Volatility Talking Points:

- VIX and other asset volatility measures will remain charged, but risk benchmarks like the S&P 500 have strong incentive to hold fast

- Event risk will pick up into the second half of the week, but liquidity expectations for the US holiday weekend are already bearing down

- With a rare break in trade war headlines, recession fears gained prominence as the 2year/10year yield curve inverted with authority

See what live coverage is scheduled to cover key event risk for the FX and capital markets on the DailyFX Webinar Calendar.

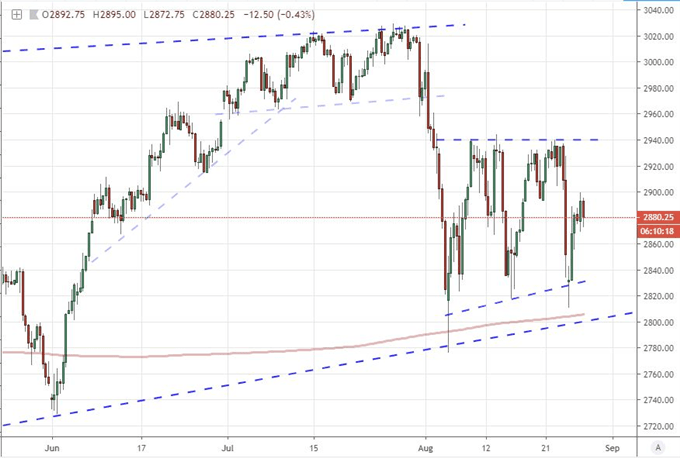

Extrapolating Global Risk Trends from a Volatile S&P 500 Range

I like to us the US indices as my baseline for 'risk trends' owing to the scale of the US markets (unrivaled) and the ubiquity of equities (the most heavily represented asset class in the average portfolio). In particular, the S&P 500 has the greatest trading profile given the turnover in its derivatives. If this benchmark stands as a good proxy for the broader markets, its present technical and conditional standing could provide an informative perspective for strategy selection. There is a well-defined range around the market that has stood for almost the entirety of August - between 2,940 and 2,800. The barriers are even more remarkable when we consider the volatility that they are attempting to contain. There have been a number of hearty swings from resistance to support and back again these past weeks. And, more often, when activity levels hold to significant heights, a break is inevitable. As it happens, this same pattern is playing out across most assets with a similar anchor to sentiment. Volatility measures for Yen crosses, emerging markets and Treasury yields are all elevated - though most of underlying measures for these derivatives is refusing a clear trend.

Chart of S&P 500 Emini Futres and 600 Period Moving Average (8-Hour)

Chart Created Using TradingView Platform

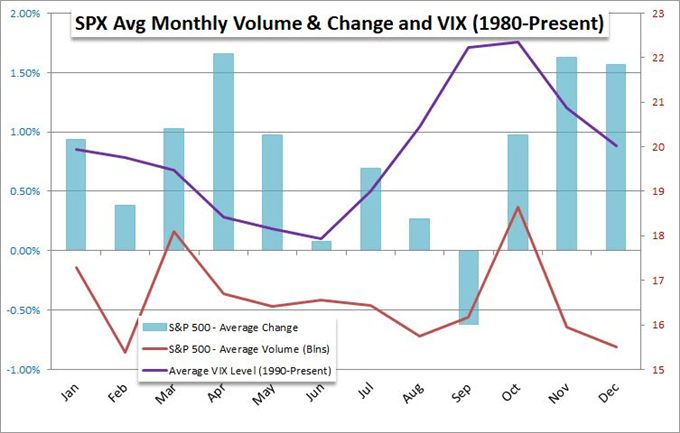

As established as the US index's chart pattern is, I would not put much weight into its durability if we were trading through 'normal' conditions - such as any time during the fall trading season. Though, as it happens, we are in the thick of the seasonal lull. This week leading up to the Labor Day holiday weekend in the US is the height of anticipated quiet. That won't curb the developments that can spur sharp moves across the financial system - a jog in trade wars, fresh recession signals, etc - but it can effectively limit the reach of the market's ambitions. Before the forthcoming holiday weekend, the barrier to breakout - much less follow through - will be particularly strong. Yet, in balanced proportion, the month of September will bring with it the seasonal swell in volatility and worry over the worst performing calendar month of the year. Shifting the market's default view to a dovish perspective given our frequent fundamental issues of late could prove a loaded backdrop.

Chart of Seasonal S&P 500 Performance and Volue Along with VIX

Trade Wars Go Quiet and Recession Signals Take Their Place

Looking for the standard fundamental drivers behind our more substantial market heaves these past months, there was a remarkable absence of updates on trade wars through Tuesday's session. It was inevitable that we eventually find some pause to the drama following last week's dangerous escalation between the US and China in their ever-growing economic fight. Despite the very loose reports of thawing commentary between the two countries leaderships, there has been no clear de-escalation from the higher tariff rates (25 to 30 percent and 10 to 15 percent in the next wave) and new range of products coming under tax ($300 billion) on the US side nor China's fresh levies and restoration of auto tariffs. And yet, no news is construed as good news when it comes to a situation where the fundamental trajectory is steady deterioration.

Monetary policy on the other hand would earn greater appeal among hungry traders. President Trump was on the wires once again with his typical verbal bombing run of the US central bank. The tune was familiar one from the aggrieved leader. He suggested that the Fed enjoyed seeing US-based manufacturers struggle and that was the reason for the maintenance of their relatively hawkish policy setting. It was clear that his criticism was not aiming for lower rates to spur lending and underlying GDP, but rather he was interested in projecting the effect of the United States' trade war pressure. Against this backdrop, a very provocative op-ed generate considerable attention on monetary policy. Former New York Fed President Dudley wrote that the central bank shouldn't forgo is mandate and cater to the President's demands. The real controversy followed his suggestion that the trade war was among the greatest threat to the outlook and therefore a policy bearing that diminished Trump's reelection could be theoretically preferable in sheer risk scenario terms. The Fed saw it necessary to release a statement rejecting the remarks, but the remarks will not simply be overlooked.

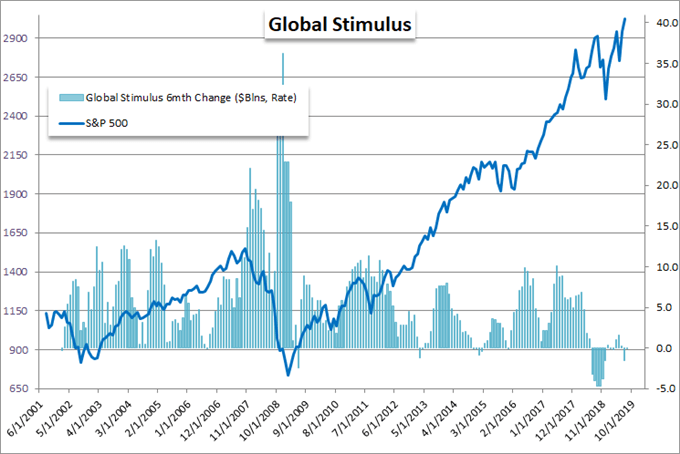

Chart of S&P 500 Overlaid with the 6-Month Rate of Change in Stimulus Programs (Monthly)

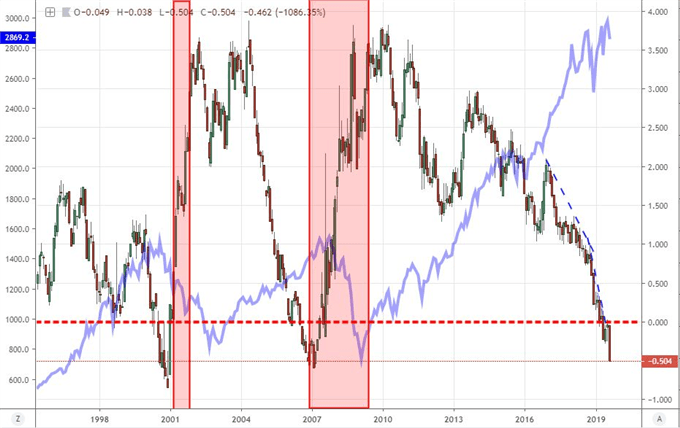

For true heft this past session, recession fears would move back up to top fundamental spot as much through the moderation of the competing issues as the charge that growth worries itself would generate. There was a range of economic data with a traditional growth perspective this past 24 hours. The US economy was troubled by the orders component of US durable goods orders last month hitting a near three-year low, Germany's 2Q GDP details showed weakness in critical consumption and business investment, while China's industrial profits proved the only genuine bright spot with a 2.6 percent growth. That said, I wouldn't put too much emphasis on the data. In contrast, the preferred market-based signals are flashing warning lights so bright that it is hard to ignore. Previously reticent to follow the 10year3month yield curve into true reversion, traders' favorite 10-year2-year curve dove below the zero mark Tuesday. To added a little more emphasis to the situation, the 30-year yield would also hit a record low close. While not an imminent indication of economic collapse, there is fairly consistent signaling from these occurrences.

Chart of 10year3month Yield Spread with Recessions Overlaid with S&P 500 (Monthly)

Chart Created Using TradingView Platform

EURUSD Weighing Its Fundamental Guiding Light, Pound and Swiss Franc Deserve Consideration

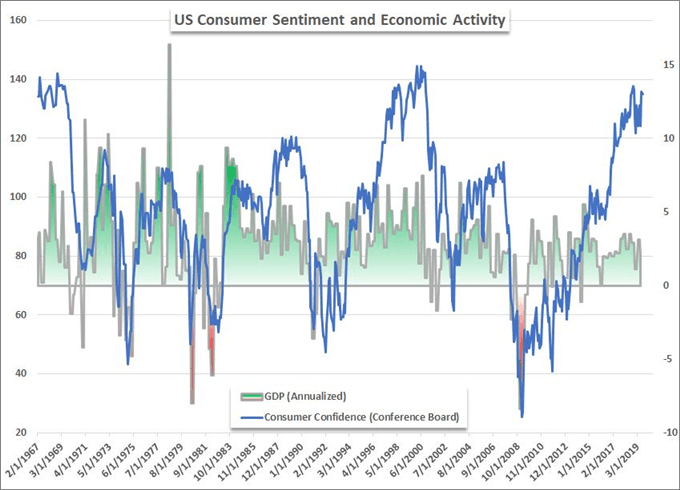

Looking for regional opportunities - relative FX plays - the majors are showing limited response to their own fundamental highlights. From the Dollar, the August consumer confidence survey from the Conference Board offered clear opportunity for those with an agenda to interpret the data to suit their needs. US Commerce Secretary Ross highlighted the 19-year high current conditions figure, while skeptics would draw upon the softer expectations component and the record disparity between this signal and the University of Michigan's own survey. Ultimately, the report is still in remarkably strong standing with an increasingly troubled backdrop (manufacturing, exports, housing prices at the higher end, etc), but the market's interests lie elsewhere. A focus to Fed tempo or the White House turning to currency wars could earn true traction.

Chart of Consumer Confidene and US GDP (Monthly)

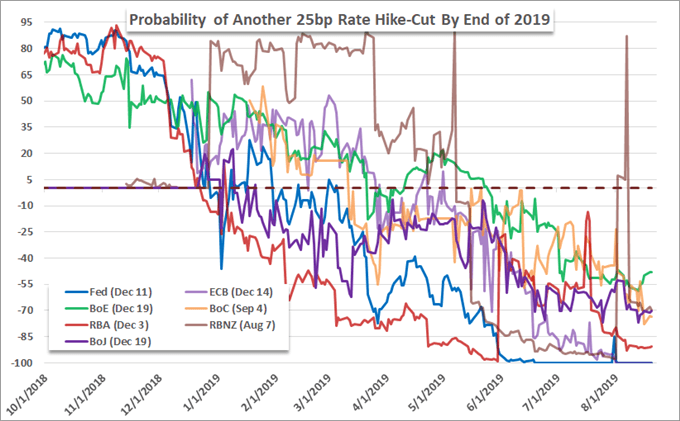

Meanwhile, the Euro was supposedly facing a significant improvement in its own fundamental backdrop. Following the breakdown of the coalition Italian government, it seemed Five Star and the Democratic Party were heading towards a collaboration which would see the government stick to the EU's 2020 budget. From the shared currency's perspective, that tempers a serious threat against regional stability. Nevertheless, the Euro dropped on the day. Perhaps the overwhelming expectation of an ECB rate cut (95 percent according to swaps) at its upcoming September 12th meeting carries more weight?

Chart of Probability in Central Bank Policy Adjustments by Year End (Daily)

A few other currencies deserving a frequent evaluation moving forward include the Pound, Swiss Franc and Australian Dollar. The Sterling is still anchored to Brexit proceedings, but the positioning by the government to thwart Parliament's efforts to negate a 'no deal' scenario point to the trouble still in the foreground. The Pound VIX is steadily growing, but the currency managed to gain further traction Tuesday. Which signal should we take more seriously? From the Swiss Franc, the name of the game is exchange rate pressure. We already know the SNB is intent in preventing steady appreciation of its local currency, but what is the turning point for escalating their efforts? The midpoint of the range that has formed since the January 15, 2015 exchange rate floor collapse is as relevant a point as any. Then there is the Australian Dollar. This is a currency that has direct trade war ties, but it is also facing some direct data in 2Q construction today and private investment tomorrow. This is not as reliable a mix, but it is certainly loaded.

If you want to download my Manic-Crisis calendar, you can find the updated file here.

What fundamental themes should you follow next week? How will they impact the markets at large? Sign up for our webinars to better evaluate how market developments are shaping markets. Sign up on the Webinar Calendar.