Trade War Talking Points:

- Growth troubles rebounded through the end of the past week with November PMI's showing economic contraction in Japan, Germany and the UK

- Trade wars will be a persistent risk given the uncertainty of US-China and US-EU relations compounded by limited communication

- Structural complacency will converge with extreme seasonal liquidity conditions with the US Thanksgiving holiday - but don't ignore risk

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 4Q 2019? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Volatility and Liquidity are the First Consideration for the Week Ahead

There is a natural expectation among many in the market that the week ahead will settle comfortably into converging streams of long-running complacency and reliable seasonal liquidity drain. On Thursday, the US will be offline for the Thanksgiving holiday which historically levels out speculative activity across the globe. As far as the key technical standings and meaningful fundamental themes staging markets at present, there are certainly opportunities for targeted volatility developments. Yet, tapping into the systemic fear or greed of the masses would be exceptionally difficult given our present conditions. For general 'risk' trends, I will certainly keep tabs on the S&P 500 and Dow. Where the stress cracks in an over-leveraged speculative backdrop is not as obvious at the surface level for the likes of global equities, emerging markets, carry and other traditional measures; the record highs of these key US indices can amplify the attention they draw. What's more, their status as the leading 'bullish leaning' benchmark can potentially override the liquidity breaks.

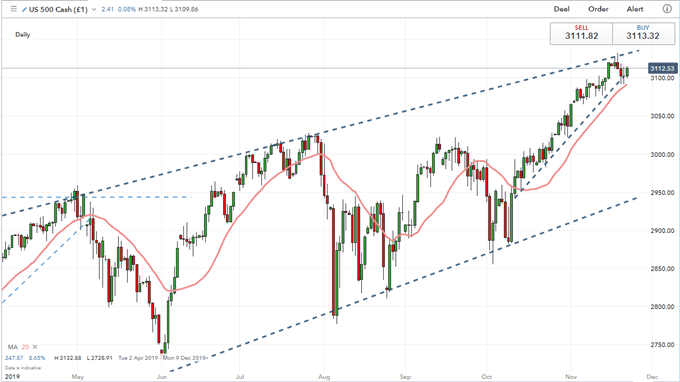

Chart of S&P 500 with 20-Day Moving Average (Daily)

Chart Created with IG Charts

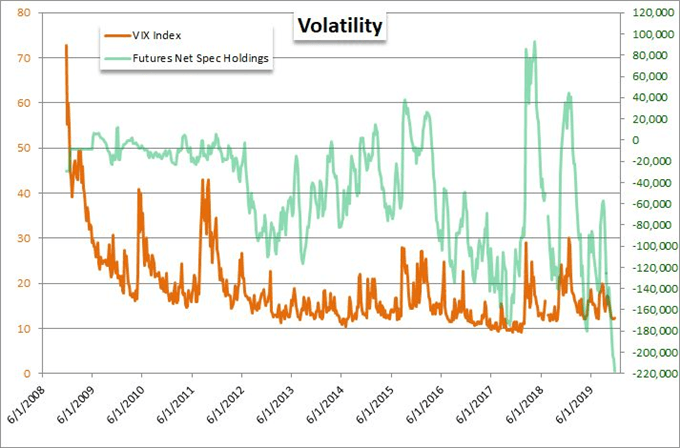

My top concern, however, moving forward is not high-profile pace-setters tripping technical levels nor even event sparks setting off loaded fundamental themes. Rather, I'm far more mindful of the exposure behind the financial system. The Dow pushing a record high represents its own overindulgence in sentiment as it insinuates pricing in the best possible projection of growth and/or return potential. That is certainly far-fetched. Yet, beyond that difficult-to-justify valuation, there are extreme measures of exposure across the system. Increasing a collective position to the financial system to earn increasingly smaller rates of return is a hallmark of the past half-decade. Yet, with that escalation, the exposure to risk grows to levels previously unheard of. This is reflected in the slow build up similar to the 'boiling frog' parable with unprecedented leverage among investors, central banks, consumers, businesses and governments. It is also a more immediate measure through benchmarks like the VIX. The traditional reading of demand for hedge and general fear, speculative futures traders extended their run of record net short interest for a fourth consecutive week.

Global Growth Concerns Revived Yet It Seems Biggest Impact is Dollar's 'Least Strained' Status

The outlook for global growth has wavered on the of serious trouble for some time now, but the pressure seems to be building in earnest once again. Through the end of this past week, a global run of PMI figures offered a timely overview of our economic bearings; and the result was not at all encouraging. The Markit's November update gave a troubling signal for the world. The Australian composite dropped from a neutral 50 reading to 49.5 (anything below 50.0 indicates contraction in the economy or sector) while the Japanese reading ticked higher from 49.8 to 49.9 - still tracking a slump. In Europe, the German composite ticked lower to 49.2 (from 49.3) and the Eurozone reading unexpectedly dropped to 50.3 but the UK took a marked downturn from 50.2 in October to 48.5. The only bright spot seemed to be the US figure which accelerated from 50.9 to 51.9. That won't be enough to turn our global course.

Chart of World Uncertainty Index and Wilshire 5000 (Quarterly)

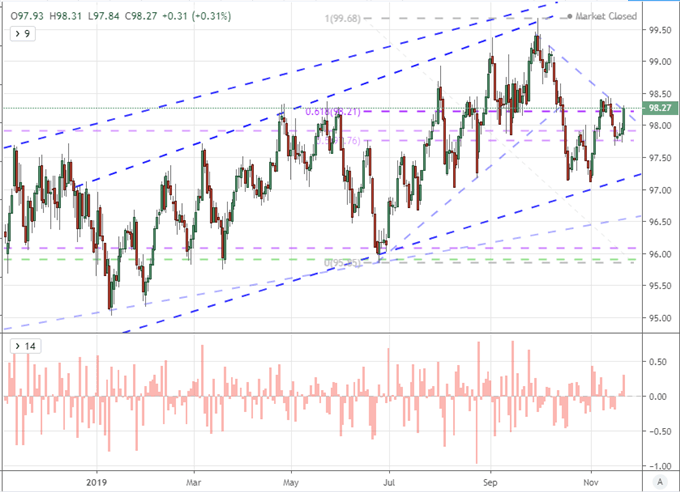

The stand out performance from the US figures may not have reinforced global risk appetite, but it could have very well charged the Dollar through the short-term. The DXY Dollar Index jumped surged higher through Friday in something of a recovery move. That said, the potential for follow through for the Greenback and/or US assets is fairly low. Between the PMIs and the meaningfully University of Michigan (upward) revision, there was enough to nudge Fed forecasts up measurably and in turn lift the Dollar. This is not a spark that will fuel follow through into the foreseeable future though. Ahead, we have the Conference Board's consumer sentiment report and the Fed's favorite inflation reading (PCE deflator), but I will hold my expectations for consistent outperformance low.

Chart of DXY Dollar Index and 1-Day Rate of Change (Daily)

Chart Created with TradingView Platform

Trade Wars Remain the Most Pressing Unscheduled, Systemic Threat

Another theme of significant merit moving forward is the unpredictable trade war. The close of this past week ensure this matter would remain at the forefront of concerns as both the US-China and US-Europe skirmishes were put on an unstable footing. Between the two different fronts, the former is more likely to generate volatility moving forward. It was reported from White House sources that President Trump intended to move forward with the December 15th escalation in the Chinese tariff list to essentially encompass all of the country's shipments if there is no 'Phase One' agreement. That said there was caveat for Executive good will which makes this as variable as ever. I will operate with the expectation that further headlines are on the immediate horizon, but that volatility is unlikely to pose direct opportunity with the addition of liquidity challenges.

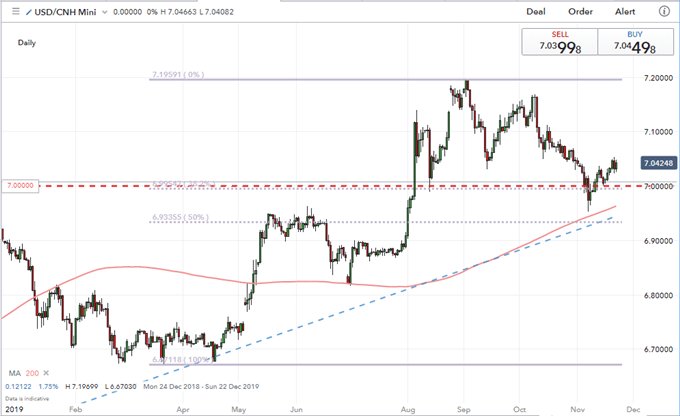

Chart of USDCNH with 200-Day Moving Average (Daily)

Chart Created with IG Charts

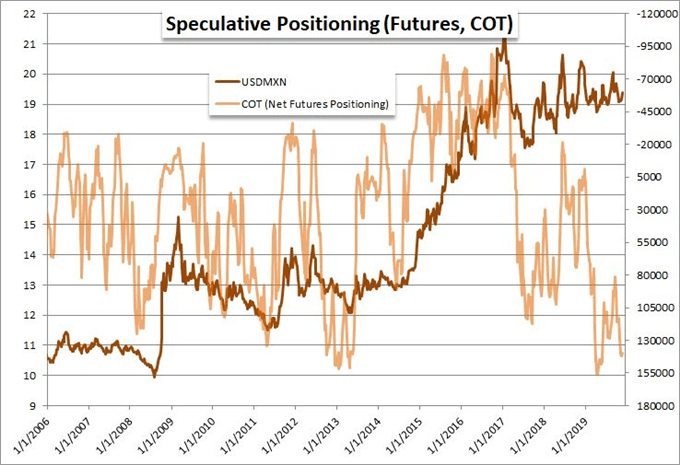

Unfortunately, trade wars are not just a US-China matter. There are further tensions to be registered between the world's largest economy and its immediate neighbors (Canada and Mexico) and its largest economic counterpart. Despite a loose interest in the USMCA many months ago, there hasn't been an adoption of the program meant to replace NAFTA. Net speculative positioning in USDMXN should be something to consider as you weigh these markets. If we consider the probable scenarios that could utterly change our global conditions, I would watch most closely the status of trade between the US and the Eurozone. Friday saw the EU Trade Commissioner issue a proposal agreement with the US an attempt to steer the relationship. That said the probability that the US pursues the Section 301 after the deadline for the Section 232 passed is dangerously high.

If you want to download my Manic-Crisis calendar, you can find the updated file here.

What fundamental themes should you follow next week? How will they impact the markets at large? Sign up for our webinars to better evaluate how market developments are shaping markets. Sign up on the Webinar Calendar.

.