FOMC DECISION KEY POINTS:

- The Fed holds its benchmark rate unchanged at 5.00%-5.25% at the end of its June meeting, in line with expectations

- Policymakers signal a higher peak rate than envisioned in March, meaning the hiking cycle is not over despite today’s pause

- Gold prices erase session gains after the FOMC announcement crosses the wires

Most Read: Japanese Yen Still Battered by BOJ’s Policy Outlier Status

The Federal Reserve today concluded one of its most closely watched and highly anticipated policy meetings, opting to leave its benchmark interest rate unchanged at its current range of 5.00% to 5.25%, in line with market expectations.

The decision, widely telegraphed by some FOMC senior members in recent weeks, was reached by unanimous vote, a sign that policymakers remain on the same page and in agreement on the strategy to tackle inflation and return it to its 2.0% long-term goal.

The move to stay on hold comes as the Fed tries to buy time to better assess the evolving outlook and the cumulative impact of past actions. For context, the bank has hiked at each of its last ten reunions, delivering 500 bp of tightening since March 2022, in what has been one of the most aggressive normalization cycles in decades.

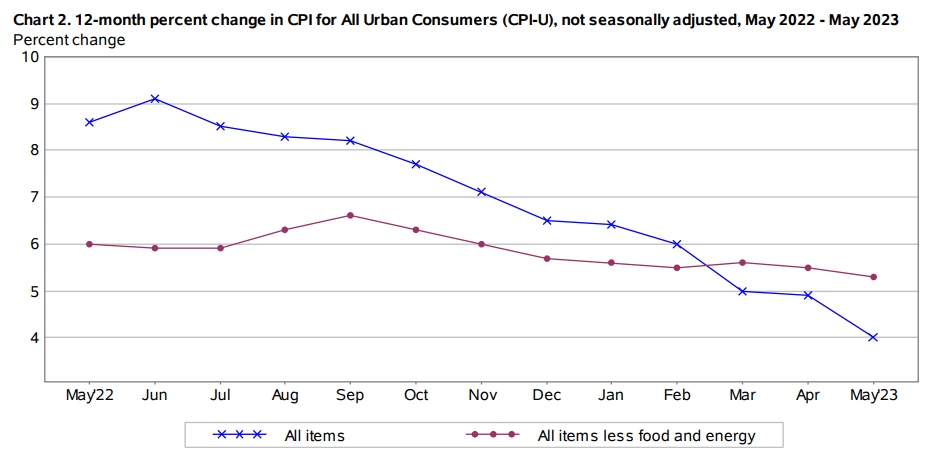

The fast-and-furious tightening campaign appears to be paying off. Headline CPI stood above 8% for much of last year, but now it’s running at 4.0% year-over-year. Although the directional improvement is welcome, it should not be confused with mission accomplished; after all the current rate is still double the target while the core gauge shows extreme stickiness.

HEADLINE AND CORE CPI CHART

Source: BLS

FOMC POLICY STATEMENT

The statement was very similar to the one issued in May, with some minor tweaks. In the June’s iteration, the central bank indicated that the economy is expanding at a modest pace and that employment gains have been robust. It also reiterated that inflation remains elevated.

In terms of the monetary policy outlook, the bank noted that standing pat this month will allow the committee to assess additional information and its implications for monetary policy. The bank also repeated that “in determining the extent to which additional firming may be appropriate”, it will take into account the impact of total tightening, the implementation lag and economic/financial conditions.

Today’s guidance wasn’t overly hawkish, but it clearly retained a hiking bias and an open mind about future steps.

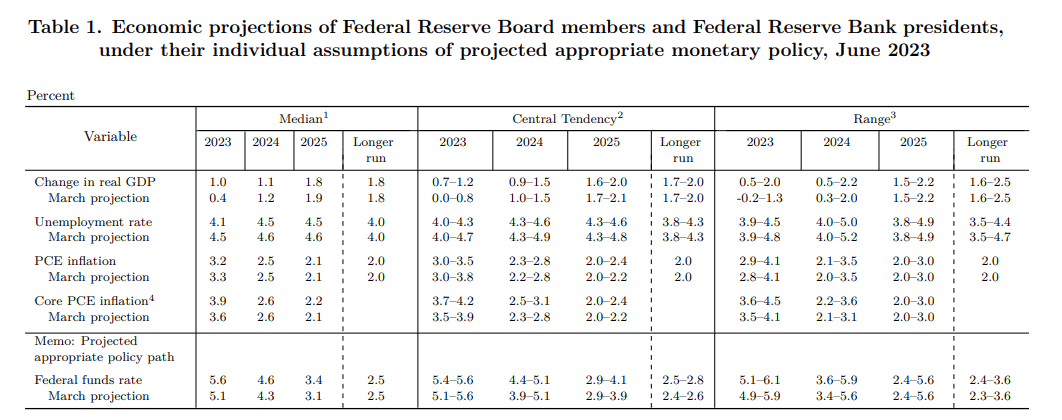

SUMMARY OF ECONOMIC PROJECTIONS

GDP, CORE PCE AND UNEMPLOYMENT RATE

There were significant changes in the June Summary Economic Forecasts (SEP) from the March quarterly estimates.

Delving into key details, gross domestic product, and core PCE forecasts for 2023 were revised upward: the former from 0.6% to 1.0% and the latter from 3.6% to 3.9%. The economic activity outlook suggests no recession on the horizon yet.

For next year, GDP is expected to increase by 1.1%, slightly below the 1.2% assumption three months ago. For its part, the Fed's favorite inflation gauge is seen ticking down to 2.6% in that period, on par with the previous estimate.

Looking at the employment situation, the end-of-year jobless rate was marked down to 4.1% from 4.5%, signaling confidence in the labor market’s ability to withstand tighter monetary policy. For 2024, unemployment is projected to rise to 4.5%, one-tenth of a percent below the March view.

FED DOT PLOT

The dot plot, which maps out Fed officials' estimates of how borrowing costs are likely to evolve in the future, was more hawkish than the version presented in March. That said, the median interest rate projection for 2023 rose from 5.1% to 5.6%. The new peak rate is equivalent to a target range of 5.50%-5.75%, implying two additional 25 bp hikes during the second half of the year.

For 2024, policymakers see the Federal funds rate inching down to 4.6%. Three months ago, the central bank saw rates at 4.3%. Fast forward to 2025, the key rate is expected to fall to 3.4%, less than envisioned in March when the policy-setting outlook was 3.1%. All this points to little appetite to cut rates aggressively over the coming years in the face of sticky inflation.

The table below summarizes the Fed’s new macroeconomic projections

Source: Federal Reserve

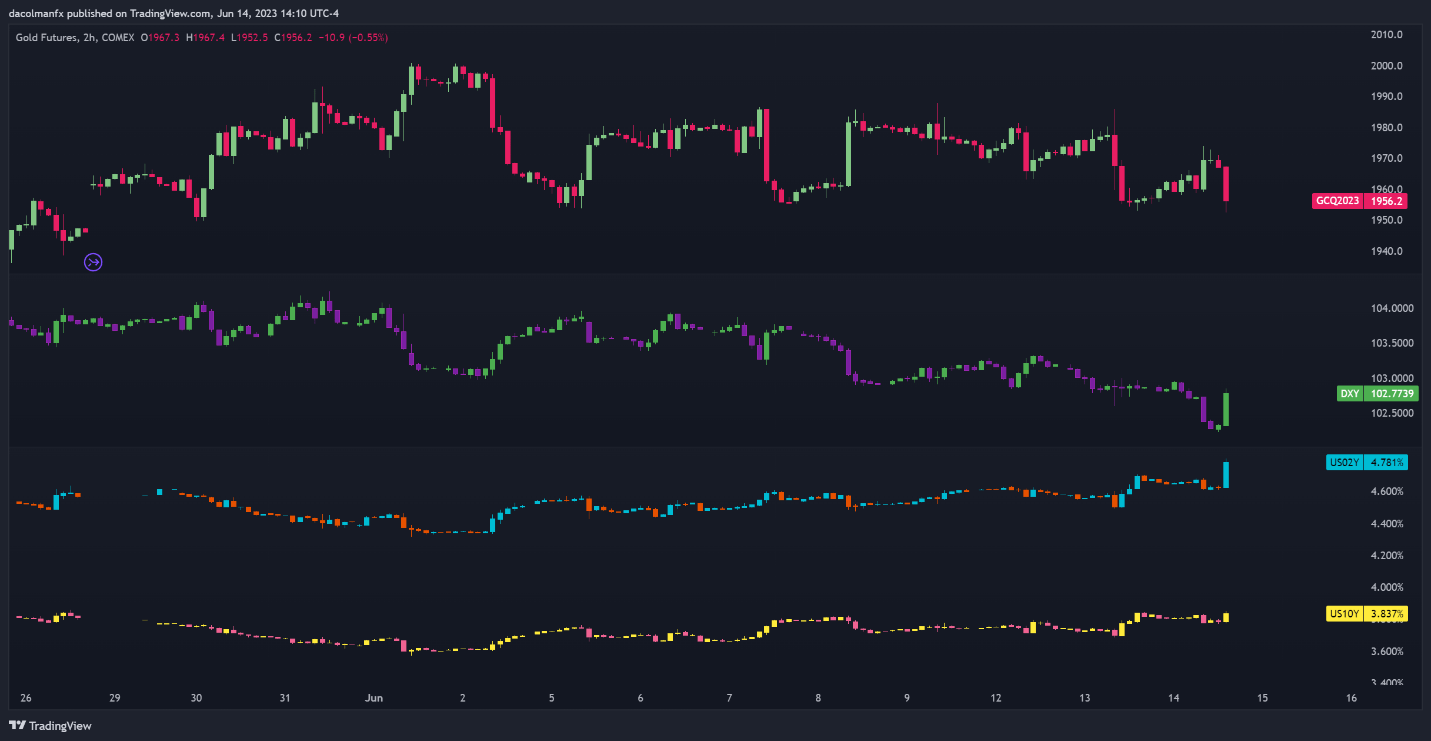

In the immediate kneejerk reaction, gold prices erased early session gains, sinking into negative territory, pressured by the jump in U.S. bond yields and the U.S. dollar’s rebound. Overall, the Fed's steeper tightening path and the prospect of higher interest rates for longer should be negative for non-yielding assets such as precious metals. In any case, Powell’s press conference may offer more insight into the central bank’s monetary policy outlook.

Stayed tune for more in-depth analysis

GOLD PRICES, US DOLLAR, AND YIELDS CHART

Source: TradingView