S&P 500, Dollar, EURUSD, GBPUSD Talking Points:

- The wavering in risk trends trend into outright retreat this past session and the S&P 500 seemed to lead the way

- Wavering stimulus conviction and recognition of growing coronavirus hotspots have added to recognition of indulgent speculative appetite

- True risk remains unresolved; while the Dollar is better positioned for stimulus debate, Sterling awaits another Brexit deadline, Euro mulls tariffs and Aussie Dollar feels China’s pressure

Risk Trends Retreat Owing to an Absence of a Clear Motivation Rather than Owing to One

More often than not, my first fundamental look at the market is to assess whether ‘risk trends’ have caught any significant traction. This universal conduit in the financial system can override most individual themes or events and pull the entire market along for the ride. As of this past session, there seemed to be a market shift towards risk aversion. Not only was my preferred, imperfect representatives of speculative appetite – S&P 500 and Nasdaq 100 – on the lam; but there was further retreat registered from emerging markets (EEM), junk bonds (JNK) and carry trade (AUDJPY) among other measures. Breadth is one factor in risk aversions reach, but so is intensity. While the retreat may have been broad, it registered more as a breather rather than a committed reversal. That is an important distinction as it is the difference between a temporary reprieve versus a genuine trend. What we need to genuine conviction is a capable driver to charge fear or greed.

Chart of S&P 500 with 50, 100-Day Moving Averages, Consecutive Candles (Daily)

Chart Created on Tradingview Platform

The Coronavirus Threat Rears its Ugly Head and GDP Outlook May Actual Land

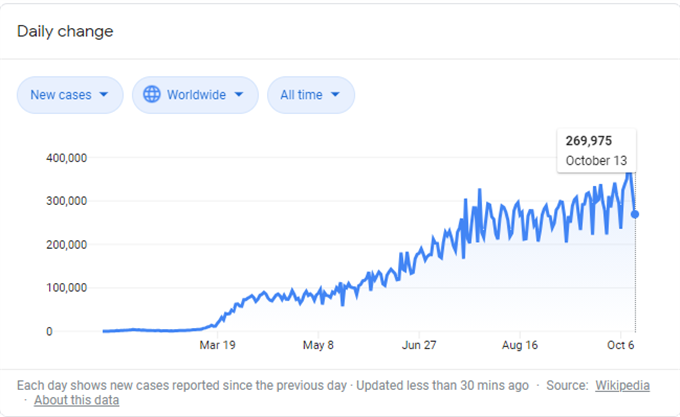

Though it is a catalyst rather than the ends that sentiment represents, the coronavirus has proven itself to be quite the capable motivator for the global economy and financial system. That said, the headlines have taken a material turn for the worse around the pandemic and growth interpretations may start to seep through otherwise impenetrable speculative appetite. Worldwide cases on a 7-day average are pushing to record highs while certain regions are starting to respond to their own acute resurgences. UK Prime Minister Boris Johnson is supposedly weighing circuit breakers owing to the renewed spread in England while Italy’s numbers have hit a fresh record high and France is supposedly on the cusp of restoring curfews. The human toll this represents aside, there is also the question of whether this is a global risk burden or a relative market consideration as with EURUSD.

Chart of Worldwide Coronavirus Cases (Daily)

Chart Created by Google with Data from Wikipedia

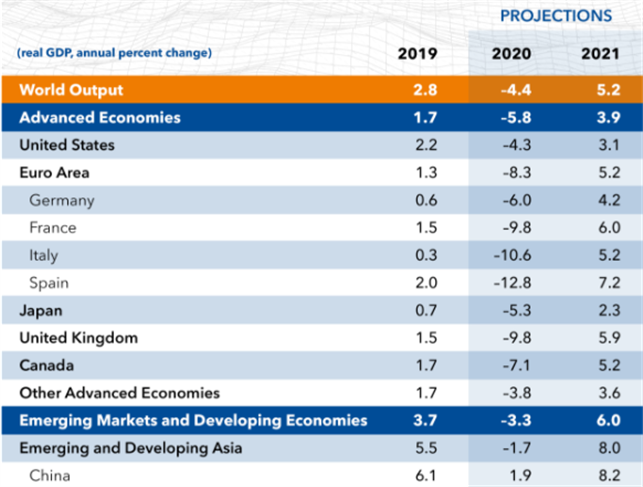

Another theme that hasn’t drawn the attention it seriously deserves is the recent growth forecasts that have crossed the wires. The IMF’s modest upgrade to its 2020 projection and the downgrade to its 2021 and beyond views doesn’t seem to have materially altered market convictions. With the coronavirus tally rising and either explicit decisions by governments to re-shutter economies or watch the markets take steps on their own, this may grow to be too significant to overlook. In the meantime, a wholly different venue for growth projection may draw greater interest from the market crowd. Amazon’s annual ‘Prime Day’ event is drawing to a close, and this pandemic-attuned pseudo-holiday may better reflect actual consumption health better than anything we have seen in ‘official’ channels.

Table of Global Growth Forecast from IMF’s WEO

Table from IMF

Stimulus is Tinder for the Dollar, Not Risk Trends

While I am keeping track of the untapped systemic potential, stimulus remains one of the active motivators – even if just through heavy interpretation. US stimulus discussions seem to be a key fundamental concern among traders whether through my own poll or via Google search interest. That said, the influence of the impending US Presidential election will likely stand as a constant encumbrance to actually realizing the much-needed relief for Americans either out of work or under-employed. Should this situation continue to drag out, it may eventually drag down US assets and the Dollar, but tolerance to marginal change is high. Alternatively, if the government does finally find compromise, I will be looking to the Dollar rather than US indices to respond given the former’s state of earnest discount.

How has the Dollar traded around previous Presidential elections? Read this article to see how the Greenback has fared in previous decades’ elections.

Twitter Poll on Most Market Moving Theme Next Week

Poll from Twitter.com, @JohnKicklighter

Taking a look at the Dollar’s standing, the picture is significantly different relative to the likes of the S&P 500. While the index is just off of a record high, the USD measure trading just off multi-year lows and has put in for consolidation that seems to set the stage for reversal with proper motivation. That same perspective seems to translate to pairs like EURUSD, USDCAD and others.

Chart of DXY Dollar Index with 50 and 100-Day Moving Averages (Daily)

Chart Created on Tradingview Platform

Unique Event Risk in Another Brexit Deadline and Rekindled Trade Wars

Keeping the anchor to the Dollar, there are other major currencies’ developments that can spur volatility from the majors or the relevant crosses. GBPUSD for example saw the Sterling rally impressively this past session. The move is remarkable against a backdrop where the PM is considering instituting further lockdowns owing to Covid and reports that the UK and EU were still at an impasse on trade negotiations at the former’s self-imposed deadline today. Keep tabs on the Sterling’s volatility and the headline as the artificial clock runs out.

| Change in | Longs | Shorts | OI |

| Daily | -14% | 3% | -7% |

| Weekly | -18% | 23% | -4% |

Chart of GBPUSD with 50 and 100-Day Moving Averages with 20-Day Historical Range (Daily)

Chart Created on Tradingview Platform

Another pair I am watching a little more closely is AUDUSD. This has a sensitive to risk trends and is another Dollar pairing whereby the benchmark looks like a loaded spring. Yet, the more concentrated fundamental consideration is the representation of China’s global situation via this pair. China is increasingly finding itself at odds with global counterparts and moving to domestic sources of growth to compensate its lost trade support. If I were only waiting to see a slowdown in Chinese health (such as with Monday’s 3Q GDP), it may never come. However, another spark may arise where AUDUSD is concerned as it is reported that China is planning to ban Aussie coal imports – a significant economic concern.

Chart of AUDUSD and Inverted USDCNH with 50, 100-Day Moving Averages (Daily)

Chart Created on Tradingview Platform

If you want to download my Manic-Crisis calendar, you can find the updated file here.

.