S&P 500, FOMC, BOE, GBPUSD, NFPs and USDCAD Talking Points:

- The Market Perspective: USDJPY Bearish Below 146; EURUSD Bullish Above 1.0000; Gold Bearish Below 1,680

- The FOMC’s rejection of a quick halt to its hawkish path has carried over to Thursday trade with a continued slide from the S&P 500 and a greater contrast to the BOE’s own hike

- Top event risk through Friday is the October NFPs with the recognition of economic trouble and financial imbalance exposing raw trading nerves

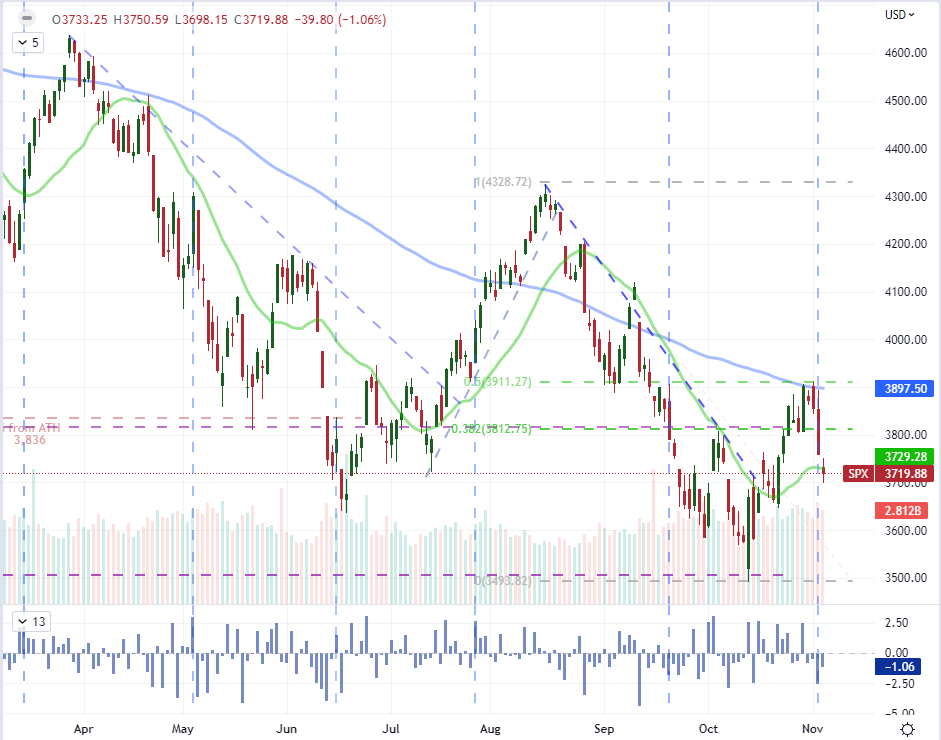

S&P 500 and Risk Trends are Still Feeling the Fallout of the Fed’s Hawkishness

The aftereffects of the FOMC rate decision on Wednesday were carrying over to market trade this past session, and it is likely that we see the fallout for some time going forward – though whether or not we appreciate the steer depends on our macro radar. For general risk trends, my preferred measure sentiment – convenient, though far from perfectly indicative – the S&P 500 suffered an extension of the previous day’s post policy event slide. The US index opened to a -0.7 percent gap to the downside following Wednesday’s -2.5 percent loss with the day ultimately culling -1.1 percent in value. That is the fourth consecutive trading session’s slide with a close back below the index’s 20-day moving average. In terms of conviction, this wasn’t a particularly intense decline given recent history nor does it invite critical technical progress. From a ‘breadth’ perspective, other measures of sentiment (global indices, emerging market assets, carry, etc) were somewhat mixed with the same lack of total conviction. There seems a weight to the speculative bias, but a total capitulation to the bears is still beyond the current landscape. Perhaps today’s NFPs can tip that balance – though I am not holding my breath for a definitive market move.

Chart of S&P 500 with 20 and 100-Day SMAs, Volume and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

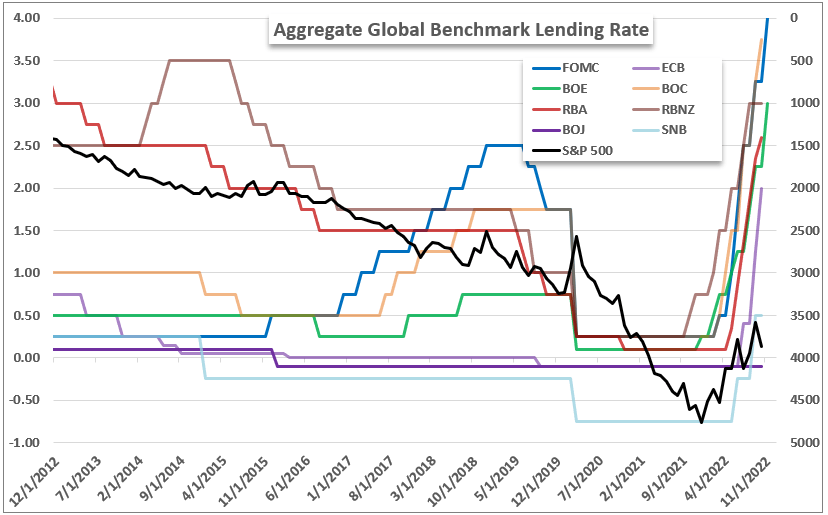

For fundamental motivation, it would be far to say that the global markets are still drawing heavily on monetary policy as an influence. From the systemic perspective that tighter policy is an afront to speculative largesse to the relative considerations of one central bank outpacing another, we can tap into very different market influences. Following up on the RBA’s 25 basis point (bp) hike on Tuesday and the FOMC’s 75bp increase Wednesday, the Bank of England (BOE) increased its benchmark rate by 75bp – the biggest jump in 33 years – this past session. That lifts yet another major country’s baseline lending rate to the 3 percent market. The throttling of ‘easy money’ driven growth continues. Extreme accommodation played a heavy role in the market’s gains up through the end of this past year and the subsequent withdrawal of support is having the commensurate impact on stretched benchmarks. Below is a chart of the major central banks’ benchmark rates overlaid with an inverted S&P 500 chart. While balance sheets bolstered by QE may help buffer the comedown, this is an ‘negative relationship’ that is likely to persist.

Chart of the Major Central Banks’s Benchmark Rates Overlaid with an Inverted S&P 500

Chart Created by John Kicklighter

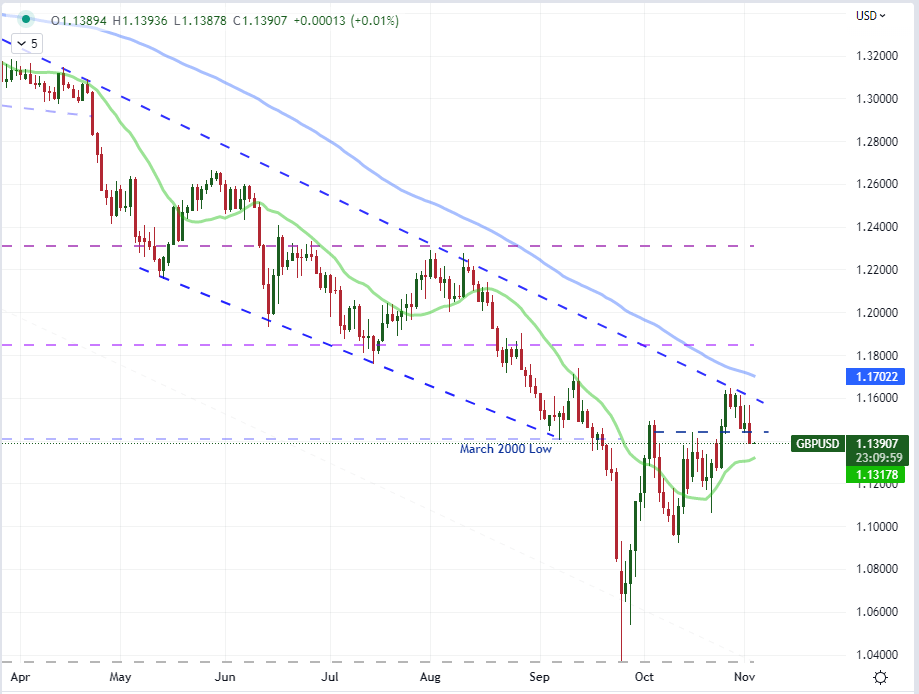

So Why did GBPUSD Drop with a 75bp BOE Hike?

If you are evaluating the macro market from a linear or academic perspective, the bearings from cable (aka GBPUSD) this past session don’t really line up. The Bank of England (BOE) rate decision was one the top events on my docket, and it didn’t disappoint for historical precedence. Meeting expectations, the group announced a 75bp rate hike, which is the largest single-meeting increase in the benchmark in 33 years. Without any kind of speculative interpolation, this would have been a very hawkish and likely bullish market view. However, the Sterling dropped sharply after the event with GBPUSD suffering a particularly acute decline through short-term support. What is the logical disconnect here? As exceptional as the hike was, the markets had anticipated the outcome. Therefore, the aspect of the event that was not accounted for by market observers was the deepening concern around the UK’s economic trajectory and what it means for the future course of monetary policy. That is quite the contrast from the (likely optimistic) outlook from the FOMC.

Chart of GBPUSD Overlaid with 20 and 100-Day SMAs (Daily)

Chart Created on Tradingview Platform

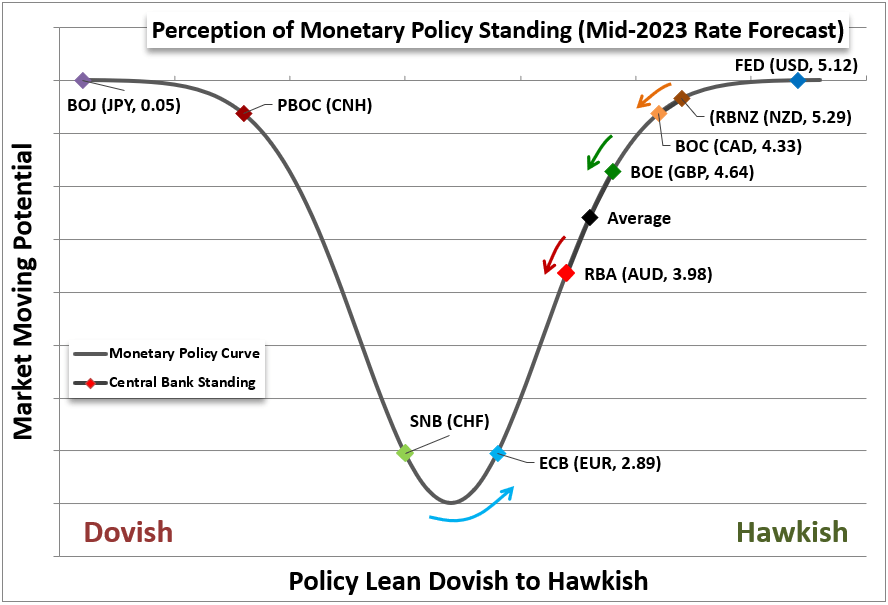

To illustrate the perspective of monetary policy and its influence in relative strength considerations, as with the FX market, it is worth looking out into the future. Current benchmark rates create a very clear hierarchy of carry standings, but markets are forward looking in nature. We find speculative appetites prize forecasts – whether they are realized or not is a matter of projections meeting realized event risk. Below is a chart of my assessment of the major central banks’ relative monetary policy stance with the forecast for mid-2023 (June for most) derived from overnight index swaps. As can be seen in that forecast, the BOE rate for the middle of next year stands around half a percentage point relative to the US rate over the same time frame. It is worth noting that the forecast for the BOE’s rate by that same time was over 150 basis points higher less than two weeks ago. That goes a long way towards evaluating the Sterling’s struggle.

Chart of Relative Monetary Policy Stance Perception with Mid-Year 2023 Rate Forecasts

Chart Created by John Kicklighter

What’s on Tap for Friday and Beyond

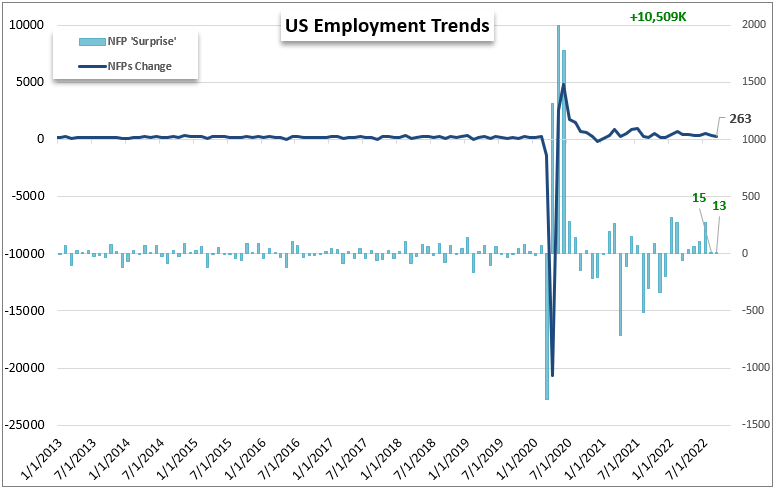

Shifting the focus forward, it should not be controversial to suggest that the October change in US nonfarm payrolls (NFPs) is our top fundamental listing. While there are other indicators of note on tap, there isn’t anything that I believe could compete with the global ubiquity of the US labor report. I’m interested in the details of the report as it pertains to the larger trend of the economy’s health, but speculative appetites are likely to hang on the headline readings. This serious has ‘beat’ expectations for six months running but the last two months have presented very moderate outperformance relative to consensus forecasts. The economist forecast is for a net 200,000-job increase in payrolls, but it is worth noting that the White House Press Secretary this past session suggested the government was expecting a 150,000 monthly average for the immediate future. I don’t like to cater to conspiracy theory, but the White House has been privy to early insight on economic figures in the past and mid-terms are next week. Discounting expectations before a ‘miss’ would make sense to political strategists.

Chart of the NFPs (Monthly)

Chart Created by John Kicklighter with Data from BLS

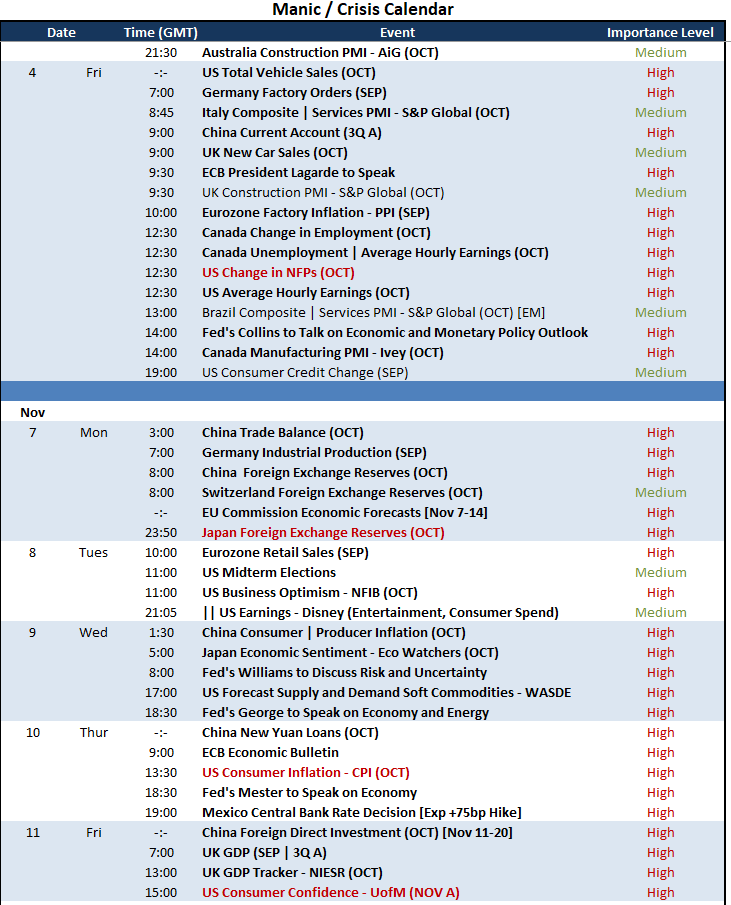

Looking beyond the US employment data, there are other US events to mind including the first official Fed member remarks from Susan Collins. She will be speaking on the economic and monetary policy outlook at 14:00 GMT. There is also event risk Friday that falls outside the United States’ sphere of influence. Most notably, Canada will release its own employment data at the same time as the NFPs hit. Then there is also the Canadian Ivey manufacturing report. Shifting further out to a forecast for next week, the docket will likely continue to prize events that connect to systemic themes – like the US CPI release – but I will go into more detail on what is ahead tomorrow.

Critical Macro Event Risk on Global Economic Calendar for Next 48 Hours

Calendar Created by John Kicklighter

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team