Nasdaq 100, Dow, Dollar, Recession, FOMC and EURUSD Talking Points:

- The Market Perspective: USDJPY Bearish Below 146; EURUSD Bullish Above 1.0000; Gold Bearish Below 1,680

- The significant hit to FAANG earnings this week proved a top macroeconomic weight for those tracking broader risk trends, but priorities are likely to shift ahead

- Top marks for market-moving potential in the week ahead goes to the FOMC decision; but don’t underestimate the BOE and RBA updates, Eurozone GDP and NFPs among other releases

FAANG Earnings Have Hobbles Risk Appetite from the Inside

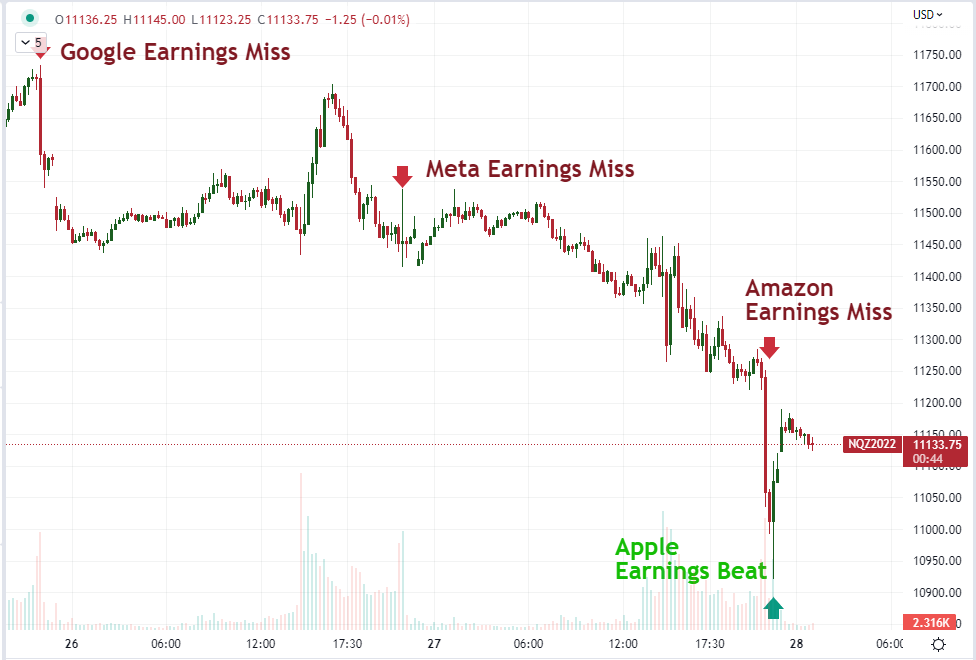

The momentum behind benchmark ‘risk’ assets has been seriously undermined this past week by the uneven performance of FAANG earnings. Though we have navigated event risk that speaks to serious problems for economic activity and financial stability, it was the profitability of the few major US tech companies that seemed to ultimately rouse the market to life. Avalanches can originate near the peak of the speculative mountain, so it is not totally unprecedented; but confidence-from-complacency is such a dominant feature of our landscape. Looking ahead to the docket, seasonal norms and backdrop for the week ahead; priorities are likely to shift to the macro considerations of recession risk and monetary policy distortion. That said, the fallout from corporate performance should not be ignored in the broader speculative equation. In this past week, the afterhours activity of the exposed Nasdaq futures reflected the serious swoon in confidence as the top names announced their numbers. Google’s distinct shortfall started things off while Meta’s miss seemed to fall short of full-market inference. Amazon’s miss on EPS and revenue led to the -14 percent (and peak -21 percent) drop after hours AMZN.

Chart of Nasdaq Futures with Volume Indicating GOOG, META, AMZN, AAPL Earnings (15 Minutes)

Chart Created on Tradingview Platform

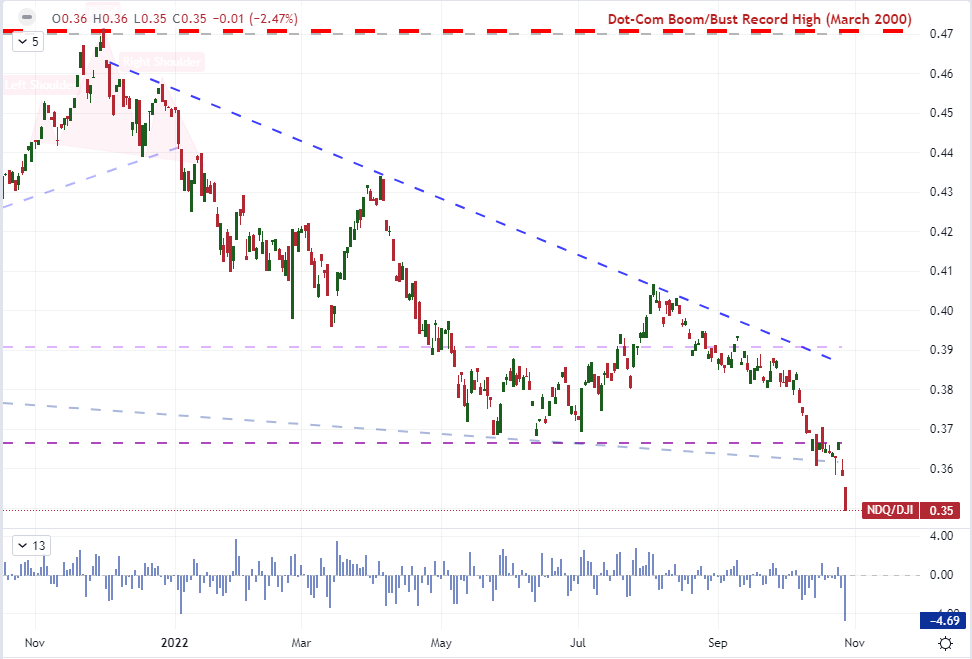

The concentrated influence of the largest market-cap tech stocks isn’t exactly indicative of the foundation of the global capital markets and sentiment, but it does represent an important insight into speculative perspective. Given the swell in performance for the FAANG members – and subsequently meme stocks – following the impact of the pandemic, the post economic lockdown period was defined by the unusual distortion of lockdown-motivated stimulus efforts. Those same infusions are now being unwound in a bid to combat inflation, but speculative appetite does not seem willing to cede control. That will be a holdout that seriously challenges investors’ commitment. One of my preferred measures of focused risk reflection is the Nasdaq 100 to Dow ratio. While there has been a bounce in both of those measures individually, the isolated ‘risk’ perspective of the comparison has seen the ratio drop to its lowest level since April of 2020 following the biggest daily drop since November 2020 through Thursday.

Chart of Nasdaq 100 to Dow Average Ratio with 20 and 200-Day SMA and Gaps (Daily)

Chart Created on Tradingview Platform

How Well is the Market Positioned: Volatility and Event Risk

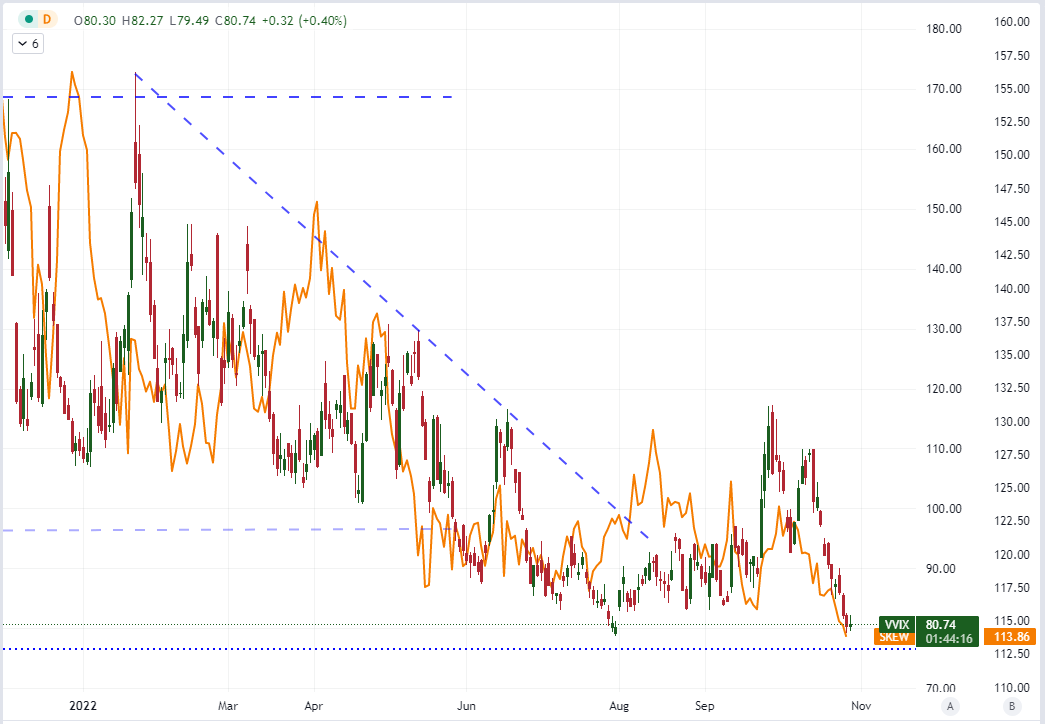

After a significant drop in risk-leaning assets, like we have seen this past week, it is tempting to suggest that a bottom is near-at-hand. However, conviction for such a low point should not be taken at a face value. Despite the volatility in the benchmark assets discussed above, there has been none of the shake out that we would expect to see from implied volatility readings. I consider a surge to 50 a ‘capitulation move’ that could act as the stand in for an underlying improvement in fundamentals to guide the bulls back into the market, but we have stayed far away from that high water mark. In fact, the general activity (also considered the ‘fear’) gauge has generally slid these past weeks. What more, the more extreme measures of uncertainty have started to push to flagrant levels of inactivity. The VVIX ‘volatility of volatility’ index dropped to meet levels that represent the lows of anticipation stretching back to July 2019. Meanwhile, the so called ‘black swan’ measure in the SKEW index hit October 2019 lows. I don’t consider this reassuring. In fact, it is a point of serious concern for me given the serious fundamental backdrop with which we are contending.

Chart of VVIX Volatility of Volatility Index Overlaid with the SKEW Index (Daily)

Chart Created on Tradingview Platform

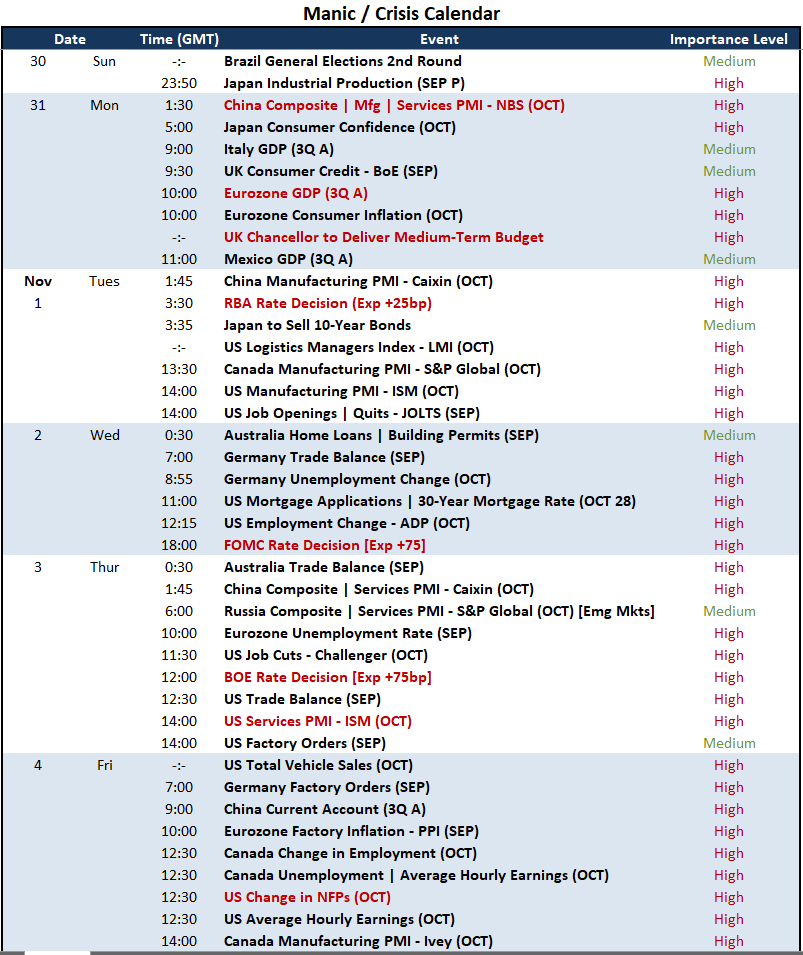

For scheduled event risk, the coming week will see our attention shift. What we were dealing with this past week was a continuous feed of meaningful event risk that was subsequently overridden for market moving potential by anticipation of the next high-profile event (Apple overriding Google earnings or US GDP subverting the US consumer confidence report). In the week ahead of us, we are likely to see a significant downgrade in the impact of corporate US earnings given that the largest (tech) market cap companies have already announced their performance. That will tarin the spotlight back on the more systemic matters, namely recession risks and the fallout from monetary policy imbalances. On growth, the US 3Q GDP’s better-than-expected 2.6 percent annualized reading hasn’t soothed the market on fears for what lies ahead for the largest economy in the world. Where the BEA’s growth update is a lagging indicator, there are a string of updates from the ISM activity figures to October NFPs ahead that will present a more timely update for the world’s largest economy. Meanwhile, the Eurozone GDP, Chinese PMIs and myriad of sentiment surveys will give global perspective.

Critical Macro Event Risk on Global Economic Calendar for Next 48 Hours

Calendar Created by John Kicklighter

Monetary Policy Top Theme and EURUSD Top Pair Ahead

Moving into the new trading week, the fundamental priorities will shift meaningfully. While the proximity of a global recession is an ever-present threat, it remains far too abstract to represent a progressive influence on speculative markets…until the fire is undeniable. In the meantime, monetary policy will provide its own fundamental upheaval. This past week has offered up a disappointment from the Bank of Canada (50 versus 75 bp hike), a retreat from the Euro despite an accelerated 75bp European Central Bank hike and an unrelentingly dovish Bank of Japan hold to its out-of-touch yield curve control. The Federal Open Market Committee (FOMC) meeting ahead is the top individual monetary policy listing, but don’t underestimate the bigger picture shaped by the Reserve Bank of Australia and Bank of England as the world starts speculating that the world’s largest central banks may have very well peaked in their hawkish monetary policy drive.

US 10-Year to 3-Month Treasury Yield Spread (Daily)

Chart Created on Tradingview Platform

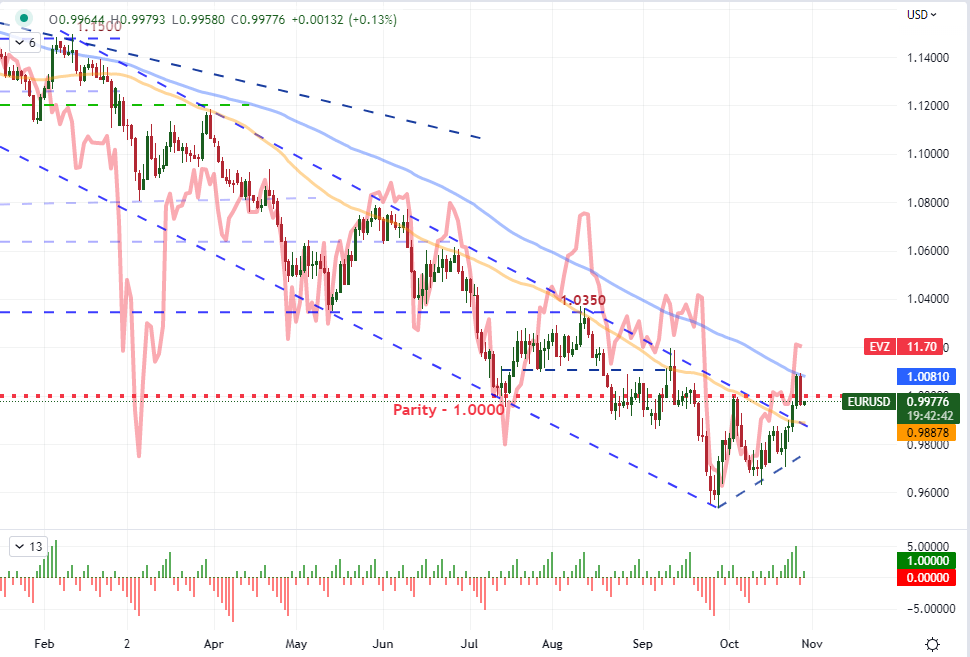

For a standout moving forward, I believe EURUSD deserves closer observation by global macro traders. Despite the ECB’s announcing that it was hiking its benchmark rate an incredible 75 bps this past week, the market (aka the Euro) ultimately seemed disappointed by the news. A drop from the benchmark currency pair back below the parity mark (1.0000) on the news, there must have been some serious anticipation at work. It is possible that the upcoming FOMC event is met with the same ‘anticipation’ distortion, but there is much more seemingly at work with this pair than just relative yield potential. Safe haven and growth trajectory seem to play just as significant a role in dictating the exchange rate.

Chart of EURUSD Overlaid with Inverted Euro Volatility Index Overlaid (Daily)

Chart Created on Tradingview Platform

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team