Market Minutes Overview:

- Recent US economic data has been hotter than hot, with the Atlanta Fed GDPNow 2Q’21 growth forecast clocking in at +10.3%.

- Friday’s US nonfarm payrolls report comes with great expectations following the May US ADP employment change report.

- The Fed’s taper timeline hasn’t accelerated one way or the other.

Heating Up

When a fire burns, the difference between a red flame and a white flame is roughly 1,000°F. The same can be said about an advanced economy: if growing at +5% annualized is considered red-hot, then growing at +10% annualized must be considered white-hot. And given where the US economy stands on this Thursday, June 3, it appears that we’re on the verge of a white hot American summer.

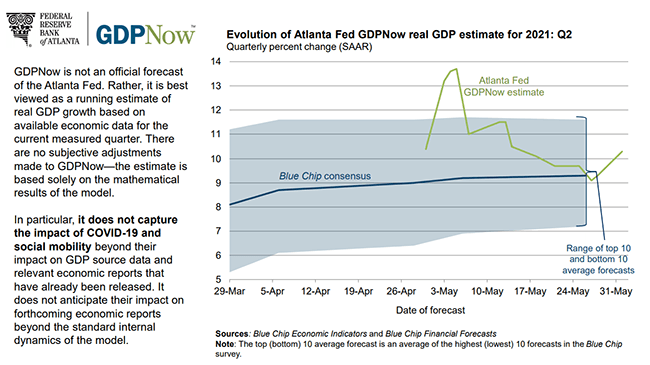

The Atlanta Fed GDPNow 2Q’21 growth forecast is coming in at a searing +10.3% annualized, a rate of change which, if achieved, would bring about the fastest consecutive two quarters of compounded annual growth in US history since 1984.

Atlanta Fed GDPNow 2Q’21 Growth Estimate (June 3, 2021) (Chart 1)

Based on the data received thus far this week, per the Atlanta Fed, “the nowcasts of second-quarter real personal consumption expenditures growth and second-quarter real gross private domestic investment growth increased from 8.6 percent and 20.7 percent, respectively, to 9.5 percent and 22.0 percent, respectively.”

Should we expect the strong trend to continue? It very well may be a white hot American summer. In particular, and thinking about the upcoming May US nonfarm payrolls report, the US labor market is in great shape for the next few months with favorable tailwinds:

- rising vaccination rates allow for great mobility, crucial for small businesses;

- public schools are reopening, which allows parents (mainly women) to rejoin the workforce as at-home childcare needs are reduced;

- and unemployment insurance benefits will be rolling off in a few months, so many may want to get their job under their belt before their government-sponsored runway ends.

A Closer Look at the May US Nonfarm Payrolls Report

The main issue for the US Dollar when it comes to the May US Nonfarm Payrolls report is whether or not the US labor market regained its momentum after a disappointing April report. After all, the prior month’s reading came in at +266K against an expectation for a round +1000K (or +1M) jobs added.

Market participants are indeed expecting that May reading will show a strong rebound, given that jobless claims continue to trend lower and vaccination rates have improved, leading to many lockdowns and/or restrictions otherwise to be lifted. Consensus forecasts are looking for a reading of +650K, which should help the unemployment rate (U3) drop further lower from its still-lofty 6.1% level. Meanwhile, the US labor force participation rate is still a meager 61.7%.

The May ADP employment change report, coming in at +978K, will likely bias expectations higher heading into the official release on Friday morning.

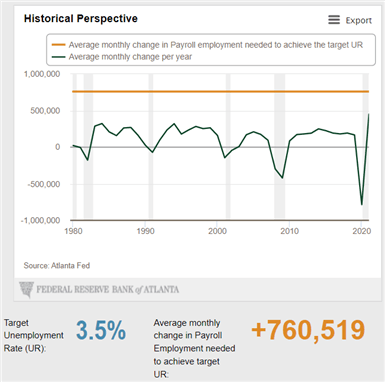

Atlanta Fed Jobs Growth Calculator (June 2021) (Chart 1)

Even if there are good jobs data, there is still a long ways to go before the US reaches ‘full employment’ as experienced pre-pandemic. According to the Atlanta Fed Jobs Growth Calculator, the US economy needs +761K jobs growth per month over the next 12-months in order to return to the pre-pandemic US labor market of a 3.5% unemployment rate (U3) with a 63.4% labor force participation rate.

Taper Timeline

There’s been a lot of conversation around the perceived timeline of the Federal Reserve’s plan to taper its asset purchases, a discussion likely to be revived regardless of the outcome of the May US NFP report. This is in part thanks to heightened activity across the Fed’s open market desk (with respect to reverse repos) as well as news that the Fed is winding down its corporate credit portfolio.

In consideration of these facts, it appears that market participants have the taper timeline priced as such:

- June through September 2021 = taper talk

- September 2021 = indication taper is coming

- December 2021 = taper targets announced

- January 2022 = taper begins

- September/December 2022 = taper ends

- March 2023/June 2023 = first rate hike (3-6 months post-end of taper)

Broadly speaking, even if it’s an insignificant amount of funds, the Fed winding down is pandemic credit portfolio is completely sensible given the fact that the RRP facility has been tapped so frequently recently. The system is flush with cash; companies are well capitalized. Markets don't need to worry about the 'tides of insolvency dragging the illiquid out to sea.'

Read more: The Scary Fed Number Everyone is Talking About

DailyFX Economic Calendar for Friday, June 4, 2021 (Table 1)

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist