Trade War Talking Points:

- The new week opened to a broad and aggressive 'risk aversion' as China allowed the USDCNH to rise beyond the closely-watched 7.0000 mark

- Further fast-tracking reciprocal trade war actions, the US Treasury officially labeled China a currency manipulator Monday evening

- Alternative fundamental themes like economic health and monetary policy - as well as their events - will be distorted by the risk impact

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2019? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Trade War Escalations to Start the Week

We knew heading into the weekend that US President Donald Trump's escalation of the trade war against China would not be the end of the headlines. The unexpected Tweet this past Thursday that the White House was placing a 10 percent tariff on the remaining $300 billion in Chinese imports into the country at the beginning of September was a move that almost guaranteed retaliation from the Asian giant as it attempted to balance the painful economic impact it would inevitably absorb from the actions. There were no more US imports to match the US in a like-for-like fashion, so they would need to pursue the even more unorthodox. I expected the country would take the relatively measured next step of selling private US assets or restricting access to rare earth materials - a substantial move, but not one that would exert too much pain on on the United States. Instead Beijing would take the far more aggressive step of allowing USDCNH to appreciate beyond 7.0000.

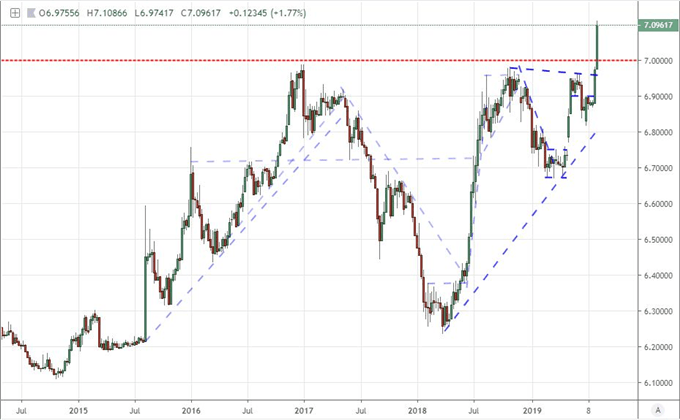

Chart of USDCNH (Daily)

Soon after the Monday morning open, USDCNH made a charge towards the previous-protected cap on the exchange rate and proceeded to surge through the cap in a dramatic 2 percent charge. This is a remarkable move for a number of reasons. First, China has made it a key financial policy to prevent the Yuan's depreciation through the boundary for years (since 2008). Originally, this was most likely a measure to curtail accusations that the country was unduly devaluing its currency for trade advantage - a common accusation by trade partners. However, it eventually adopted an alternative status as the point for which it would be judged that capital flight was overwhelming Chinese authorities' measures for control. Make no mistake, this move is planned; but the lingering concerns over its reflection on China's economic and financial health will remain. This said, I am far more concerned with the fact that this move will inevitably spur the United States to further escalate.

An Inevitable Escalation in Tensions Ahead...and Likely Risk Aversion

With China's decision on its route to retaliate against the White House's escalation, there is an inevitable next step to project. With removing the cap on the Dollar-Yuan exchange rate, China effectively neutralizes much of the United States' efforts to exert economic pain on the country. Adopting the calculation we've seen in USDCNH effectively offsetting the Trump tariffs in previous iterations to our present standoff, the surge in the exchange rate easily offsets the burden intended to force change from the world's largest exporter. Like an effective blocking move in chess, this new measure will naturally elicit a response from the Trump administration that attempts to flank Chinese control. Such routes are inevitably extreme, but recent history shows us that they are not off limits to the President. The first step was Monday evening's headline that the US Treasury had officially labeled China a manipulator - for the first time in over a quarter century, never mind the piratical assessment that an effectively-employed economic cinch would naturally encourage a currency to slide.

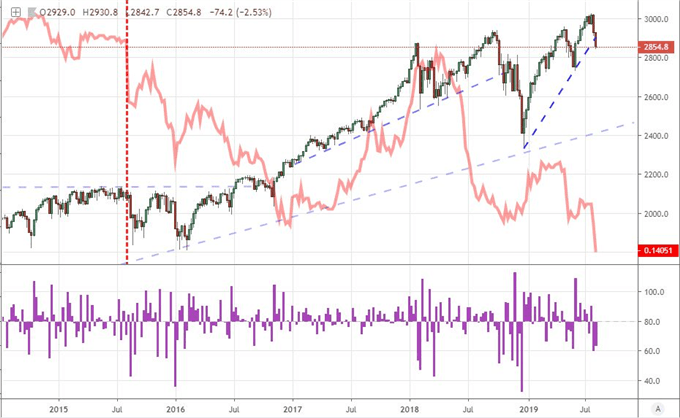

Chart of S&P 500 and CNHUSD with 1-Day Rate of Change (Daily)

Regardless of who is at fault, risk markets have taken note. The US equity indices standing as the most resilient benchmark asset class over the past decade has taken a severe blow with this new fundamental wind. Following the steepest bearish gap on the open in approximately four months, the S&P 500 and Dow suffered the worst single-day loss since the height of selling during the fourth-quarter-2018 tumble. Seeing a seemingly impervious hold-out like these US indices give way is a particularly potent signal that fear is rising. However, I still feel there is no better measure of risk than the breadth assessed by correlation and intensity of global slump in speculative assets. That is exactly what we have seen to start this week with global shares, emerging markets, carry trade and numerous other risk (and safe haven) assets confirm to the traditional alignment. Considering the implications for economic and financial stability, this should come as no surprise. The only shock at this stage is the lack of correction global investors take to reduce or hedge their explicit risk exposure.

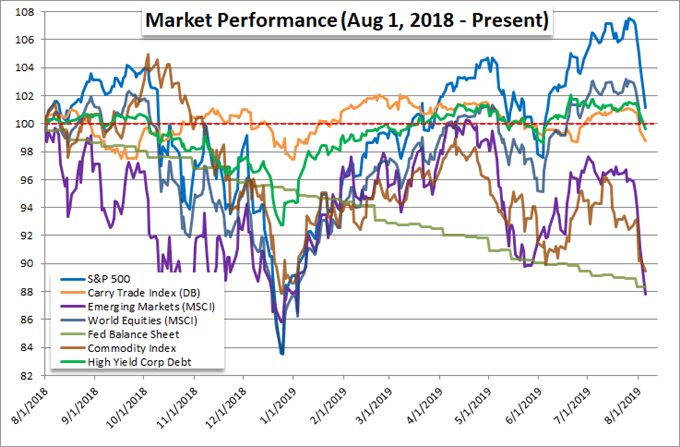

Chart of Relative Performance of ‘Risk Assets’ (Daily)

The Great and Abstract Risk for the Dollar Becomes Tangible

While the risk to global sentiment through the many speculative assets is a systemic interest we should all share, it is perhaps not as fundamentally damaging as the stability threat that we see facing the US Dollar. The Greenback has played much less the traditional safe haven that we have come to expect in previous economic and financial phases. We used to see a natural flight to the liquidity and reliable stability found in the top credit-rated US Treasury - with a natural benefit afforded to the currency used to buy it - when any serious threat arose in the global financial system. That faith has been seriously shaken however - and not even explicitly for the the fact that the sovereign no longer holds 'triple A' status with all three principal credit rating agencies (Standard & Poor's downgraded the US back in 2011). In the current fog of economic war, we find the United States seems to be at the center of most actions and threats to throttle global economic and financial growth.

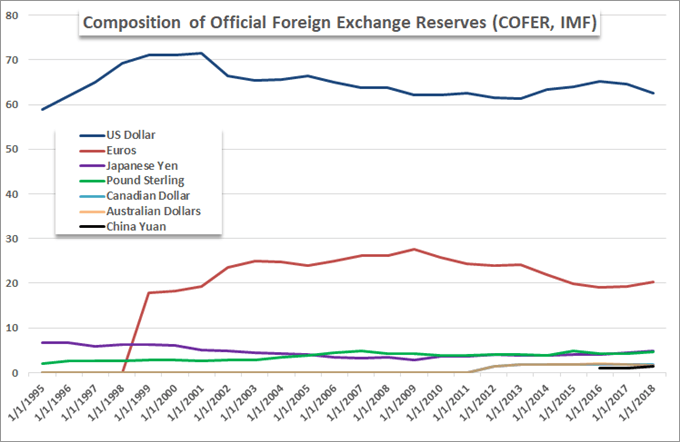

Chart of Global Reserves (Yearly)

It would take an overwhelming effort and amount of time to unseat the Dollar as the chief reserve currency, but that doesn't mean the speculative rank wouldn't migrate away from the benchmark well before that status is lost - speculation tends to front run the official news. There has been an interest from international sources to diversify away from the Greenback and the US financial system since the Great Financial Crisis. A fire that many attribute to US subprime housing - though it was more a result of excessive leverage across the globe and risk spectrum - encouraged those in charge of funds in the private and public sector to start slowly exploring alternatives to a direct tie to US Treasuries and the USD. With circumstances necessitating a quick adjustment, the market has been forced to determine what the best alternative may be in the short-term. The Japanese Yen and Swiss Franc have certain virtues, but liquidity would place the Euro above both - and it is hard to miss the EURUSD's rally this past session. I still believe gold is the most appropriate alternative in a world where aggressive monetary policy is uniformly devaluing the most prominent currencies, so keep an eye on this historical fallback for store of wealth.

Chart of EURUSD with 1-Day Rate of Change (Daily)

Other Key Fundamental Themes and Event Risk Will Receive Be Distorted

As the trade wars continue to progress at a rolling boil, we should expect all other fundamental themes and high level event risk to at least pass through a speculative filter that evaluates circumstances according to this unique systemic risk. One such concern is monetary policy. This past week, before the Trump tweet on an additional $300 billion in Chinese imports coming under tariff, the top event risk was the FOMC rate decision. The US central bank announced a 25 basis point rate cut to its range and the market dove into the details trying to assess their plans for next steps. Chairman Jerome Powell attempted (poorly) to convey a message that this first cut in over a decade was not necessarily the start of a dovish regime and the market was forced to backtrack on some its certainty. Today, we find the market is certain of a September cut and expectations of a 50 bp cut is nearing 40 percent.

Chart of DXY Dollar Index and Implied Yield from December 2019 Fed Fund Futures (Daily)

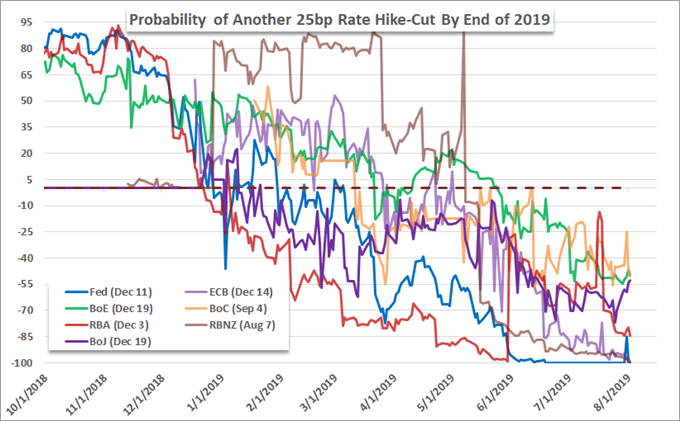

Furthermore, other major central banks around the world, will be forced to account for this 'external risk'. For groups like the European Central Bank (ECB) already staring contemplating more accommodation to account for weakness in local growth, support becomes almost inevitable. This week, however, the headline focus will be on lesser benchmark central banks due to update policy in their regular course. The Reserve Bank of Australia (RBA) was on tap Tuesday with speculation from the end of last week treating the group with a wait-and-see anticipation that was appropriate for steady markets. The Reserve Bank of New Zealand (RBNZ) in the meantime was seen cutting in swaps and only has more reason to act now.

Chart of Probability of Rate Cuts by Major Central Banks

Another big picture theme that we should expected to be swayed by recent developments is the state of global growth. We have recent economic data from monthly manufacturing data to the early release 2Q GDP figures reflect the progression of restriction via trade and natural throttling over the past weeks. The circumstances will only worsen dramatically now under the prospect of an added trade war weight. Through Monday, we saw a few highlights on the service sector activity figures from Italy, the UK and even the US (the Markit's figure); but none of that now will truly encourage as it is seen as 'before the trade war escalation'. There are numerous further economic readings due - ECB bulletin, UK and Japan 2Q GDP, further PMIs - but all of it will find distortion whereby favorable updates will be viewed with skepticism and disappointing outcomes will be treated as confirmation that the situation is already 'out of hand'. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.

What fundamental themes should you follow next week? How will the RBA and RBNZ rate decisions impact their respective currencies? How will they impact the markets at large? Sign up for our webinars to better evaluate how market developments are shaping markets. Sign up on the Webinar Calendar.