QQQ Nasdaq 100 ETF, S&P 500, Dollar, AUDUSD and AUDCAD Talking Points

- The Trade Perspective: QQQ bearish on reversal from 380; EURUSD bearish below 1.1200; AUDCAD bullish above 0.9050

- Amid a run of after-hours earnings, Google’s 4Q report smashed expectations and sent GOOG shares rallying in off hours – will the Nasdaq 100 be fueled by the move?

- Wednesday is a lull in an otherwise heavy week for event risk, but the Eurozone CPI and US ADP payrolls will offer a prelude to ECB and NFPs…and perhaps EURUSD volatility

As Good as a Top Level Bullish Catalyst as We Can Expect

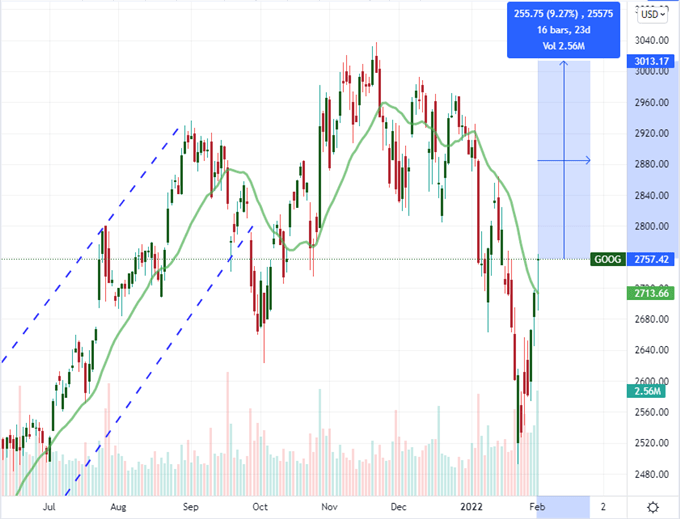

We may have seen a short stretch of strong gains for the US indices, but there is as yet limited momentum from the likes of the S&P 500 and Nasdaq 100. What’s more, there remains limited breadth to the bullish move across the financial system. Global equities, junk bonds, carry trade and even the already-charged crude oil market are showing a unmistakable lack of enthusiasm for this current swell. Perhaps persistent will win the broader markets over or a definitive and unabashed fundamental driver. I’ll be gauging both through Wednesday’s US session open following the remarkable showing by Google earnings after hours this past session. There were a host of high profile companies reporting after the close (from the strong performances like AMD to the painful such as Paypal), but the tech behemoth clearly stood out. The FAANG member soundly beat forecasts with a $30.69 EPS (earnings per share) that beat against $27.35 expected on a staggering $75.3 billion in revenue. Given the more than 9 percent rally after hours for GOOG shares, there is a strong argument to be made for spillover enthusiasm from the specific ticker to the general tech sector to the market at large. But if that appetite doesn’t show up, it will be something of a glaring absence for bulls.

Chart of Google with 20-Day Moving Average, Volume and After-Hours Change (Daily)

Chart Created on Tradingview Platform

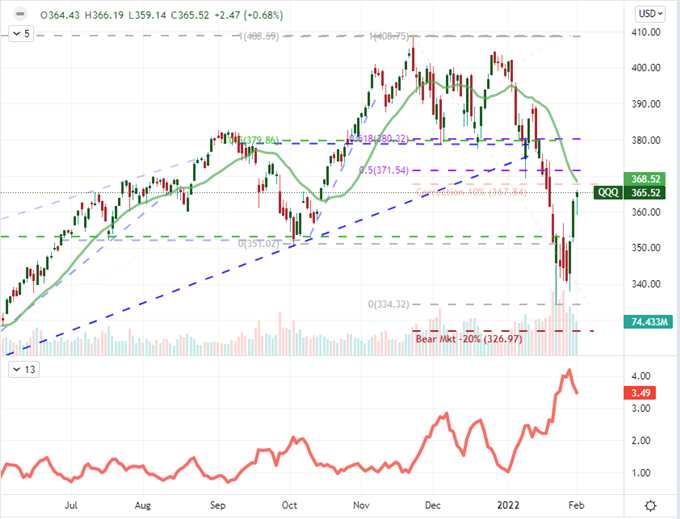

Looking at the QQQ’s (Nasdaq 100 ETF) response to the Google news, the broader tech measure was also higher, though with far less momentum to its name as would be expected from a singular component’s influence – even one as large as Google. We are running into a nest of resistance from the official ‘correction’ line (367.84) to the midpoint of the November to present range (371.54) to the long-term channel we crashed through last month (380). I am most interested in seeing if/when momentum flags and seeing a restoration of the nascent bear trend. That is not to say it has to happen, but between a bullish or bearish market projection, the latter is likely to come with greater intensity. A clear strike against follow through on this measure in particular – besides the sentiment not spreading to the rest of the speculative market – is that anticipation for Facebook (now Meta) after hours Wednesday and Amazon who reports after the close Thursday.

Chart of QQQ Nasdaq 100 ETF with 20-Day SMA, Volume and 10-Day ATR (Daily)

Chart Created on Tradingview Platform

Wednesday is a Data Lull

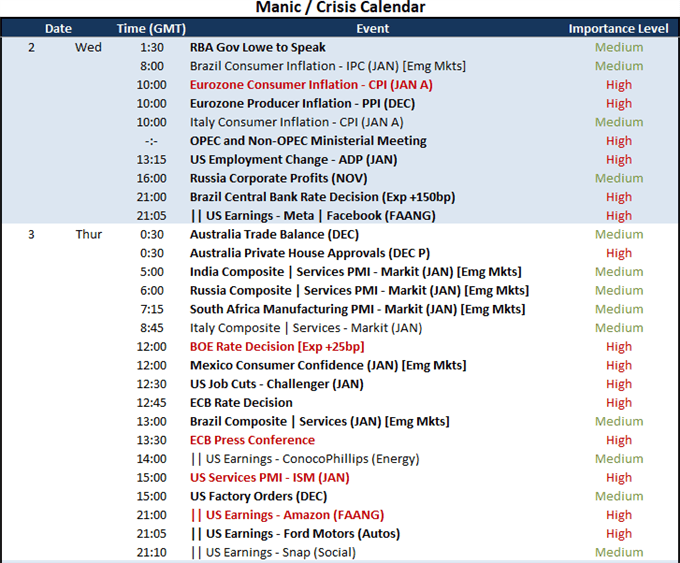

Through this week, the event risk that can exact serious influence over large segments of the capital market is numerous – and there are quite a few updates that could tilt the entire financial system with the correct outcome and background conditions. Friday NFPs, Thursday’s ECB and BOE rate decisions and the previously mentioned earnings are a few such loaded events. However, there is a notable lack of these big ticket items for the current session. Eurozone inflation, US private payrolls, the Brazil central bank rate decision and Facebook earnings are top billings with a notable lack of the full reach I am looking for scalable speculative impact.

Calendar of Top Macro Economic Event Risk for the Week Ahead

Calendar Created by John Kicklighter

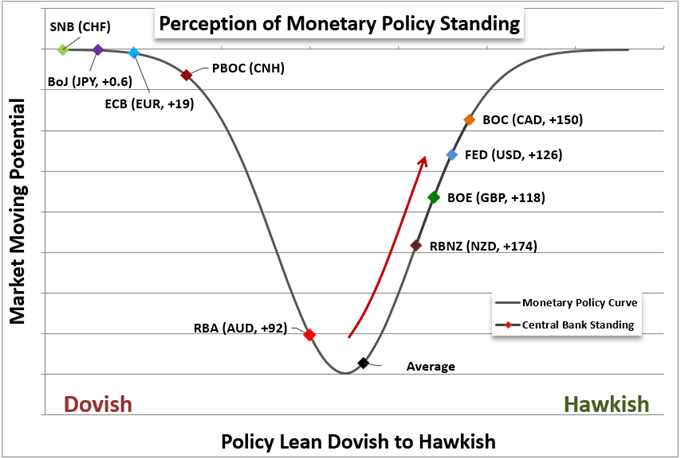

Thematically, interest rate speculation is still the greatest fundamental scope in the global market. This past session, the Reserve Bank of Australia (RBA) announced an end to its stimulus program, but it also attempted to talk the market down on its rate expectations. The swaps market was pricing in approximately 92 basis points of tightening this year. The market doesn’t seem to believe their intentions – or options. Swaps this morning place the outlook for tightening through year end now at 98 basis points. The Aussie Dollar reflected that hawkish disbelief, and AUDCAD is flirting with a bullish break around 0.9050 to start Wednesday’s trading session. Ahead, in the Americas’ session, Brazil’s central bank is due to announce its own policy and there is anticipation of a remarkable 150 basis point hike. That is a big move – even for an emerging market policy through – but it also sets expectations very high. Keeps tabs on USDBRL.

Relative Monetary Policy Standing of Major Central Banks

Chart Created by John Kicklighter with Data from Swaps

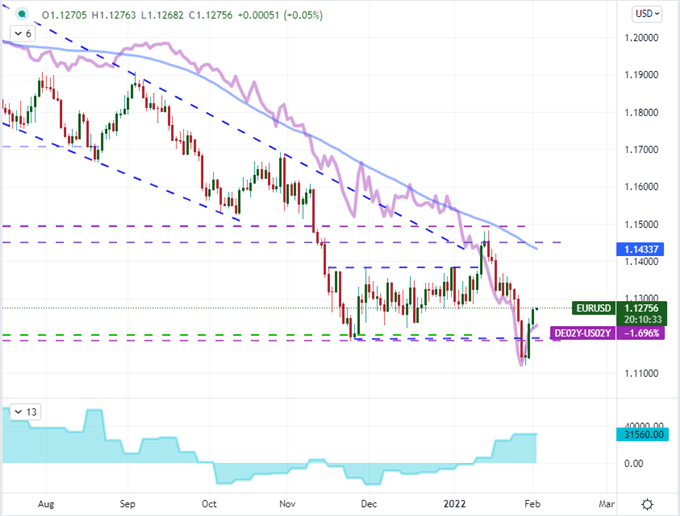

One of the most important, but perhaps innocuous, monetary policy updates we are due through Wednesday will be the trade off between the Fed and ECB. Tuesday’s ISM manufacturing activity report disappointed on the headline figure, but it reported a jump in both the employment and inflation metrics. That only reinforces the pressure on the Fed to keep considering five or more hikes and threaten a 50 bp option to scare the market into compliance. The ADP payroll figure is a more reflection of the official NFPs due Friday, but the markets are in a position to be sensitive to headlines. Meanwhile, the Eurozone consumer price index (CPI) for January will come just before Thursday’s ECB rate decision. If inflation pressures are unrelenting, efforts to steer speculation away from a 2022 rate hike will prove very difficult. I still see the Fed as leading in this comparison, but I’ll wait to see if we can get back below 1.1200 and further below 1.1100 before making a call on where sentiment is landing.

Chart of EURUSD with 100-Day SMA Overlaid with German-US 2-Year Spread and COT (Daily)

Chart Created on Tradingview Platform