Bear Market Talking Points:

- Between strong NFPs and soothing rhetoric from the current and previous Fed Chairs, risk trends helped push SPX above 2,520

- The Dollar's motivations remain complicated and unclear, but the rise in volatility threatens a steadfast, narrow range

- Top event risk next week (US CPI, BOC decision, UK GDP) won't take over from themes like rising liquidity, risk trends, trade war

What are the DailyFX analysts' top trading ideas for 2019 and key lessons to take away from 2018? Sign up for both on the DailyFX Trading Guides page.

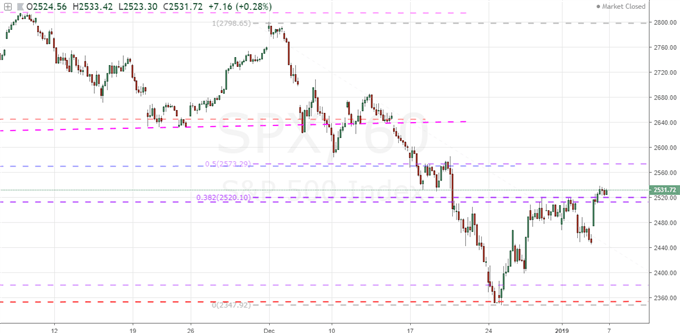

How Much Comfort will the S&P 500's Progress Give to Bulls?

It is hard to believe that we have only closed out the first week of trade for the year - and it wasn't even a full week with standard levels of liquidity. That is because we continue to experience extraordinary volatility. Yet, there seemed to finally be a break in the speculative storm clouds through the close of this past week. A number of the risk-leaning assets that I follow showed some degree of stabilization with a few even posting a noteworthy rebound (like the HYG high-yield fixed income ETF). However, the symbol of speculative health over the past decade is unquestionably US equities - specifically the S&P 500. The SPY ETF (and S&P 500 emini futures for the more savvy leveraged set) has become the rudimentary asset that represents exposure to 'the market'. Its slow conformity to the slide in global equities between February and October helped control global fear and its accelerated tumble between October and December amplified it to destabilizing levels. As such, the rebound the index secured to close this past week can carry more weight than a host of counterparts. The S&P 500 managed to break the range high established over the past three weeks around 2,520 - though it didn't move far beyond the milestone. A technical break is not a self-sustaining event however. Sentiment has been badly shaken recently, and the combination of Fed Chairman Jerome Powell's softer language towards tightening and the short-term impact of the NFPs beat this past Friday do not soundly offset issues like the ongoing trade wars and US government shutdown - not to mention general growth projections. Be mindful of relying on a clear trend in risk because it seems the market is willing to flip at moment's notice.

Chart of the S&P 500 (1 Hour)

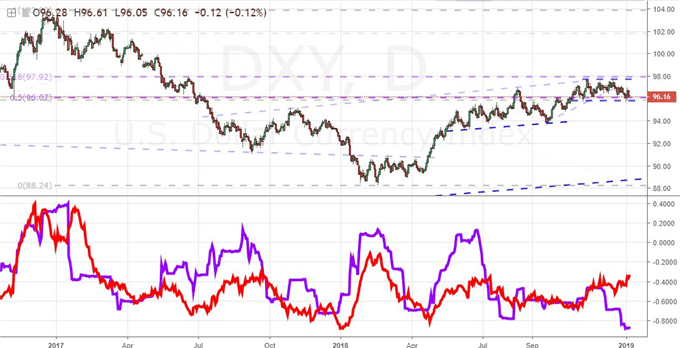

The Complicated Fundamental Backdrop for the Dollar Won't Keep It Landlocked Forever

As volatile and provocative of trends as the US stock benchmarks have been, the US Dollar has refused to entertain any notion that it is on the verge of picking a direction. Instead, it continues to track out a remarkably restrained range. In fact, the range the DXY Dollar Index has established between 97.70 and 95.70 has registered as the smallest 50-day span for the benchmark since the summer of 2014 (a period of historically low volatility). So long as the market remains exceptionally quiet, these boundaries could hold; but that isn't the environment we are facing. Activity is increasing across the financial system and even the FX market is experiencing jolts of sudden volatility as we experienced with the Japanese Yen and few other currencies this past week. As obvious as the Dollar's range is, we have also seen its own activity levels rise. One of the most basic readings of volatility - the ATR - has picked up materially. In fact, the 20-day (equivalent of one trading month) ATR hit its highest level since February in a material divergence to the measure of the market's span. Even if we knew that a break was on the immediate horizon, direction would not be easy to call for the currency. It's commitment as a carry currency or safe haven, a trade war oasis or its epicenter, Fed benefactor or the yield with the most to lose is not clear. Perhaps the market will settle on its principle motivation in the week ahead as liquidity fills out.

Chart of DXY Dollar Index and 20-day ATR and 50-day Historical Range (Daily)

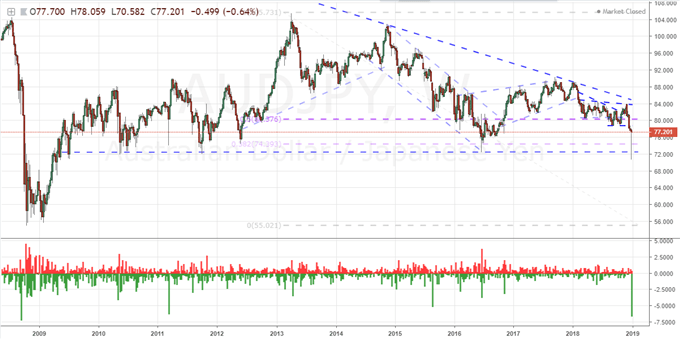

Contrasting the Yen, Aussie Dollar to the Euro, Loonie

For volatility, there are few currencies that can come close to the level of relative intensity experienced by the Japanese Yen and Australian Dollar this past week. While there are certain minor currencies that experience such extreme daily moves on a more frequent basis, the scale of intraday volatility experienced by these two this past week was historically extreme. And, as I often highlight, the masses flock to volatility like moths to a flame - regardless of the intent behind the observation. The volatility these two experienced this past week is not the kind that we can reliably associate to a clear trend. In fact, the fundamental commitment behind them is the furthest from a consistent charge as we have seen from the majors in quite a long time. Both are considered risk-sensitive as a funding currency (Yen) and carry (Aussie). That said, both have proven remarkably obtuse considering the notable movement in underlying sentiment trends this past year. That said, it is more likely that this out-of-the-blue volatility will revert to either the aimless trade we saw before or otherwise a much more restrained level of activity. In contrast, the Euro and Canadian Dollar have not been at the top of the activity tables lately, but their willingness to follow fundamentals when properly motivated is clear and strong. For the Euro, there is still some separation to capable themes after the Italian-EU conflict de-escalated, however a return to regional economic health or monetary policy can readily swoop back in to steal attention. For the Canadian Dollar, the persistent trends the currency has exhibited have not always aligned neatly to the highest profile fundamental headline, but price activity has not strayed from catalyst for long. Both recently signaled their own, tentative technical turn. The Loonie's reversal however is far more remarkable.

Chart of AUDJPY and ‘Tails’ (Weekly)

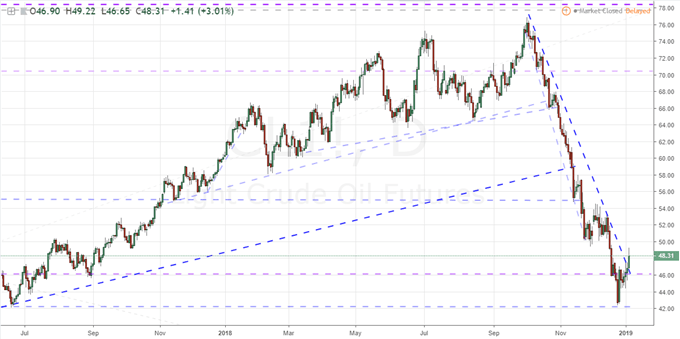

Evaluating Trend for Gold and Crude Oil

Outside of the FX and capital markets, there remains a remarkable degree of activity in commodities. While many goods' futures prices have proven relatively active as of late, the bulk of the focus continues to revert to crude oil and gold. From the US-based WTI energy benchmark, we saw a remarkable technical effort mounted into the close of the past week. With the close above 47.50, we have seen the break of a moderate reversal pattern (inverse head-and-shoulders) as well as the clearance of resistance on an exceptional three-month bear trend channel. This is not a move that has been driven by traditional factors like growth, speculative trends or supply/demand imbalance. Therefore, it is probably not the most reliable guideline for a lasting reversal. Watch speculative positioning instead. As for gold, the climb has come with a quiet appreciation of risk aversion and despite the resilience of the Dollar (the primary pricing instrument). If we look at the metal priced against evenly against its major counterparts, we see even more significant progress than the XAUUSD offers - suggestion the specific version of safety that we have kept this asset in mind for so long. We discuss all of this and more for next week in this weekend Trading Video.

Chart of US-based WTI Crude Oil (Daily)

If you want to download my Manic-Crisis calendar, you can find the updated file here.