Trade Wars Talking Points:

- Though no 'major' escalations have followed the previous week's new US tariffs and USDCNH cross of 7.00, trade wars remain focus of fear

- Chinese data for July, diplomatic pressure around Hong Kong, South Korea-Japan moves and No-Deal Brexit support all qualify as fronts

- Data on US business sentiment and CPI, UK jobless claims and Eurozone investor sentiment are all important, but reserve weight to themes

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2019? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Trade Wars Still Resonating Globally

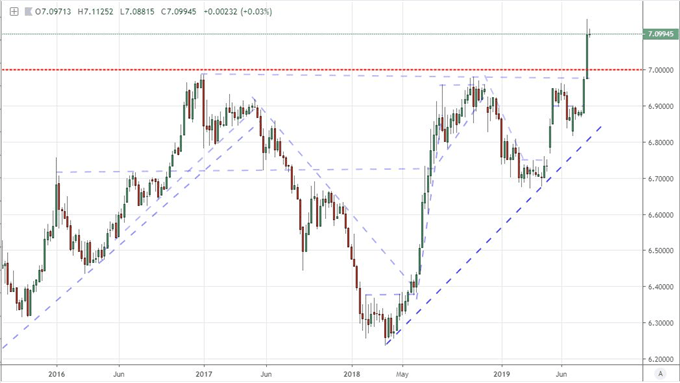

Thankfully, there was a break from the recurring instance of weekend escalation in thematic fundamental threats that has generated severe moves in the capital markets on Monday open more than a few times these past weeks. Last week, the charge was the latest trade war moves between the US and China - the former announcing another $300 billion in imports facing a 10 percent tariffs on August 1st and the latter allowing the USDCNH clear 7.0000 when markets opened on August 5th. The market's panic response to further moves to disadvantage economic peers has steadily declined with each major iteration, but the cumulative pain continues to build regardless of the short-term speculative response. That is the contrast between dip-buying opportunism versus the long-term trajectory problems that we are facing in this market. Between the US and China, the updates were in more traditional data. China reported its aggregate financing grew only 1.01 trillion versus 1.63 trillion expected while new loans slowed to 1.06 trillion against 1.28 trillion forecast. Ahead, we will find foreign direct investment sometime over the coming week while Wednesday morning will definitively offer industrial production, fixed assets and property investment.

Chart of USDCNH (Weekly)

What truly worries me is the realization that the economic fight is not isolated to the US and China. Involving similar forces, the diplomatic tension between the two countries over the situation in Hong Kong threats to raise more pressure on their direct trade confrontation. Another Asian center for rising tension though can readily be found between Japan and South Korea. The two major economies have escalated trade actions between themselves in a series of retaliatory moves that began with Tokyo's restriction on three chemicals necessary for the production of hardware in consumer electronics. The most recent move saw South Korea remove Japan from a list of trusted trading partners which would slow trade between the two even further. For the United States' part, it isn't a one-region focus as the EU is moving forward with the digital tax that is to be applied to top tech firms that are primarily domiciled in the United States. It isn't far fetched to expect the Trump administration to interpret this as a trade war move against the US itself. In the the meantime, UK Prime Minister Boris Johnson reportedly spoke to the White House and the latter said it "enthusiastically" supported a no-deal outcome in the former's Brexit negotiations. Encouraging aggressive trade policies globally.

Risk Sensitivity Still Clear in Assets and Implied Volatility

Trade wars continue to build concern over the state of global growth with various official readings, sentiment surveys and favored market measures continue to raise the stakes for expansion. Building on previous economic readings from major central banks, governments and external parties from the past weeks, the IMF's warning into the weekend that continued trade war pressure on China could threaten its growth felt particularly relevant. Meanwhile, Goldman Sachs' chief economist joined a growing number of prognosticators that are warning a continued trade stand off could push the world's largest economy towards stall speed. Further for the US, the NY Fed's consumer expectations survey showed fissures in confidence through July while market measures exposed specific concern - like the 30-year Treasury yield nearing a record low after its sharp 5.7 percent plunge Monday or reports that a $57.5 billion increase in US money market accounts brought the crisis-era haven to a back up to a 2008 peak exposure of $3.3 trillion in assets.

Chart of US 30-Year Treasury Yield and 1-Week Rate of Change (Weekly)

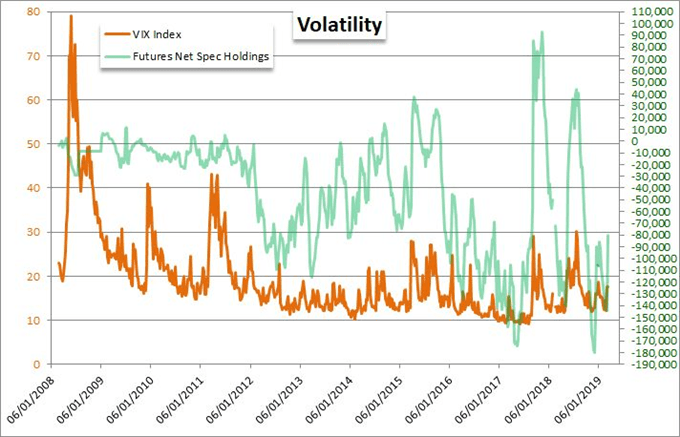

This economic fear leads naturally to desperation for the Federal Reserve and other central banks to act in a bid to offset the external problems. Even in theory, however, central banks put to the test are facing serious scrutiny over their ability to counter systemic pressure. That is perhaps a concern that is growing mainstream. This past session saw the S&P 500, Dow and other benchmark US equity indices slide to start the week. That doesn't charge a renewed fear over the state of sentiment, but it does curb the belief that complacency can readily revive the lurid bid for ever-diminishing yield. A strong indication that concern is building behind the speculative facade is the collective retreat in global indices, emerging markets, high-yield assets and carry. Another particularly-strong measure of strained sentiment is the unrelenting status of implied (expected) volatility. It is worth noting that net speculative futures positioning from the COT showed late last week that a familiar trade of complacency took a heavy hit with the jump in volatility registered in risk and the VIX.

Chart of VIX and Net Speculative Positioning in Futures (Weekly)

Dollar Is Due a Run of Data That is More Than Its Update

As the week progresses, we are due to run into a series of three key US data prints. The most closely observed release of the data run Tuesday will be the July consumer inflation reading (CPI). This is the market's favorite inflation indicator - part of the dual mandate for the US central bank - and will be particularly important given the first rate cut in a decade this past month. Whether the group will find it remotely possible to move at successive meetings - something that risks raising market concern that there is a crisis that the group is fighting an emergent crisis - depends on the support for action from these traditional measures. If they hold near target, it would either be seen as sacrifice of independence and credibility to cut rapidly or an unspoken fear of impending financial crisis. Neither would be good for the Fed and the future of global financial stability.

Chart of DXY Dollar Index and Implied Fed Rate for December from Futures (Daily)

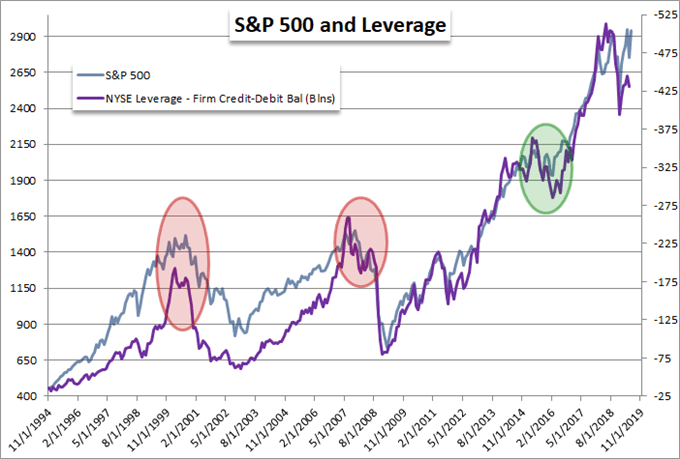

Also on the docket is the release of the NFIB's monthly small business sentiment survey. This is principally a trade war measure, but it is also rooted in regional economic health. Small businesses are responsible for the bulk of US employment as well as wages, therefore they are also indicative of consumer. Thus far, this group's view on the outlook has held firm against wavering consumer and bank sentiment for the world's largest economy, but the trade war pressure and natural cycle progression is unrelenting. Though a modest economic reading generally, it takes on greater status particularly if the data slackens. A distant third in terms of importance, but an indicator to monitor nonetheless, will be the 2Q US household debt update. I am of the particular view that the greatest risk across all regions and market participants (investor, consumer, business government) is the exposure to debt or leverage. With extreme readings, this becomes a more mainstream concern.

Chart of S&P 500 and NYSE Broker Leverage (Monthly)

Themes Versus Event Risk for Euro and Pound

Outside the top marks for the Dollar, the world's second most liquid currency should be gauged for its fundamental principals. The Euro holds a special status in the global financial market when the Dollar is at risk for a sudden capitulation from the Fed or unfavorable perspectives of trade. That is the primary reason I believe an equally-weighted measure of the Euro is holding up. Yet, when we consider its own fundamental troubles, there is plenty to weigh for the Euro. Italy's political troubles have been revived with the pressure to call a no-confidence vote and opinion polls that suggest an end to a stretched coalition government could bring a more concentrated anti-EU lead. Whether that is an issue for Italy or not is a point of debate, but its risk to the uniformity of the EU and Euro is not. Pit that general concern against the Eurozone investor sentiment survey from ZEW. This current reading is important from a fundamental perspective as it can weigh in on growth, unmoored monetary policy and trade fears; but the market has been reticent to dig that deep into the interpretation.

Chart of Equally-Weighted Euro Index (Daily)

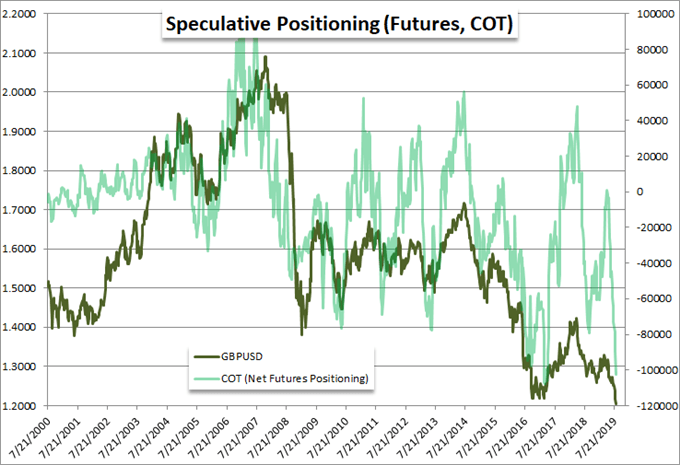

As for the Pound, last month's employment statistics are yet another milestone that we should watch for the ever-debatable health of the UK economy. Against the backdrop of the Bank of England's (BOE) Brexit-based growth warning, this figure will be evaluated for the cumulative economic impact of sheer anticipation of a poor outcome in negotiations. That said, the pain of a 'no-deal' Brexit outcome is the primary trouble for those trading the Pound. GBPUSD is within reach of three decade lows and EURGBP completed a record-breaking 14 weeks of consistent climb event if Monday offered a modicum of respite. Given that the new Prime Minister is unapologetic in his threat of a hard sever from the EU if they will not relent in the negotiations, the markets are reasonably proactive in their de-risking. Everything that we view for the Pound - whether it be data or market moves - should be viewed through the Brexit lens. We discuss all of this and more in today's Trading Video.

Chart of GBPUSD and Net Speculative Futures Positioning (Weekly)

If you want to download my Manic-Crisis calendar, you can find the updated file here.

What fundamental themes should you follow next week? How will the US CPI and Australian employment updates impact their respective currencies? How will they impact the markets at large? Sign up for our webinars to better evaluate how market developments are shaping markets. Sign up on the Webinar Calendar.