Talking Points:

- There is no doubt that the NFPs - and various US BLS labor statistics - garner some of the greatest speculative attention

- The payrolls change has become a self-fulfilling prophecy of speculative charge, but deeper economic implications rarely bubble up

- For the Dollar, rate expectations is the key aspects; but market implied yields through year end are already rising without USD

Are you watching or trading the upcoming US NFPs release? Join the DailyFX Analysts as they cover the release and analyze the market reaction live. Sign up for the event on the DailyFX Webinar Calendar page.

The monthly US nonfarm payrolls (NFPs) report is celebrated by volatility spotters as one of the most media-hyped events of the calendar month and thereby one of the greatest opportunities for market tumult to trade through. That said, even in the best of times - where liquidity is filled out, markets are less skeptical of value, and the deeper themes this report can tap are fluid - the event risk is disadvantaged. It is released on the first Friday of the month typically which means we have to absorb it in the twilight of the week's liquidity. So, either we get a strong jolt of short-term speculation or we get the motivation for a trend that will continue beyond the weekend. Neither scenario is going to be particularly easy to achieve in our current conditions. First and foremost, we may be wading into the new trading year; but market depth is still restrained by the previous months holiday trade - the deepening sense of complacency over the past year certainly making that difficult.

Speculators, nonetheless, are drawn to opportunities of sharp price movement in this general drought of significant price swings. That said, the greatest potential in this labor report is in the short-term impact it can achieve through risk trends. There are a range of assets that represent the rise and fall of sentiment, but a benchmark like the Yen-based carry trades or junk bonds will be less enthusiastic to response because the implications are more ancillary or they simply aren't near critical technical levels. That is not true for US equity indices though. The major indices from the S&P 500 to the Dow to the Nasdaq all hit record highs this past session. That sets up exaggerated views on already richly priced benchmarks. It could certainly cater to further extend the 'risk on' charge for a short burst. However, the more influential outcome from this data would be a substantial disappointment that triggers concern about the economic engine that should be powering this capital market climb. I say 'should' because the market participants that are currently more prevalent are short-term speculators who care less about the traditional measures of 'value' and more about what they think others would emphasize.

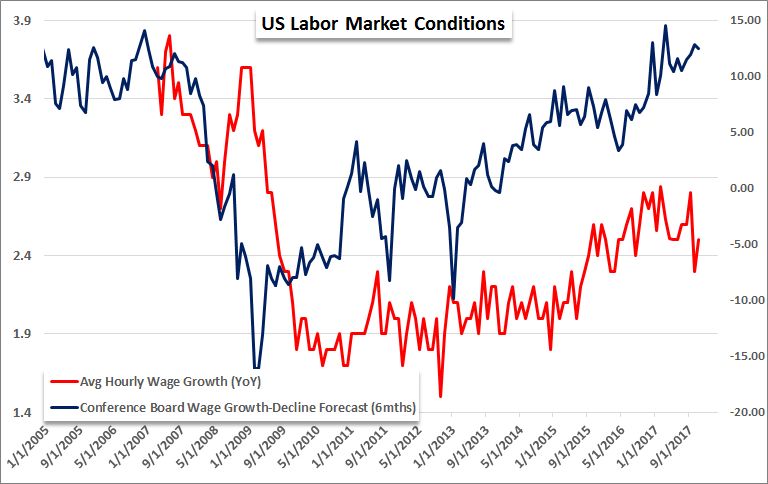

For the Dollar, there are various implications of influence through this data. Yet, the theme that FX speculators will default to is the interpretation of interest rate expectations. In the most academic sense, an improvement in employment trends (NFP beat, drop in jobless rate, rise in wages) translates into faster increases in interest rates and vice versa. Yet, the outlook for monetary policy is increasingly diverging from this economic node and the market instead seems to have a distaste for the Dollar whether the Fed offers a growing yield advantage or not. In fact, the implied yield forecast from Fed Fund futures through the year end has recently surpassed 1.9 percent to close the discount to the Fed's own forecasts. And yet, the Greenback continues to struggle. It is not as clear about what surprise - bullish or bearish - will have the greater impact on the Dollar in terms of sheer volatility like it would for equities and risk assets. We discuss trading the upcoming NFPs to set expectations for reasonable trading in today's Strategy Video.

To receive John’s analysis directly via email, please SIGN UP HERE