices elevated. Eyes will also be on the potential for further sanctions on Russia due to their involvement in Syria, which could be announced either today or later in the week. Elsewhere, Friday saw the release of the latest Baker Hughes rig count whereby oil rigs rose for a second consecutive month to its highest level since March 2015.

DailyFX Economic Calendar: Monday, April 16, 2018 – North American Releases

US retail sales rebounded from a weak start to 2018, printing at a modest 0.6% rise (Exp. 0.4%), limited reaction observed in financial markets however, given that the monthly data is typically volatile and is also not adjusted for inflation. For the rest of the session, traders will eye key speech from slew of Fed members (Kaplanm Kashkari and Bostic). At the US market close, the latest TIC flow will be released, eyes will be on whether China had been reducing its vast treasury holdings.

DailyFX Webinar Calendar: Monday, April 16, 2018

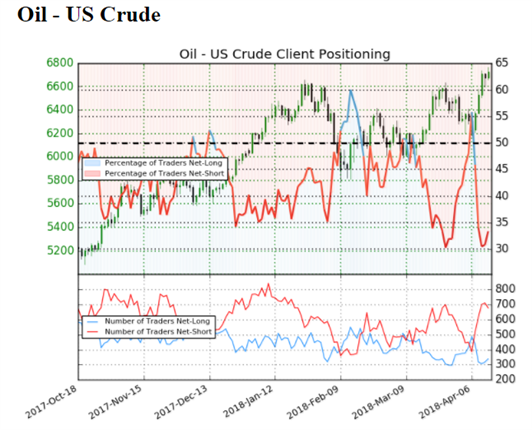

IG Client Sentiment Index Chart of the Day: US Crude Oil

Oil - US Crude: Data shows 33.4% of traders are net-long with the ratio of traders short to long at 1.99 to 1. The number of traders net-long is 4.8% lower than yesterday and 28.8% lower from last week, while the number of traders net-short is 6.0% lower than yesterday and 58.7% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests Oil - US Crude prices may continue to rise. Positioning is less net-short than yesterday but more net-short from last week. The combination of current sentiment and recent changes gives us a further mixed Oil - US Crude trading bias.

Learn more about the IG Client Sentiment Index on the DailyFX Sentiment page

Five Things Traders are Reading

- “No Range Break in Sight Yet for EUR/USD” by Christopher Vecchio, Senior Currency Strategist

- “Key UK Wages and Inflation Data Will Drive Sterling | Webinar” by Nick Cawley, Market Analyst

- “CoT Weekly Sentiment Update – EUR/USD, USD/JPY, Crude Oil & More” by Paul Robinson, Market Analyst

- “Markets Brush Off Geopolitics, Gold Nears Strong Support” by Nick Cawley, Market Analyst

- “Expect a Dow and S&P 500 Break Early Next Week, More Range for USD” by John Kicklighter, Chief Currency Strategist

The DailyFX US AM Digest is published every day before the US cash equity open - you can SIGNUP HERE to receive this report in your inbox every day.

The DailyFX Asia AM Digest is published every day before the Tokyo cash equity open - you can SIGNUP HERE to receive that report in your inbox every day.

If you're interested in receiving both reports each day, you can SIGNUP HERE.

-- Written by Justin McQueen, Market Analyst

To contact Justin, email him at Justin.mcqueen@ig.com

Follow Justin on Twitter @JMcQueenFX