Resilient labour market conditions and persistent services sector’s prices were not well-received by Wall Street yesterday, as the overnight data called for a hawkish bias in Federal Reserve’s (Fed) policies. A significant beat in the US ADP report (497,000 versus 228,000 forecast) was followed up with continued strength in the services sector, as the US ISM services purchasing managers index (PMI) data came in at its highest reading in four months (53.9 versus 51 forecast). Still-robust labour demand was also reinforced by a renewed expansion in the services PMI employment index (53.1 versus 49.9 forecast).

Given that the Fed has previously expressed their unease over services’ inflation, the persistence in services prices from the ISM data (54.1 versus 53.3 forecast) further challenged the pace of progress in inflation. The overall data brought about an upward surge in US Treasury yields, as rate cut bets have been facing some pushback lately from January to May next year. Notably, the US 10-year has crossed the 4% mark for the first time since March this year.

While the ADP has not been a good predictor for the US non-farm payroll historically, some signs of a resilient labour market still raises the odds for a stronger US job report today. Over the past one year, the US job report has outperformed market expectations on 11 out of 12 occasions, with a notable reacceleration viewed over the past two months. Forecasts for June are for a 200,000 increase, with unemployment rate remaining unchanged at 3.7%. Another set of better-than-expected readings may support hopes of a soft landing but could also pressure the Fed to do more, with eyes on the wage inflation figure as well.

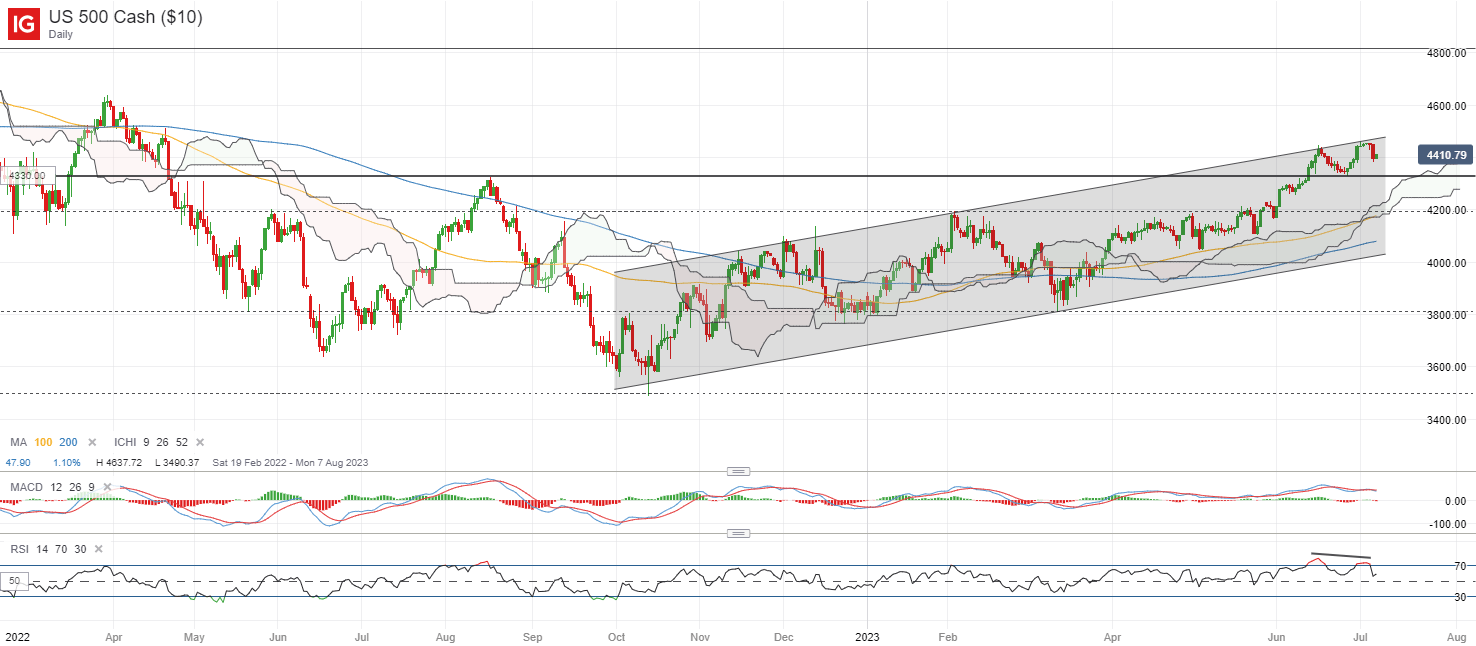

The S&P 500 has met some resistance at the upper trendline of an ascending channel pattern for now, with lower highs on daily RSI pointing to moderating upward momentum. Near-term overcrowded sentiments may be reflected with a reversion in the Fear and Greed Index back to ‘extreme greed’ territory late last week, although seasonality in July remains in favour for a continuation of the upward trend, which leave any formation of a higher low on watch. For now, further downside will likely pave the way for the formation of a double-top pattern, with the 4,330 level serving as the crucial neckline to hold for the bulls.

Source: IG charts

Asia Open

Asian stocks look set for a downbeat open, with Nikkei -0.45%, ASX -1.86% and KOSPI -1.02% at the time of writing, largely tracking the negative handover from Wall Street. A 3% retreat in the Hang Seng Index in the yesterday’s session seems to reflect investors’ anxiety over China’s consumption-led recovery, further amplified by Goldman Sachs’ recent downgrade of its top lenders and some unnerves around US-China relationship. The Hang Seng Mainland Banks Index is down more than 9% over the past week.

The regional economic calendar this morning saw a surprise jump in Japan’s average cash earnings (2.5% versus 0.7% forecast) in May. With subdued wage increases looked upon as a basis for ‘transitory’ inflation by the Bank of Japan (BoJ), recent pull-ahead in wage pressures seems to renew bets for a quicker policy shift. That said, a continued contraction in real wages for the 14th consecutive month and a sharper-than-expected decline in household spending (-4% versus -2.4% forecast) may still call for some reservations.

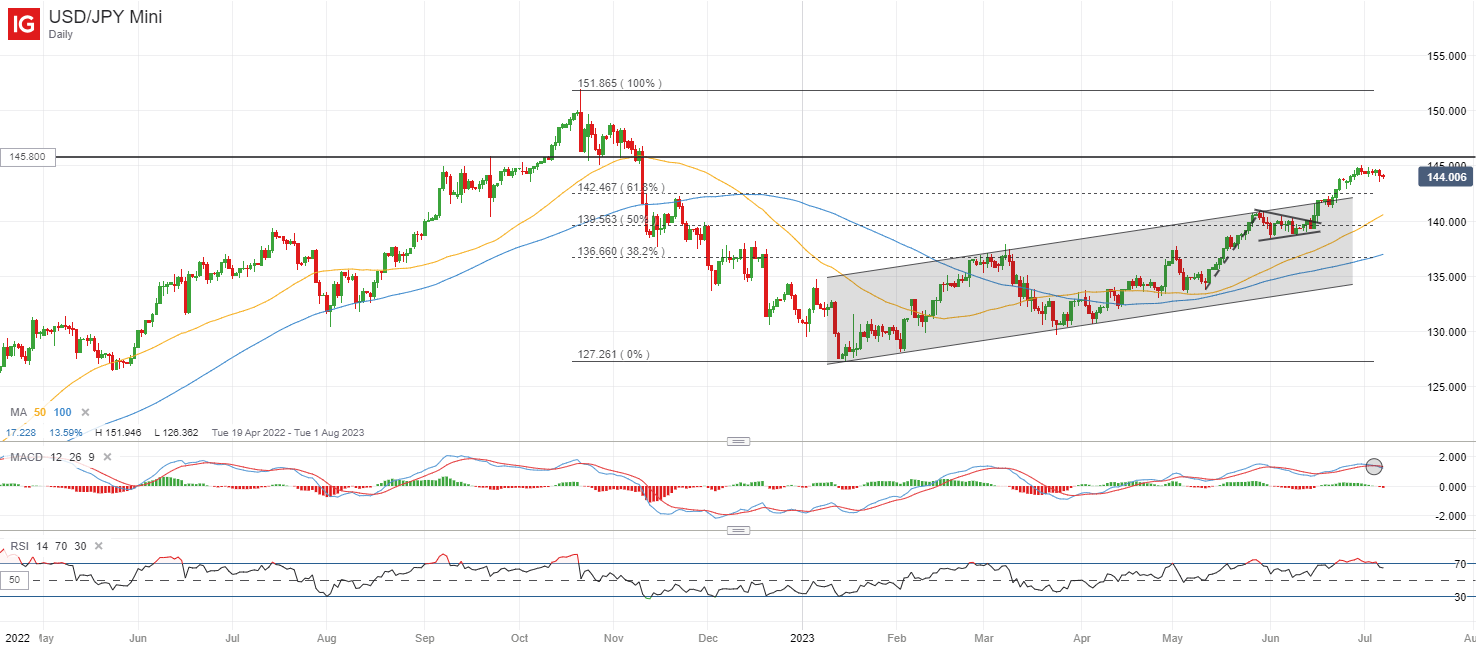

The USD/JPY has been consolidating around the 145.00 level lately, as it nears a previous level of intervention by the BoJ back in September 2022. While a bearish crossover on MACD and moderating RSI from previous overbought levels points to some near-term exhaustion, the pair tends to track the US-Japan 10-year yield differentials closely over the past year, with recent surge in the US 10-year yields to its four-month high potentially providing some support for the pair. The upward trend remains in place for now, with the formation of higher highs and higher lows since the start of the year, with any retracement placing the 142.50 level on watch as immediate support.

Source: IG charts

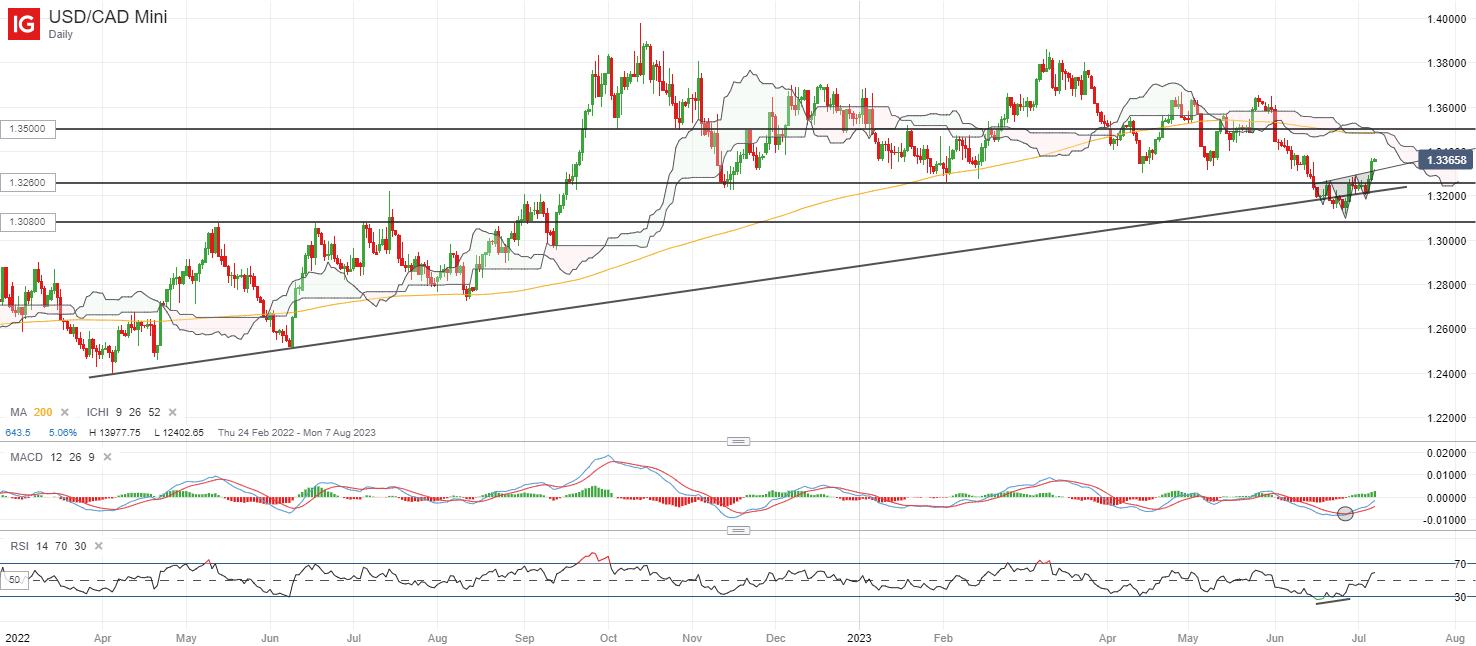

On the watchlist: USD/CAD on watch ahead of US and Canada’s job report today

Following a brief breakdown of the 1.326 level of support last month, the USD/CAD has shown some resilience lately, gaining by 1.2% over the past week. A minor inverse head-and-shoulder formation seems to be in place since mid-June this year, with a recent break above the neckline yesterday potentially putting the 1.350 level on watch for any retest, as increasing RSI and MACD point to building upward momentum.

Much will be determined by the job report releases from both the US and Canada later today. Thus far, policymakers from both ends have expressed their unease over recent labour market resilience, which calls for a hawkish tilt in their respective policy guidance. Any divergence in labour market conditions will be on watch, with any softer labour data likely to translate to some weakness in its currency. For the USD/CAD, any downside may leave the 1.326 level back on the radar for near-term support, where an upward trendline support stands.

Source: IG charts

Thursday: DJIA -1.07%; S&P 500 -0.79%; Nasdaq -0.82%, DAX -2.57%, FTSE -2.17%