Talking Points:

- The Swiss Franc has been remarkably strong these past few months despite a notable lack in traditional fundamental background

- An SNB rate decision will be immediately discounted before it even produces its verdict, but surprises are always possible

- Scenarios pose greater potential for a Franc tumble if it should come to pass, to which I like EURCHF better than most crosses

The Curious Case of the Swiss Franc

Of the FX 'majors', the Swiss Franc has proven to be one of the most fundamentally troubled players of the past few years. Back on January 15, 2015, the Swiss National Bank (SNB) announced that it was abruptly abandoning its version of the extreme monetary policy that had had peaked with stimulus (quantitative easing) programs for most of its peers. Rather than open the taps with injections of funds into its own financial system, the local policy authority saw Switzerland's issues more distinctly associated to trade and the in particular the rising cost of its exports on the back of a rising Franc. To answer this issue, the SNB attempted to put a floor under the primary EURCHF exchange rate. That lasted for three years and four months until its disastrous end. After the cost of maintaining the failing effort became too great, it decided to pull the plug just two days after one of its senior members reiterated their absolute commitment to the endeavor. The point of failure for the SNB was the ECB. Its larger counterpart trying desperately trying to prevent the Euro from rising and to bolster inflation committed to a 'traditional' large scale asset purchase program. There was no way to offset a program calibrated to an economy multiple times larger than Switzerland. Three-plus years after the fallout, the markets have moved to completely drown out the SNB's vows and interests.

CHF Index Chart (Daily)

A Completely Discounted SNB Rate Decision is a Risk

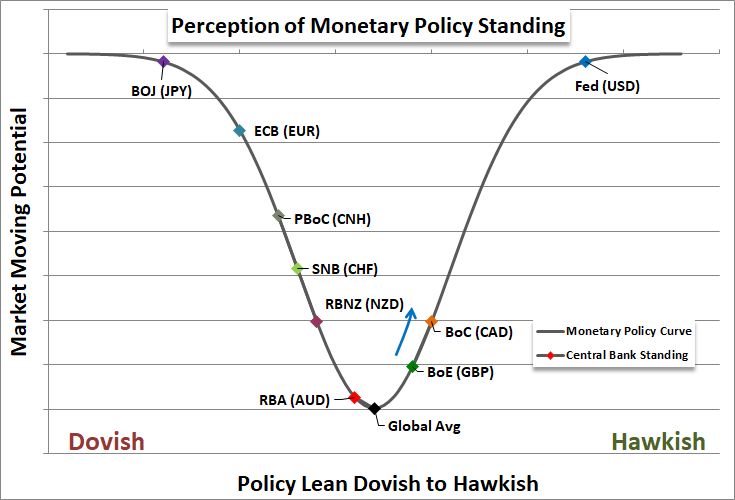

Given the complete loss of credibility for the Swiss policy group, the markets have extended its unmoored assessment to the Franc as well. There are other roles the currency looks to play in the absence of the standard monetary policy filter. A long-standing safe haven, this currency still represents a unique harbor. Rather than simply exhibit an extraordinarily sensitive calibration to every rise and fall in the speculative rhythm, CHF is appealing for its neutral position in global finance and politics. Representing a low-risk participant to the ever-expanding trade wars is certainly beneficial but its role as a beacon for wayward capital has been muted by global tax authorities pressing the country's secretive banking sector. This places the Swiss Franc in an unusual position. After a few months of rally, it now stands with a significant amount of speculative premium. Yet, the motivation for this advance is flimsy or nonexistent. The situation further sets the market to believe the SNB rate decision will be a non-event. Given there is little chance that the Swiss want to follow the Fed and ECB to normalize given their different objective, that leaves no change or a bid to ramp up the dovish pressure. No change would maintain the deepest negative rate among the majors and draw further contrast to the slow and even resistant hawks. If they attempt to ramp up the rhetoric - or are desperate enough to try an actual escalation - the effort is unlikely to prove fruitful. However, it could eventual catch traction and/or speculators may just be looking for a reason to trade back from recent appreciation. To write off the event and the general scenario all-together begs to be caught by surprise.

Monetary Policy Standing vs. Market Moving Potential Chart

Scenarios and Pairs I prefer to Track

While it would translate into greater follow through should the market decide to establish a straight-line evaluation of the Franc and its counterparts by current monetary policy settings or their forecasts, we should plan for the most systemic change. That said, it shouldn't be closed off as an opportunity. Should this interpretation break through, we could take our pick of the CHF litter. More likely, the market's own settings following an extreme speculative positioning move in futures will set the motivation for a retreat if one eventually shows. Among the Swiss crosses, I consider EURCHF the best option is EURCHF. Not only is this the exchange rate the SNB is most focused on, it is one of the least impeded by cross fundamental themes. While the Euro must still deal with the ECB's long-term policy bearings and local systemic issues such as Italy's head-butting with the EU, it is currently one of the least pressured of the majors. CHFJPY would be another dual purpose option should the Franc drop given the Yen's propensity to act like a safe haven currency. I have personal interest in GBPCHF and CADCHF given existing long exposure, but these currencies are competing for its focus with the Brexit and NAFTA negotiations. Two pairs that seem obvious appeal for the Swiss currency are AUDCHF and NZDCHF. They can certainly cater to traditional carry trade fundamentals, but both the Aussie and Kiwi Dollars have lost their status for high yield. We focus on the Swiss Franc and its trade potential in today's Quick Take video.

EURCHF vs. COT Chart

EURCHF Daily Chart

Written by John Kicklighter, Chief Currency Strategist for DailyFX.com