Talking Points:

- US March employment data is due Friday morning with forecasts of 185K payrolls, a 4.0% jobless rate and 2.7% wage growth

- Key to determining the trading pull of this data is establishing how this fundamental run can influence the markets

- Forging a Dollar breakout will be difficult despite technical proximity while volatility can leverage a short-term risk impact

Top event risk through Friday is the US NFPs due at 12:30 GMT. If you are trading the Dollar or markets with a sensitivity to risk trends, keep an eye on the impact this data can have. Join Strategists Chris Vecchio and Michael Boutros as they cover the release and market impact live. Sign up on the DailyFX Webinar Calendar page.

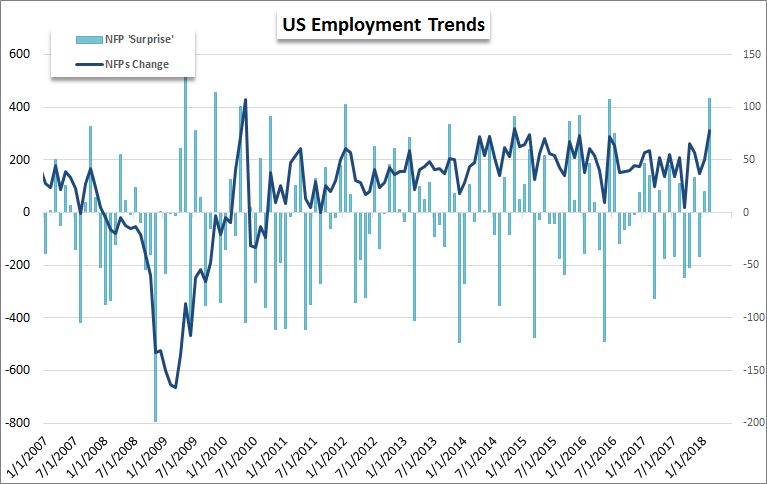

The Name Brand Behind Nonfarm Payrolls

If you ask traders of varying experience levels - from novice to professional - to name the top three market-moving pieces of event risk in the global markets, it is almost inevitable that the monthly NFPs makes the list. Why? It has a history of generating volatility; and anything that can set markets in motion is looked upon with awe or appetite by market participants. However, there is a substantial gap between the headline worthiness of the economic report and its genuine sway over economy and financial system. The labor sector in the US is near its so called 'full capacity' which naturally translates into marginal subsequent impact from further improvement and disproportionate influence through a weaker update. Most experienced traders recognize the limitations of this indicator given historical reactions, the critical fundamental themes of late and the quick disruption with the liquidity drain into the weekend. Nevertheless, the headlines often prove bombastic enough to bolster the market's interests.

Monetary Policy Doesn't Carry Much Weight Anymore

The first rule of fundamental analysis is determining what can actually move the market and what can't. In years past, the Dollar was driven steadily higher on the build up to the Fed's turn in monetary policy to the tightening regime that we are now fully acclimated. Yet, since the rate hikes actually began, the lift started to grow uneven. And in the past year when the central bank's pace turned consistently - where no other major central bank would even come close to regular hikes - we have seen the Greenback actually slide. Why are we discussing monetary policy with NFPs? Because employment and inflation are the dual mandates for the world's largest central bank, and the NFPs is baseline for the former. Yet, even with a projected pace bordering on four hikes in a single year, we have seen the Dollar track out exactly the opposite trajectory as implied rates through year end.

NFPs Is Still Headline Worthy and Capable of Inciting Speculative Salivation

If there is little chance that rate hikes will alter the course for the markets, the chances for a significant Dollar move are significantly reduced. That is a critical hurdle from a trading perspective as the DXY Dollar Index is holding below the top end of a three-month range that happens to coincide with a long-term former trendline support. To not only clear meaningful resistance but turn such a significant bear trend - more than a year strong - the markets need a capable channel and strong catalyst. While we may happen upon the latter, the former is highly unlikely. In contrast, the impact anticipated for the S&P 500 and other risk-leaning markets is already set to more reasonable expectations. Sensitive more to headlines than marginal economic changes, the interest is more often in the degree of surprise on the payrolls print relative to forecasts than any of the underlying figures. Yet, here too, major developments like the major US indices securing a systemic reversal or a return to record highs is highly unlikely.

Market Conditions Will Dictate the Full Extent of Any Response

The difference maker in this particular month's round of employment statistics is not in the data itself. Instead, the amplifier is underlying market conditions. The volatility in 2018 has been attributed to a number of developments from political risk to economic uncertainties to trade wars; but regardless of what has changed the tempo, we are still left with a far more active and reactive market. If the data run produces a particularly potent deviation in payrolls, a surprise in the jobless rate change or offers a heavy swing in wage growth; the market's overly sensitive radar will pick up on the development and response in kind. Just as the slow but persistent improvement in labor conditions has dampened the Dollar's response to hawkish forecasts, so too do the growth-to-risk implications of positive data lose their lifting power for equities and other risk assets. A disappointment would carry more weight, but clearing 23,500 on the Dow or 2,585 for the S&P 500 are highly unlikely on this update alone. We focus on the practical trade implications of the NFPs update in today's Quick Take Video.

To receive John’s analysis directly via email, please SIGN UP HERE