Talking Points:

- The Federal Reserve's hawkish policy bearing is exceptionally unique - a risk that the Fed itself mentioned in its minutes

- Maintaining the aggressive forecast of a hike in December and 3 in 2019 requires more than just inflation

- If conditions are ideal to maintain hikes, it will likely curb the Dollar's advantage while slowing would certainly earn the same

The Fed's Hawkish Policy is Extraordinary - In Good and Bad Ways

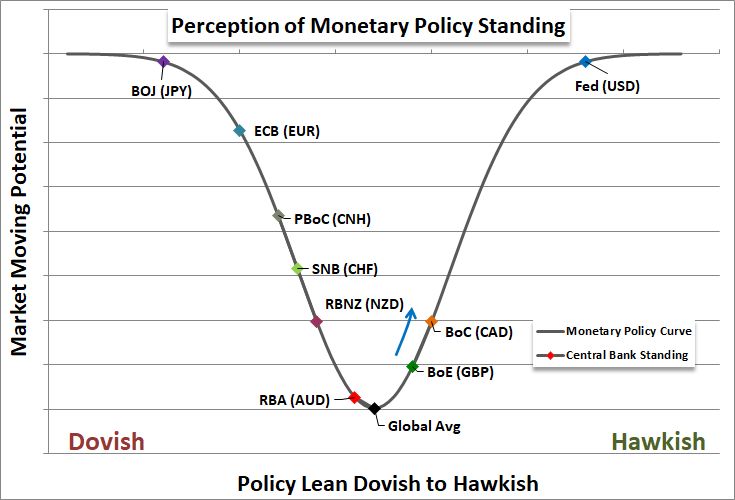

In the rank of monetary policy amongst the major currencies and central banks, there is a clear and undisputed leader: the Dollar/Federal Reserve. The group leveled out its extreme dovish policy between 2013 and 2014 when it reduced its QE (quantitative easing) asset purchases. The first rate hike by the group came on December 2015 and a remarkably gradual pace of further tightening has followed. Looking across its peers - from the European Central Bank to the Bank of England to the Reserve Bank of Australia - we can appreciate just how unique this charge towards normalization. There are few instances of even a single rate hike in this decade-long cycle; and where we find those rare instances, there is no intent at consistency. When we overlay this fundamental state over currency valuation, the Dollar is exceptionally unique. It is the very definition of carry currency given the level of yields set by a range from Swiss Franc (negative benchmark) to the New Zealand Dollar (a 1.75 percent benchmark). Over the years, this distinct policy effort has earned the Greenback considerable lift. However, more recently as the Fed's pace has accelerated and grown more certain, the currency's climb has become more uneven. Notably, through 2017 as the Fed hiked its key range three times, the Dollar notably suffered a consistent slide against its primary counterpart (the ECB) even though speculation of its first move to tighten was still very distant. This speaks to the status of actual carry trade, the dependency on speculative appetite, the role of speculation and the shifting sands in fundamental motivation. The FOMC (Federal Open Market Committee) meeting minutes reminded FX traders of the importance of context. As hawkish as the group may be relative to more restrictive rates, the actual return is historically very low. That contributes to the fading bullish influence the theme is able to carry, but the premium remains such that it can absolutely sink the currency should its advantage falter.

Policy Spectrum Chart

Difficulties in Maintaining a Neck-break Monetary Policy Pace

Given the influence of the Fed's monetary policy stance over the US Dollar's performance, it follows that the theme can both help lift the currency further as well as sink it should the favorable tide roll out again. This relationship is particularly interesting to consider given the complications a hawkish policy regime has faced in earning bulls further gains. In assessing the contribution Fed policy can afford (or inflict) on its local currency, we should consider all the required elements to merely keep the status quo. In the dual inflation system the US central bank follows, the most important and underpriced element in the mix is inflation. Looking forward, price pressures look very likely to build moving forward regardless of the thick or thin growth or financial performance considerations. Yet, the focus on inflation comes only when those two aforementioned considerations are not interfering. Employment is the metric used to qualify the growth leg of the dual mandate, but cues of trouble come far earlier from other measures. And, as for the health of the financial markets, it is difficult to miss the uncategorized third measure. When Ben Bernanke was back at the helm, he stated outright that a presumed 'wealth effect' aspect was assumed in supporting the economy. Where growth plateaued early and inflation has been slow to pick up, asset prices have soared readily and extensively. Further, given the conflict between complacency and a growing wealth of systemic risks such as trade wars, assuming quiet is presumptuous at best. The IMF's growth forecasts last week have lowered the projection for US and global activity levels. Even if everything remains on exactly the same course, side effects of higher US rates such as the struggle in emerging markets can in turn usher in an inevitable moderation for market performance and policy.

DXY vs. Fed Funds Dec 2019 Chart (Daily)

The Stakes for the Dollar and US Capital Markets

Consider, that the Fed has been uncontested in its monetary policy pace-setting for years, and the Dollar's gains have moved through both bullish and bearish phases. In the presumed bullish course moving forward, there are certain dangerous caveats for the benchmark currency. The implications of overheating emerging markets and other areas dependent on extreme monetary policy can prove both the cap on policy and the demise on the Dollar. Further refining the scenario, if all the elements are supporting the Fed's course; there is a further complication in that the environment would be generally supportive of an inevitable turn to rate hikes and policy normalization for other major central banks. Though the Fed has established itself a lead, the Dollar's true appeal is in the exceptional contrast it casts relative to counterparts, not in the yield advantage it offers. An approximate 2 percent carry represents very little return in historical returns and would offset relatively little risk in the market when put to task. More likely, as the risks to a hawkish policy grow more numerous, the range of scenarios that see the Dollar lower sets a significantly greater probability. The probability schema for a downgraded rate forecast remain the same when we factor for risk assets, but the route for impact changes somewhat. Using the S&P 500 as our baseline, in previous years, a delay in Fed tightening was hailed as a leverage for risk appetite. Cheaper funds translated into greater access to funds and reinforced speculative reach as standard assets offered little competition for capital. As much as risk appetite seems as robust now as it has anytime over the past decade - owing to the persistent drive to record highs - recognition of instability in exposure is growing. The reasoning as to why the Fed would have to back out of its pre-destined path would raise greater concern than the appeal of slightly cheaper lending for slightly longer. In other words, we could witness the return to positive correlation between rates and the S&P 500 - though predicated on significant risk aversion. We discuss the scenarios for US monetary policy and its impact on the markets in today's Quick Take Video.

Central Banks’ Probability of a 25bp Rate Hike By End of 2018

Written by John Kicklighter, Chief Currency Strategist for DailyFX.com