Dollar, EURUSD, FAANG, AUDUSD Talking Points:

- The Dollar’s respite didn’t last very long, not surprising between the deepest contraction in US GDP since the Great Depression and talk of election delay

- EURUSD will be a key pair to watch with the US still debating stimulus to replace expiring benefits while Europe (EZ, France, Italy, Spain) report 2Q GDP Friday

- My top focus for gauging risk trends will be the after-effect of astounding FAANG earnings releases – with the Nasdaq open chief but Asia and European sentiment on my radar

A Fundamental Convergence of Recession and Election Uncertainty

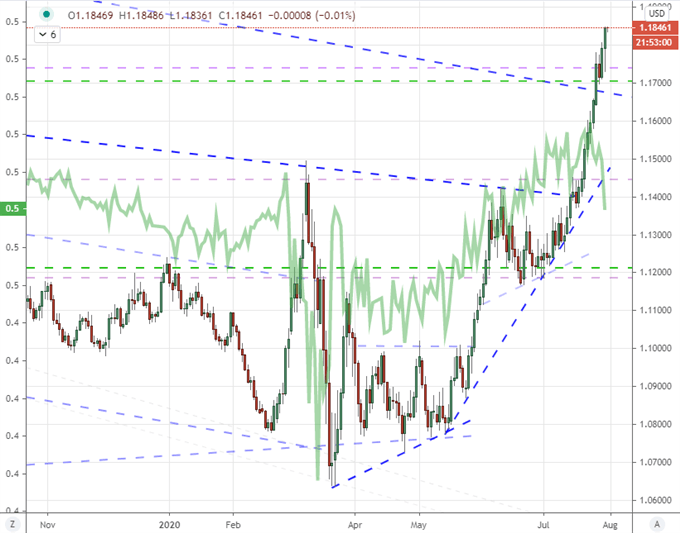

There are facing a significant fight over the course of risk trends to close out the final session of this week and month. Between the fallout in key event risk, the remarkable performance of tech earnings and the lingering possibility of another wave in US stimulus; there is plenty of potential for volatility – if not outright trend. Through this past session, one of the most productive moves to return to form was the DXY Dollar index’s ninth daily slide in 10 trading sessions. That would push the benchmark to a multi-year low and further the notion of a serious multi-year trend channel breakdown. The bearish conviction was bolstered by the benchmark US 10-year government bond yield’s slump to a fresh record low in its own right. Yet, this wasn’t a Fed or interest rate move. Instead, Twitter remarks by President Trump suggesting a delay in the November 3rd election should be considered added further tension to an already volatile event.

Chart of DXY Overlaid with US 10-Year Treasury Yield (Daily)

Chart Created on Tradingview Platform

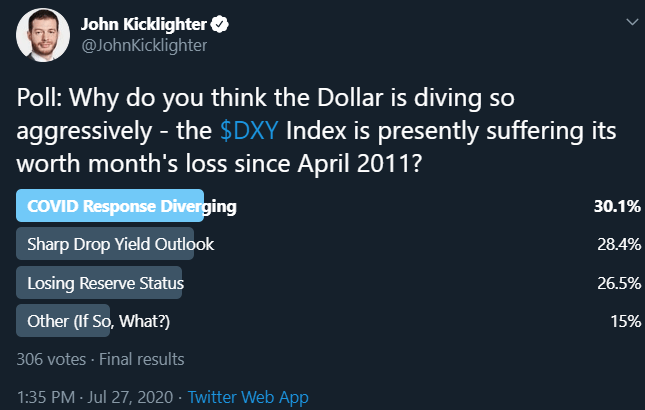

Election season volatility that converges with the natural seasonal swell could present a risk aversion drive but the Greenback is currently not in good form to take advantage of that mix – it is instead increasingly at the center for much of the uncertainty. Looking back to the results to one of my previous polls, the majority of respondents (approximately 62%) said stimulus was the foundation to the much of the current risk appetite. Therein lies an issue as the US government has struggled to work out the next leg of stimulus for the world’s largest economy. That said, another note around the White House was suggestion that President Trump was ready to support an extension of the expiring $600 addition to the soon-expiring unemployment benefits. This may ultimately prove a spark for some much needed recovery from the Greenback, but I am not holding my breath.

Twitter Poll: ‘Why is the Dollar Dropping?’

Poll from Twitter.com, @JohnKicklighter Handle

Meanwhile, the world’s most liquid currency pair – and arguably its most heavily traded asset – EURUSD has pushed to a fresh two-year high. This climb is somewhat impressive considering the Euro fundamentals themselves were not particularly reassuring. Thursday, Germany’s 2Q GDP update offered a worse-than-expected -10.1 percent slump for Europe’s largest economy. Through Friday, we are due figures for the same period for France, Italy, Spain and the Eurozone at large. This will prove important context. For the Dollar’s part, the incredible US 2Q -32.9 percent was ‘better than expected’ but still the worst turn for the economy since the Great Depression. Strength in these times is the very definition of ‘relative’.

| Change in | Longs | Shorts | OI |

| Daily | 1% | 1% | 1% |

| Weekly | 61% | -45% | 2% |

Chart of EURUSD with DAX-Dow Ratio (Daily)

Chart Created on Tradingview Platform

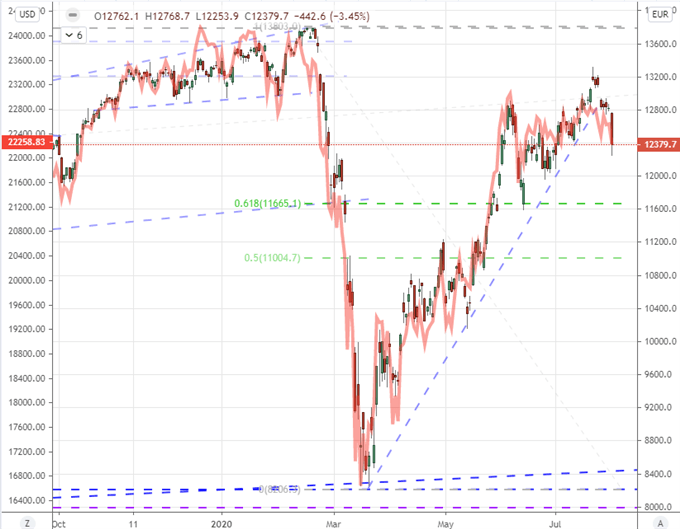

Anticipating a FAANG Response for Risk Trends

Looking out over the final trade of the week and month, my attention is set fully on risk trends. In particular, the opening hour of the New York session will prove very important for my evaluation of the speculative backdrop. After the close of US trade on Thursday, there was a run of unmistakably better-than-expected earnings data from some of the larges (by market cap) tech firms. Facebook earnings beat $1.80 earnings per share against $1.39, Google $10.13 versus $8.21, Apple $2.58 to $2.04 forecasts (and a 4-for-1 stock split) and Amazon truly astounded with a $10.30 to $1.50. This is as clear a ‘strong’ outcome as they come. If risk appetite cannot find a foothold on this strong support for a top performing category of speculative appetite, it will invite deserved skepticism. If Friday closes lower, it could act to topple of the FOMO that has held so strong.

Chart of Nasdaq Futures Overlaid with Nasdaq 100 Spot Index (Daily)

Chart Created on Tradingview Platform

Ultimately, the US session will be my principal read on the health of global sentiment between earnings, recession confirmations and other systemic issues. That said, if risk appetite were gaining earnest traction, it is reasonable to expect the bid to arise in more than just the FAANG members or Nasdaq 100. The blue-chip Dow and broad S&P 500 should find support if there is a groundswell afoot. Beyond that, risk appetite is global, so a reliable risk run should also show through Japan’s Nikkei 225 and Germany’s DAX 30 indices which broke lower through their own Thursday sessions. If these regional leaders don’t catch a spark, the high water mark for US markets moving up to speed from a dead stop is much further away.

Chart of DAX and Nikkei 225 in Red (Daily)

Chart Created on Tradingview Platform

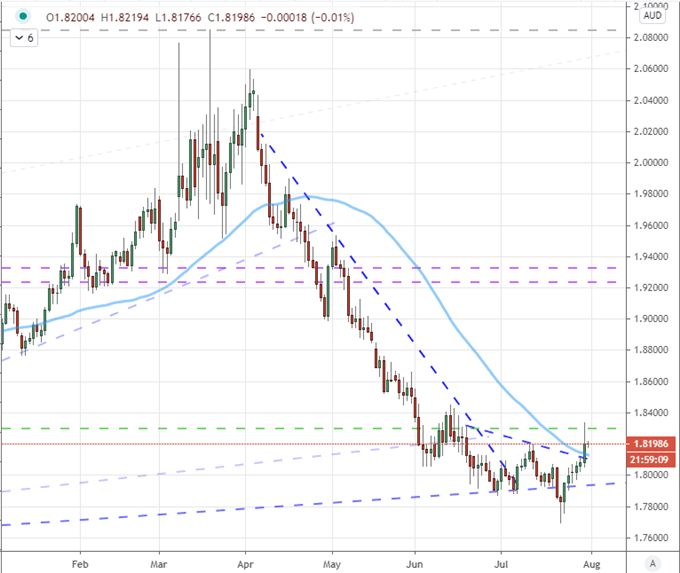

Keeping Track of the Remarkable Australian Dollar’s Climb

On a final thought, I am continue to keep tabs on the Australian Dollar given its remarkable position developed over these past three to four months. GBPAUD this past session seemed to earn a technical, counter-trend break; but such a move is not likely to serve as a momentum generator for the Aussie currency by itself. For AUDUSD, the 5-week rally is the longest since January 2018 (when it peaked) and pushing technical boundaries. For AUDCAD, AUDJPY and EURAUD; the situation is the same. The technicals alone wouldn’t be so remarkable if it weren’t for the crush in local yield, the unfavorable impact from strained Chinese relations and a revival in the coronavirus curve. Should the market chose to pay attention, this currency would look stretched.

Learn how carry trade works in the currency market in our education section.

Chart of GBPAUD with 50-Day Moving Average (Daily)

Chart Created on Tradingview Platform

If you want to download my Manic-Crisis calendar, you can find the updated file here.

.