Talking Points:

- The S&P 500's climb this past week, since the election and back a full 12 months has proven nothing short of exceptional

- Consistent gains however come with a clearly throttled pace, while the threat of irregular but violent corrections looms

- Aside from the fundamentals and market conditions skewing the picture, risk-reward statistics support caution

See what live coverage is scheduled to cover key event risk for the FX and capital markets on the DailyFX Webinar Calendar.

After its last major correction through the opening weeks of 2016, the S&P 500 has climbed nearly 30 percent from its low. This despite its dalliance with record highs, concerns about underlying growth and a conspicuous imbalance of risk to prospective return. Doubt is warranted, but should that keep us out of the market? Mere skepticism? Sometimes, we just read the market wrong; and speculative motivation proves to arise from a different source. Is that the case currently for US equities or risk trends more generally? The first consideration in evaluating the wisdom of remaining sidelined is an accurate gauge on the risk-reward balance in the market.

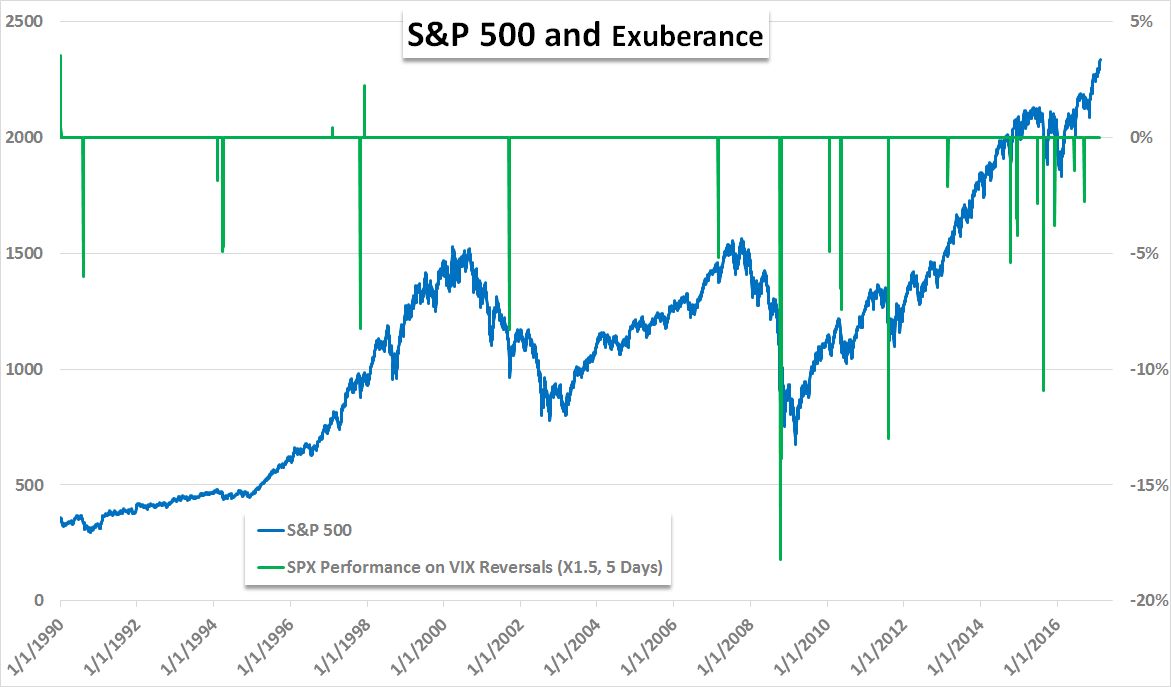

Both the potential for return and loss can be assessed in broad abstract terms. Looking at a baseline for the market's yield, record low benchmark rates from central banks translates into unprecedented market returns. The need for capital gains to compensate for an extreme lack of 'income' is evident. On the other end of the trade, complacency is deeply ingrained in low volatility readings and a surprising lack of hedge interest. The term 'sitting duck' comes to mind. Yet, statistical measures point to an imbalance of risk-reward as well. The 86 consecutive trading days without a 1 percent decline from the benchmark US equity index may be the longest stretch in a decade, but it is a passive threat that can grow more extreme with time.

When activity is exceptionally low, volume naturally contracts and set the stage for conditions ripe for liquidity-driven moves to de-risk. That means that day-to-day performance as the market rises will statistically be measured (small) even if they are more probable. In contrast, the threat of large corrections arising from data and speculative-centered events are more spaced out but potentially destructive. In periods where the VIX has doubled in two weeks' (10 trading days') time, the S&P 500 dropped has dropped between 8 and 16 percent in the three instances over the past six-and-a-half years. A 50 percent increase for the measure in just 1 week (5 trading days) is far more common, and the underlying market response still severe. The question is whether the risk of sharp and deep losses is worth the risk for small, nerve-racking gains? We discuss this in today's Strategy Video.

To receive John’s analysis directly via email, please SIGN UP HERE