S&P500, Dollar, NFPs, Debt Ceiling, EURCAD and GBPJPY Talking Points

- News of a debt ceiling deal charged the ‘buy the dip’ crowd to charge the S&P 500 higher, but how much follow through is there for two months of wiggle room?

- Both risk trends and the Dollar will look to Friday NFPs as another rung in a fundamental drive

- In addition to US employment, event risk volatility traders should keep close tabs on the BoE’s economic bulletin and Canadian jobs data

A Strong – But Possibly Temporary – Rebound in Risk Trends

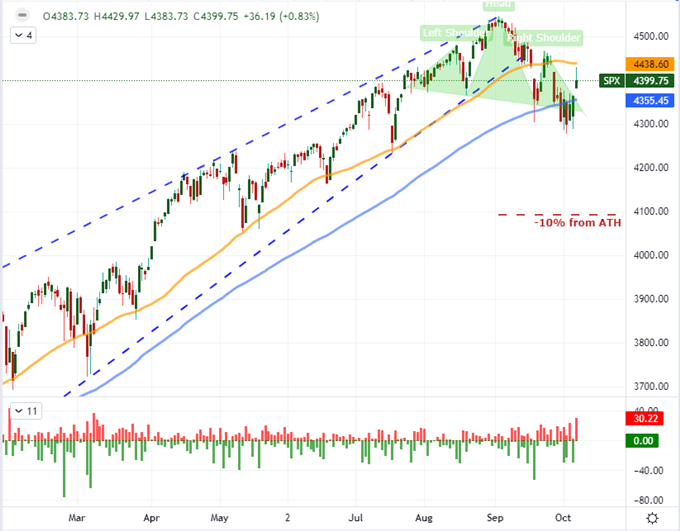

There was an unmistakable charge in risk benchmarks like the S&P 500 this past session, and it wasn’t difficult to trace the source of the enthusiasm back to a particular fundamental catalyst. Reports that the US Senate had scrounged the votes necessary to delay the impending breach of the debt ceiling was certainly occasion for a ‘relief rally’. That said, the solution is quite explicitly a temporary one, and there are other fundamental uncertainties that potential bulls will have to mull over before they can give themselves over to true conviction. Given that this immediate risk is a can kicked down the road and there are NFPs to take over for market participants prone to otherwise relent to aimless optimism, traders should be mindful of simply reverting to the status quo. As a milestone, the SPX is still a very representative measure. The index posted a 0.5 percent rally to open this past session – the Nasdaq’s 0.9 percent gap was the biggest in nearly 5 months – but it would end the day with biggest ‘bearish wick’ (intraday bearish reversal) in 7 months. That does not bode well as a measure of intent.

Chart of S&P 500 with 50 and 100-Day Moving Averages with Gaps (Daily)

Chart Created on Tradingview Platform

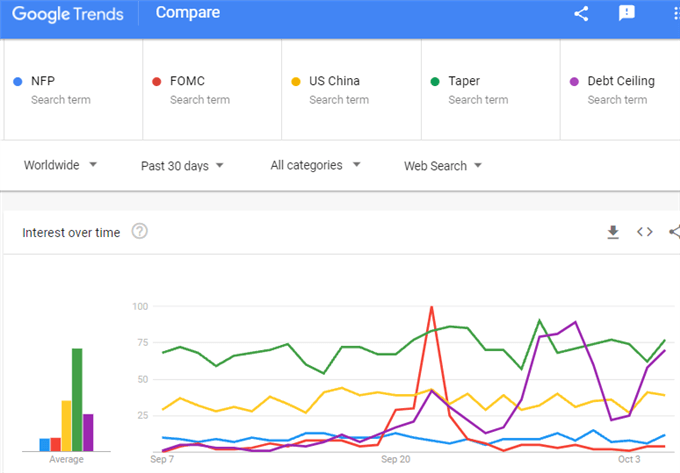

For some, the news that the debt ceiling’s deadline has been pushed back from the Treasury’s expiration date of October 18th to an early December timeline is a signal for indulgence. The attention paid to this existential risk to the financial system earns a serious respite from the anxious, but it pointedly does not resolve the larger problem of a looming default for the largest economy in the world and the ‘risk free’ foundation of global capital markets. I don’t think it was ever a serious consideration that US politicians – as divided as they are – would allow for the self-immolation of a default. However, the scale of the threat in a downgrade related to brinkmanship meant this was a matter that would not simply be overlooked. The question, naturally is: how far does the relief stretch? We are still very clearly on a path towards monetary policy normalization and China’s situation is on holiday pause to be picked back up next week. For me, the real question is not whether risk appetite has reversed, but rather what is next to take up the banner.

Chart of Global Search Interest for NFP, FOMC, US China, Taper and Debt Ceiling (Daily)

Data from Google Trends

The Dollar is Once Again at the Center of Overlapping Fundamental Matters

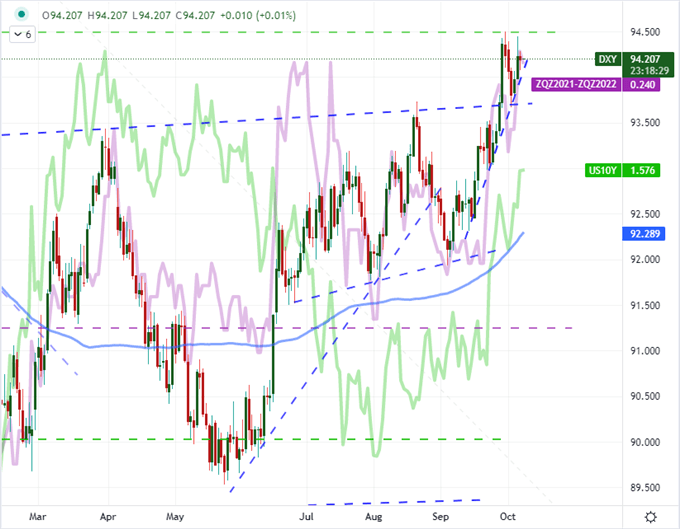

For those evaluating market activity as their gauge for market interpretation, the Greenback’s performance heading into Friday should be quite the sign of priority. Despite the relief around the debt ceiling, the DXY Dollar Index was virtually unchanged this past session. Though it may have been an expected outcome and we are only pushing back the countdown a few months, it would nevertheless seem just as prime a speculative target as the US equity indices. Alas, that appeal has not shown through. The mixed perspective of risk trends certainly does not help the safe haven currency, but it may very well be the natural shifting of attention from deficit to Fed taper potential that has kept the currency from progressing. For those looking to distinguish progress on these fundamental themes rather than taking guidance from the distracted position of the Dollar, the US 10-year Treasury yield is a good sign of fiscal expectation while implied yield forecasts from Fed Funds futures (pricing 2022 rate hikes below) are better measure of monetary policy influence.

Chart of DXY Dollar Index Overlaid with US 10-Year Yield and Fed Forecasts 2022 (Daily)

Chart Created on Tradingview Platform

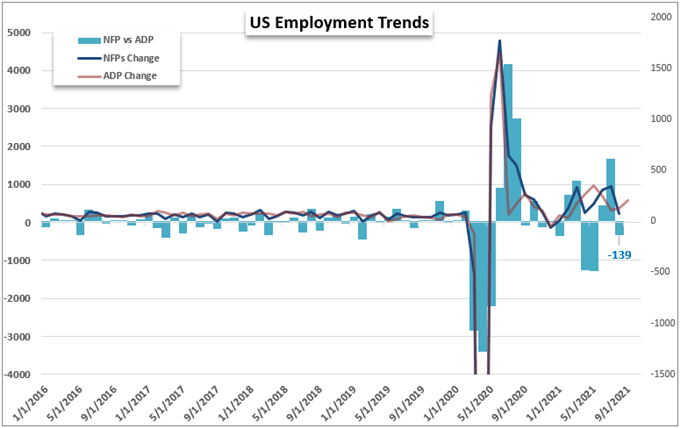

Looking out over Friday’s docket, there is a clear, top-market mover on tap: the US September nonfarm payrolls. The employment report from the US government is one of the most recognizable fundamental drivers for US and global markets. Consensus forecasts of a 500,000 net increase in jobs leans towards the favorable for those looking to growth, but that is perhaps somewhat reserved relative to the other employment data we’ve registered this week. The ADP private payrolls beat expectations (568,000 versus 428,000) and initial jobless claims were significantly smaller than expected (2.714 million against 2.780 million) projected. That could position the data to carry weight in either a ‘beat’ or a ‘miss’. For more than just the ‘name brand recognition’ volatility, the implications for the November 2nd FOMC taper call will determine how far the reaction carries.

Chart of US NFPs and ADP Private Payrolls (Monthly)

Chart Created by John Kicklighter with Data from BLS and ADP

Other Than the NFPs….

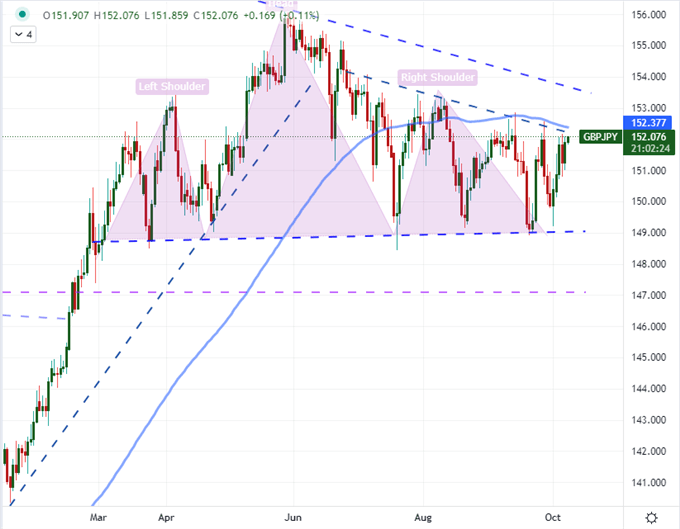

While the US employment report is the top, market-moving event risk on tap through this final trading session of the week; it isn’t the only data point for which traders will be monitoring. In the European session, the Bank of England’s (BOE) quarterly bulletin could generate some heat around interest forecasts for the British Pound. As it stands, interest rate forecasts are remarkably hawkish for the central bank relative to global counterparts with swaps pricing a probability of rate hike by February for the group – well ahead of most counterparts. It will be difficult – though not impossible – to further build upon those bullish expectations and lift the Sterling. That said, it is easier to throttle hawkish expectations and see the Sterling retreat. That said, I like GBPJPY for the scenario analysis as its range caters to the Sterling imbalance and the pull on ambitious risk trends.

Chart GBPJPY with 100-Day Moving Average (Daily)

Chart Created on Tradingview Platform

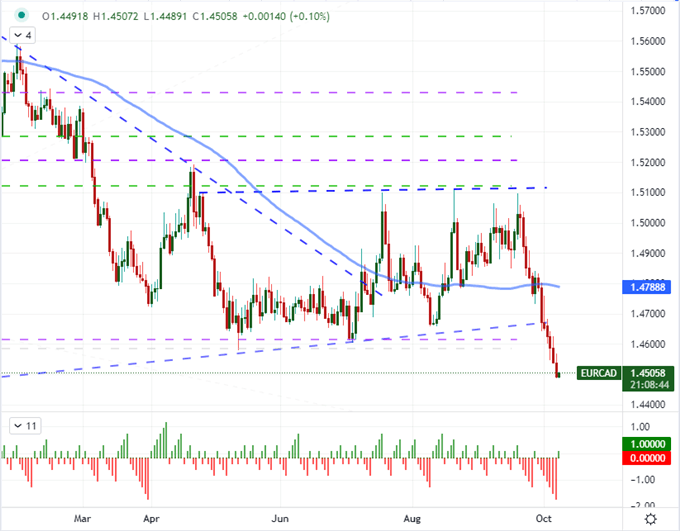

Perhaps an even more obscure event risk through Friday is the Canadian employment report. With a release time that competes with the US NFPs, the northern jobs report will see its media attention significantly drained. That said, there is plenty of capacity for the Canadian data to generate volatility for its own regional assets and currency crosses outside of the USDCAD pull. I will avoid that benchmark cross for its fundamental confusion, but pairs like EURCAD will not have competing themes, but this particular pair has made an ambitious move with a high profile technical breakdown and a 7-day consecutive slide that could be just as primed for reversal as follow through.

Chart of EURCAD with 100-Day SMA and Consecutive Day Count (Daily)

Chart Created on Tradingview Platform