S&P 500, Yield Spread, Monetary Policy, Recession and USDJPY Talking Points:

- The Trade Perspective: S&P 500 Bearish Below 4,075; USDJPY Bearish Below 134.00

- S&P 500 suffered its worst week’s loss in over two years with similar levels of volume, meanwhile the Dow is nearing its own ‘bear market’

- While the focus was monetary policy this past week, recession risks and financial stability are the top matters through the week ahead

Risk Appetite Takes a Serious Hit

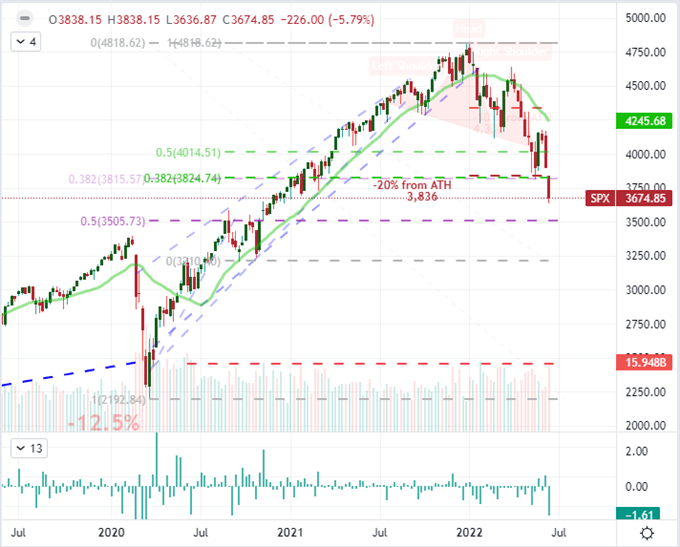

There wasn’t much of a silver lining to register in the markets through this past week. An aggressive shift in relative global monetary policy eroded speculative appetites and materially boosted the fear of a forthcoming recession. Where systemic fundamentals were essentially an afterthought for many years, these dominant themes are now overriding the speculative ebb and flows across the financial system. We may have very well passed the threshold whereby unfavorable headline can be sidelined for speculative advantage. Given the tightening of financial conditions, rise of recession fears and general swoon in favorite ‘risk markets’ of late; there is a strong fundamental drive to the market’s slide. While I prefer to assess sentiment through a broad range of benchmarks, the US indices offer a particularly acute view. The S&P 500 officially notched a ‘bear market’ from the very start of the past week; but the collective worst week’s performance in 2-years, the lowest levels in over 18 months and the heaviest volume since June 2020 really throws speculative weight to the mix. All of that said, if I were looking for a singular milestone to exert an impression on the markets, it would whether or now the ‘value index’ Dow falls into a technical recession itself (29,562) in the week ahead.

Chart of S&P 500 with 20-Day SMA with Volume and Daily Gaps (Daily)

Chart Created on Tradingview Platform

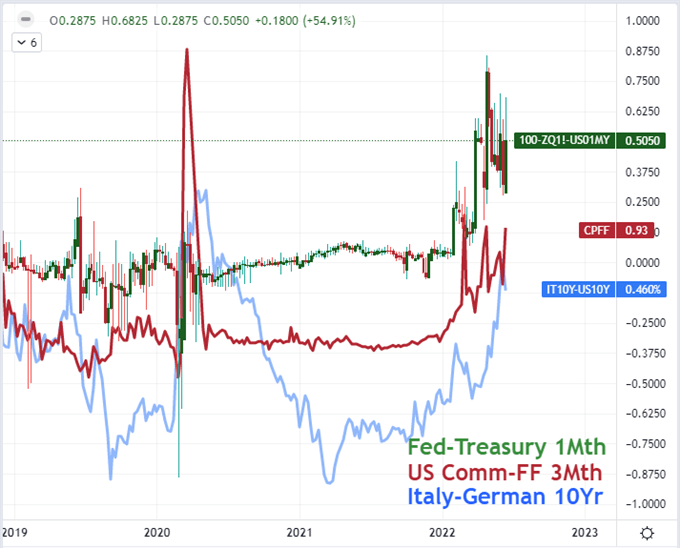

In the past week, I have described the scenarios in which the market is likely to find its balance and start to contemplate an earnest recovery. A fundamental reversal would necessitate a significant easing of inflation pressures and a serious reversal of economic forecasts. Such a shift would take considerable time. Speculative influence carries with it the potential for a faster tempo change; but that bearing is just as likely – perhaps more so – charge a deeper market slump. While the VIX’s proximity to 50 is a loose baseline for judging whether the market will exhaust itself to the downside, my concern is broadening to encompass measures that are more indicative of financial stability. The list of fractures in the system have grown lately. The US 2-year to 10-year yield spread has signaled a ‘recession risk’ inversion, but the yield curve is its own issue. In Europe, the surge in yield spreads (eg Italy to Germany) echoes conditions from the European debt crisis. Back in the US, commercial yield spreads relative to the Fed Funds and US Treasuries’ differential from the same baseline have surged to levels comparable to the Great Financial Crisis in 2008. A break in the financial system could materially worsen our course.

Chart of US Gov’t Yield Spread, Commercial Yield Spread, European Yield spread (Weekly)

Chart Created on Tradingview Platform

Monetary Policy Has Destabilized Complacency

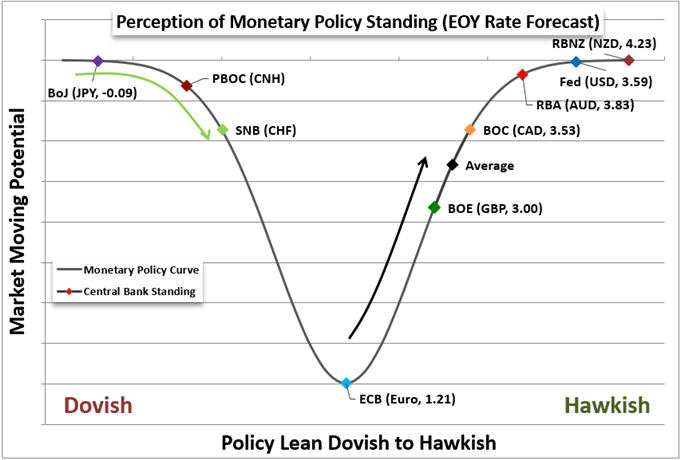

There is little disputing the suggestion that this past week’s market slide was rooted in the tightening of monetary policy. Not only did the Federal Reserve hike 75 basis points, but a number of its peers made significant moves of their own. The Bank of England hiked 25 basis points but hinted at a faster pace ahead. Most notable was the Swiss National Bank (SNB) which unexpectedly hiked its rate 50 basis points (to -0.25 percent), which puts more of the global policy spectrum into motion. There is only one major central bank rate decision on the docket next week – the Bank of Mexico is seen hiking 75 basis points – but there is plenty of feeder event risk to sway speculation around important policy moves in the future. Most notable in the scheduled is the Fed Chairman Powell testimony before Congress over two days. The central bank’s preemptive prepared statement to the government made clear that constraining inflation is an unconditional goal.

Table of Major Central Bank Relative Policy Stance with Expected EOY Rate Forecasts

Chart Created by John Kicklighter

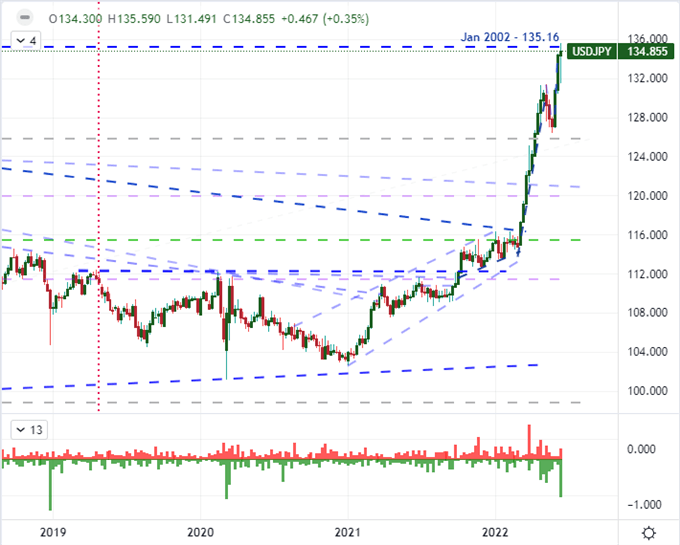

Speaking of monetary policy, the contrast is rate bearings between Japan and the rest of the world seemed to have hit a new extreme. Where the Fed just announced a 75 bp increase and others are contemplating large hikes, the Bank of Japan (BOJ) decided to reiterate it commitment to strong growth by targeting its 10-year government bond yield. Initially, the JGB 10-year did retreat, but the market reversed quickly back higher. For USDJPY, the initial reversal I’ve been monitoring has stalled; but that doesn’t mean the general turn is risk that shouldn’t be monitored. There is good reason to treat the Yen as a funding currency (short) to pursue carry elsewhere. That said, the forward projecting yield forecasts are likely to level out in the near future. After the unexpected 50 bp rate hike by the SNB this past week, there is increasingly stringent expectations on how monetary policy impacts the consumer board. I still believe the criteria for market movement on USDJPY is big picture bearing; but it is important to understand the technical expertise in DailyFX

Chart of USDJPY with 20-Day SMA and Consecutive Candle (Daily)

Chart Created on Tradingview Platform

What’s Driving Markets: From Mon Pol to Recessions

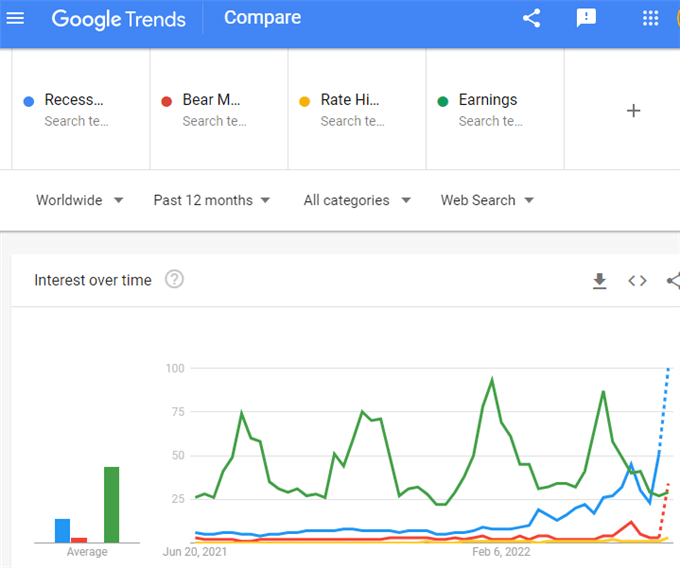

As monetary policy takes a breather for its influence on the financial community, there is some interesting data to incorporate into the collective conscious. When it comes to market health, I believe that the impact of changing interest rates will hit first where the gaps are sizable. The list of qualified candidates here is dwindling fast. It isn’t that there is a ‘carry currency’ option out there. In fact, there are an abundance of higher yielding currency which has prevented the likes of GPBUSD or AUDNZD from truly taking off. In contrast to the Fed hikes, I am watching the facilitators of such volatility in inflation and growth troubles. Recession signals come in many forms, but the US 2-10 year yield has already inversed while certain officials have suggested just such a correction could come ahead. My preference is in policy outlook moves form price action according the Conference Board’s (CEO) but recessional and bear market search interest has skyrocketed. If the June PMIs or risk appetite in general lead to the downswing, beware the momentum.

Google Search Interest in the US for ‘Recession’, ‘Bear Market’, ‘Rate Hikes’ and ‘Earnings’

Chart from trends.google.com/trends

So, we know to watch for rate expectations and capital-market linked sentiment, but the day to day movement of the markets won’t obfuscate opportunity. From the economic docket, there is more potential in surprising to the upside rather than the alternative. Among the big ticket items that we would need to keep tabs on this week, the Jerome Powell semi-annual update before Congress will carry significant heft for the rate watchers. Alternatively, the Conference Board’s CEO assessment of recession concerns worked up certainly believers. I don’t find myself in that category.

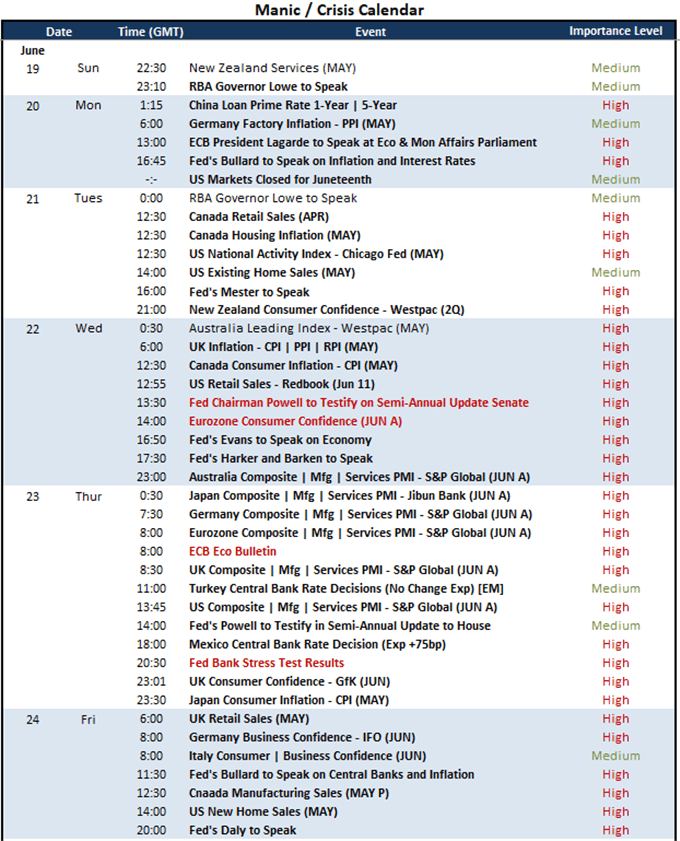

Calendar of Major Global Economic Events

Calendar Created by John Kicklighter