Talking Points

- Headline November US CPI comes in at expectations at +2.2% y/y, as did the core CPI reading at +2.2% y/y; headline inflation was unchanged month-over-month.

- Disinflation in headline inflation may continue: the US Dollar is near its yearly high and energy prices have collapsed by nearly -40% since the start of October.

- The US Dollar slumped following the release as rate hike odds for 2019 and 2020 continued to suggest that the Fed will downgrade its glide path and forecasts in its Summary of Economic Projections next week.

See the DailyFX Economic Calendar and see what live coverage for key event risk impacting FX markets is scheduled for next week on the DailyFX Webinar Calendar.

Nearly halfway through the week, the first important US economic release since Friday’s jobs report has knocked the US Dollar lower. Headline November US CPI met expectations perfectly, coming in at +2.2% from +2.5% previously (y/y). With average hourly earnings in at +3.1% y/y, real wage growth continues to trend positive in the United States for the fourth consecutive month. The annualized core inflation came in at +2.2% y/y as expected.

The inflation data come just a week ahead of what should be a very interesting Federal Reserve policy meeting. We’ve heard from key players like Chair Jerome Powell and Vice Chair Richard Clarida in recent weeks discuss how close the Fed is to achieving its ‘neutral rate’ theoretically keeps an economy from overheating or underperforming – the Goldilocks level, if you will), and in turn, suggest that a return to a data-dependent policy stance, away from the preset policy course of one 25-bps hike per quarter, is appropriate.

Given the context of the DXY Index near its yearly high and energy prices down nearly -40% since the start of October, it would appear that further evidence of disinflation, mirroring the results in today’s November US CPI report, are set to materialize in the coming months. This should force the Fed to reconcile its projected interest rate glide path with what markets are pricing: the Fed sees one more 25-bps hike this year, three in 2019, and one in 2020; markets are pricing in one more this year (74% chance), one in 2019 (56% chance by September 2019), and a cut in 2020.

Here are the data driving the US Dollar this morning:

- USD Consumer Price Index (NOV): +2.2% as expected, from +2.5% (y/y).

- USD CPI ex Food & Energy (NOV): +2.2% as expected, from +2.1% (y/y).

See the DailyFX Economic Calendar for Wednesday, December 12, 2018.

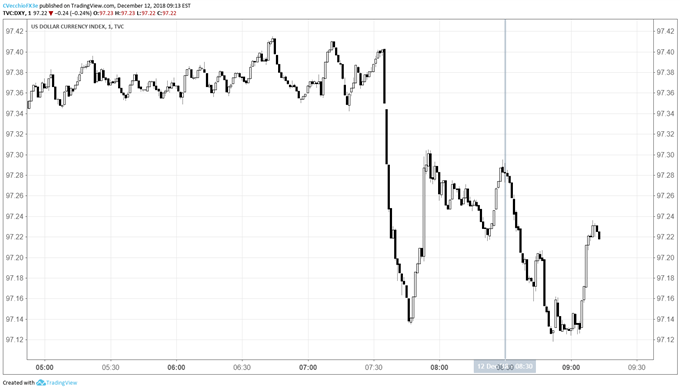

DXY Index Price Chart: 1-minute Timeframe (December 12, 2018) (Chart 1)

Following the inflation report, the US Dollar (via the DXY Index) resumed its intraday downtrend, piggybacking on losses spurred on by Brexit headlines and their impact on GBP/USD. The DXY Index initially dropped from 97.28 to as low as 97.12 following the release, but was trading back higher at 97.22 at the time this report was written.

Read more: DXY Index Holds Near Yearly Highs Ahead of UK No-Confidence Vote, US CPI

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX

View our long-term forecasts with the DailyFX Trading Guides