US Dollar, Crude Oil, Gold - Talking Points

- US Dollar resumed strengthening yesterday but has slipped today

- The Fed reminded markets of their intention and yields responded

- If Fed Chair Powell is hawkish today, will that drive the DXY (USD) Index up?

The US Dollar is treading water so far today after massive gains across the board thanks to Fed commentary for higher rates raising the prospect of a hawkish Fed Chair later today.

Yesterday, Atlanta Fed President Raphael Bostic highlighted that the tight labour market seen in Friday’s data might mean that the peak in rates could be higher than where the market is currently pricing.

Futures and swaps markets are now pricing a 2023 peak in US rates above 5.10%, up from below 4.90% last week.

The comments lifted Treasury yields across the curve with the short end seeing the largest bump. The benchmark 2-year note fell just short of 4.50% in the US session and all bond yields have eased a touch in the Asian session so far today, in line with a softening US Dollar.

Wall Street finished their day lower with the Nasdaq notching a 1% decline. APAC equities have had a quiet day with Australia’s ASX 200 slightly in the red, Japan’s Nikkei 225 fairly flat and Chinese markets scratched out small gains

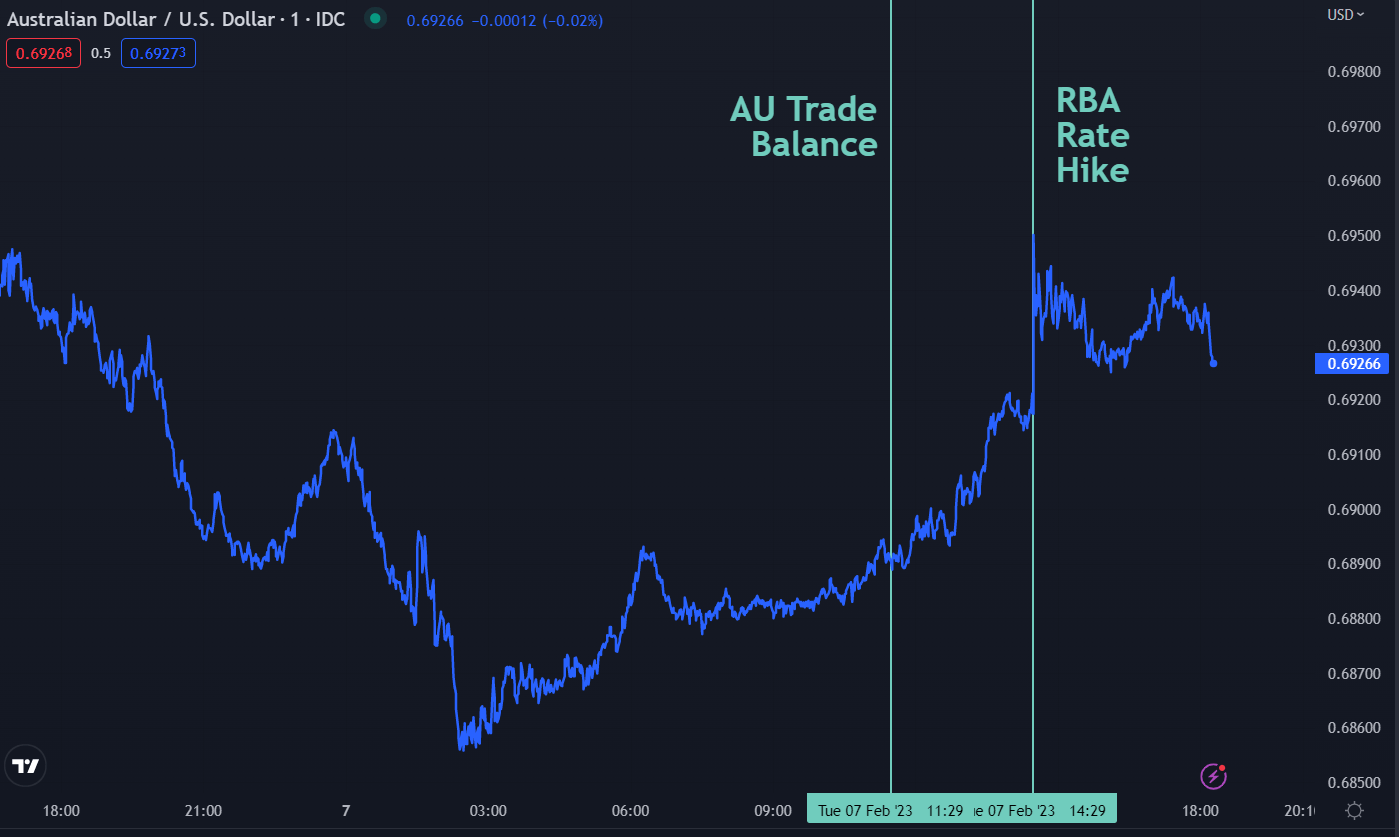

The RBA hiked rates by 25 basis points today in a somewhat pastiche approach to monetary policy after the Fed’s re-acceleration toward hawkishness. The move boosted the Aussie Dollar and has been the biggest gainer against the greenback.

It is being reported that Washington is planning to slap a 200% tariff on Russian Aluminium in the next week or 2.

The Japanese Yen is firmer after solid wage data raised speculation that the Bank of Japan might reconsider its ultra-loose monetary policy stance.

Crude oil is slightly firmer with the WTI futures contract near US$ 74.75 bbl and the Brent contract is a touch above US$ 81.50 bbl. Gold is steady at around US$ 1,875 an ounce at the time of going to print.

In other news, the New York Stock Exchange (NYSE) has agreed to pay 60% of claims from the trading glitch last month.

The focus later today will be Fed Chair Jerome Powell’s speech at the Economic Council in Washington. The very strong labour market, and Bostic’s comments yesterday might have laid the groundwork for stronger hawkish rhetoric from the chief rate setter.

The full economic calendar can be viewed here.

DXY (USD) INDEX TECHNICAL ANALYSIS

The DXY Index is testing the upper band of an ascending trend channel today after it recovered from a seven-month low seen last week.

The 55-day simple moving average (SMA) is just above the trend line and may offer resistance.

Further resistance could be at the prior peaks of 105.63, 105.82, 107.20 and 107.99.

On the downside, support may lie at the breakpoint of 101.30 or down at the previous lows of 100.82, 9957 and 99.42.

--- Written by Daniel McCarthy, Strategist for DailyFX.com

Please contact Daniel via @DanMcCathyFX on Twitter