QQQ Nasdaq 100 ETF, Amazon, Apple, EURUSD and Dollar Talking Points

- The Nasdaq 100 finally managed to make its way to a record high after a 35 day hiatus, but the Apple and Amazon earnings misses afterhours raise Friday follow through worries

- EURUSD rallied Thursday after the US 3Q GDP proved weaker than expected and the ECB failed to hit the same dovish tenor of previous meetings

- Friday will keep volatility circling the benchmark FX pair with Eurozone GDP and the Fed’s favorite US inflation report due for release

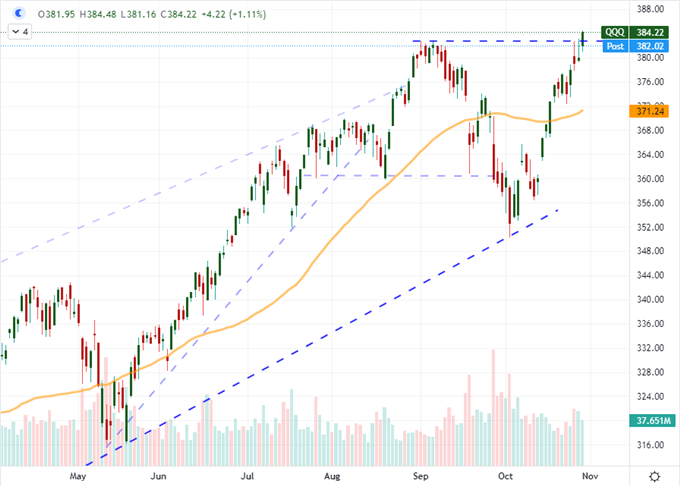

Nasdaq 100 Finally Scales its Record High, But Good Luck Holding It on Friday

Risk appetite was an uneven picture this past trading session. While the US indices fell back on their bullish charge, there was a notable lack of conviction – and even some retreat – from the global equities, carry trade, emerging market assets, junk bonds and risk-oriented commodities. Nonetheless, the Nasdaq 100 tagged its record high. The tech-heavy index has noticeably lagged its S&P 500 and Dow peers in hitting that milestone, which is an uncomfortable situation for the tech sector-heavy measure given its outperformance over the past few years in particular. Notably, the QQQ’s (Nasdaq ETF) record was notched despite a disappointing US 3Q GDP update and further charge in Fed rate forecasts – not to mention the lack of confirmation from global counterparts. We were already in a questionable position to establish follow through, but that run is under even greater pressure considering afterhours earnings from Amazon and Apple very clearly fell short of expectations, while anticipation for next week’s FOMC rate decision represents an outsized risk.

Chart of QQQ Nasdaq 100 ETF with 50-Day SMA and Volume (Daily)

Chart Created on Tradingview Platform

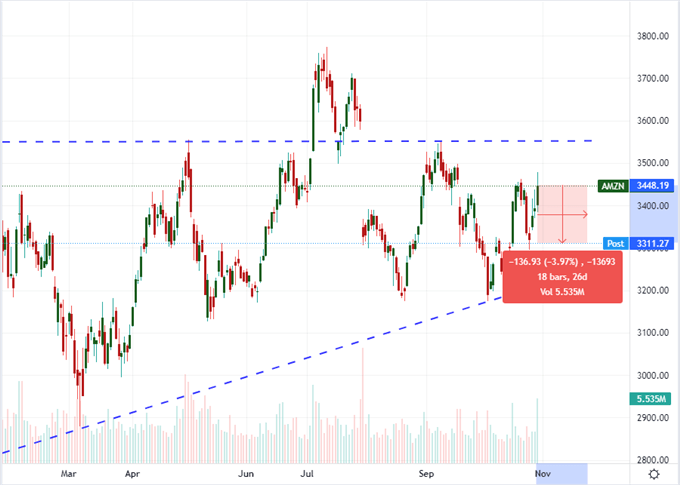

The FAANG collective may have lost some of its luster since the rise and fall of the meme stock craze and the ever-oscillating popularity of cryptocurrency market, but it nevertheless represents an enormous concentration of speculative appetite. That said, it’s influence hasn’t waned much through the various distractions – though perhaps the acronym should be shifted. Facebook, dogged by regulators and legislators, could be dropped; while Tesla should be added to the group. The electric vehicle maker has gained greater and greater traction as climate change has taken center stage and its deal with Hertz has expanded amid a deal with Uber. Nevertheless, Amazon, the consumer giant reported an unusual miss in earnings with EPS of $6.12 (versus $8.97 expected) and revenues registering $110.8 billion (against $111.8 billion) with a lower 4Q sales forecast than was expected. Naturally, AMZN shares were lower afterhours. A recovery for Friday trade (like Intel) would be much more difficult to inspire given this data actually warrants the swoon.

Chart of Amazon with Volume and Afterhours Change (Daily)

Chart Created on Tradingview Platform

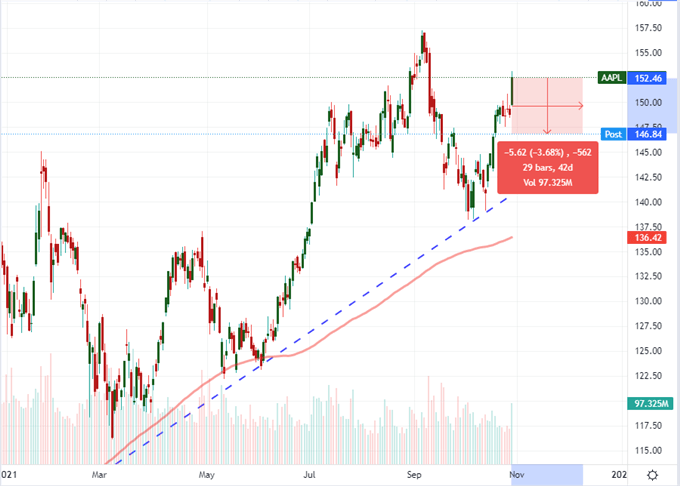

The other top market cap stock to report its earnings Thursday evening was Apple. The consumer tech good company was in a very similar position to Amazon. It met its Earnings Per Share forecast of $1.24, but revenues fell short of forecasts with $83.36 billion versus $84.69 billion projected. After hours, AAPL fell 3.5 percent to significantly reverse the gains earned through Thursday’s active trading session. Though this may seem an equities matter, global macro traders would do well to pay close attention to see how both AMZN and AAPL trade through the opening hours of Friday on the New York Stock Exchange. While these tickers can move in contrast to the broader markets, that is a particularly unusual case when we are seeing the indices push a record high with an enormous amount of headwind to raise concern.

Chart of Apple with 200-Day Moving Average and Volume (Daily)

Chart Created on Tradingview Platform

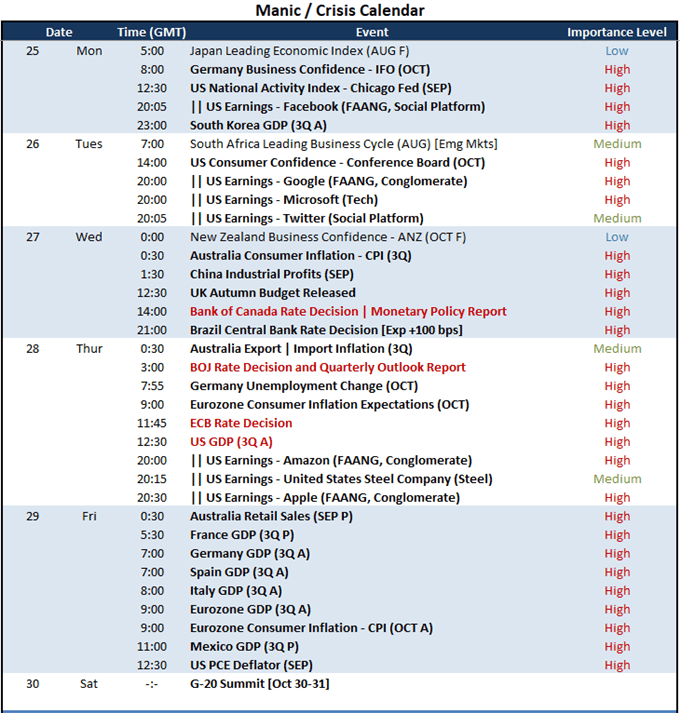

A Final Run of Event Risk for Friday

Through this past session of trade, the top macro-economic event on tap risk proved particularly remarkable for EURUSD. When facing multiple, significant market-moving updates influencing the same asset, it is just as likely that they conflict and leave the market listless as align and provide a decisive charge. Between the ECB rate decision and US 3Q GDP release this past session, there was an unexpected consistency for the benchmark exchange rate. The ultimate rally was helped in part by the monetary policy event for which the market decided to interpret aggressively. Though the group didn’t actually change in policy mix, there was a notable shortcoming it the typical reiterations of a dovish policy view. President Christine Lagarde wouldn’t offer up the same conciliatory language of an indefinite backstop that traders have gotten used hearing. With so many of the ECB’s peers shifting to outright normalization (or even tightening), it would indirectly take on some of the same perception.

Calendar of Major Macro Event Risk for the Week

Chart Created by John Kicklighter

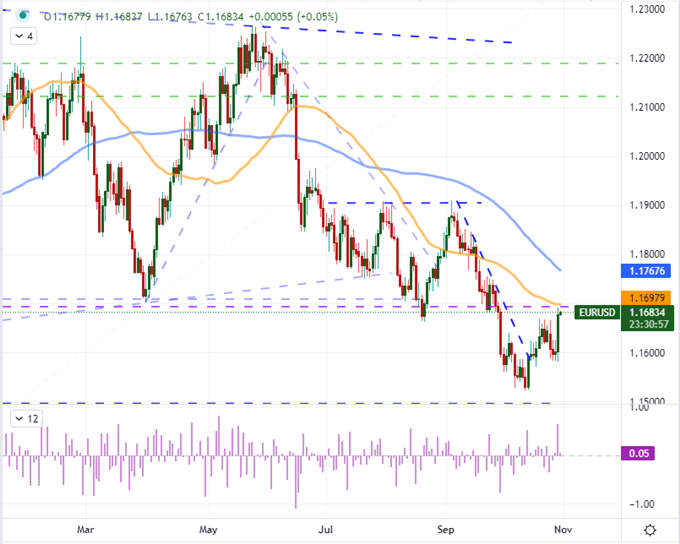

From EURUSD, the biggest daily rally since May 7th reflect as much of the one-sided market as the actual speculative charge that would provide the lift. Between the two major event risks this past session, the US 3Q GDP carried far more decisive weight for the pair than the ECB update. Growth in the world’s largest economy cooled faster than expected, running at a 2.0 percent pace versus the 2.7 percent expected. That should raise any alarms considering we are slowing from a stimulus-led pandemic recovery, but it still generates drag on enthusiasm. A subsequent charge higher from this pair would require a break above a long-term Fib level and 50-day moving average around 1.1700. This would be no small feat, but we do have some meaningful event risk to serve as a platform if the data lines up. Euro-area 3Q GDP data have a favorable contrast to draw against the US docket’s slip while the Fed’s favorite PCE deflator update is due as direct fodder for next week’s FOMC rate decision.

Chart of EURUSD with 20-Day SMA (Daily)

Chart Created on Tradingview Platform

Don’t Forget What is Just Beyond the Horizon…Markets Won’t

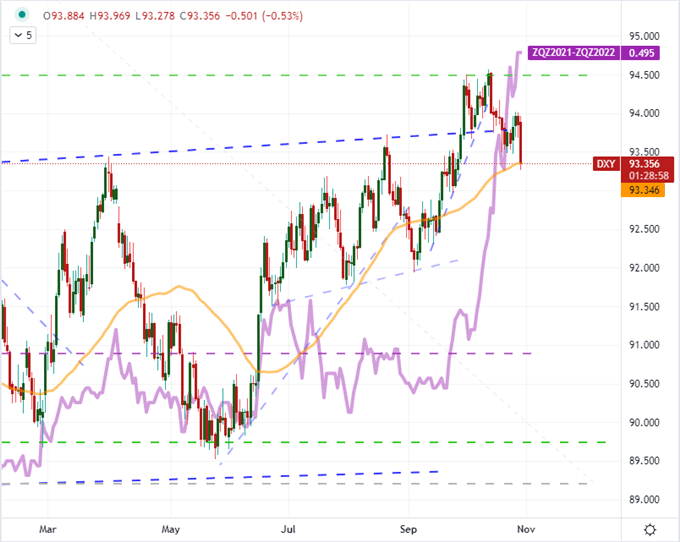

Friday has enough event risk to keep things interesting for the Dollar, Euro and broader risk markets. I will also be keeping tabs on the Mexican Peso given Mexico’s 3Q GDP is also scheduled. That said, anticipation is as much a driver for speculative intention as the aftermath of past releases. For the US inflation data, it is the anticipation for next week’s FOMC rate decision – where the onus of a taper decision weighs heavy – that presents such hefty market potential. As it stands, interest rate expectations over the coming year have surged to fully price in two full, 25 basis point rate hikes through 2022 via Fed Funds futures, while swaps are more aggressive still.

Chart of DXY Dollar Index Overlaid with Implied 2022 Fed Forecast from Fed Fund Futures (Daily)

Chart Created on Tradingview Platform