Talking Points:

- The Dow and S&P 500 suffered their worst single-day declines since February, the Nasdaq and FAANG moves were far more severe

- Greater amplitude for the retreat in US equities suits its previous outperformance, the real risk would come in contagion

- An IMF warning on financial stability was timely but not a likely catalyst, both Italy and Brexit headlines were overwhelmed

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 4Q 2018? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

US Equities Suffer

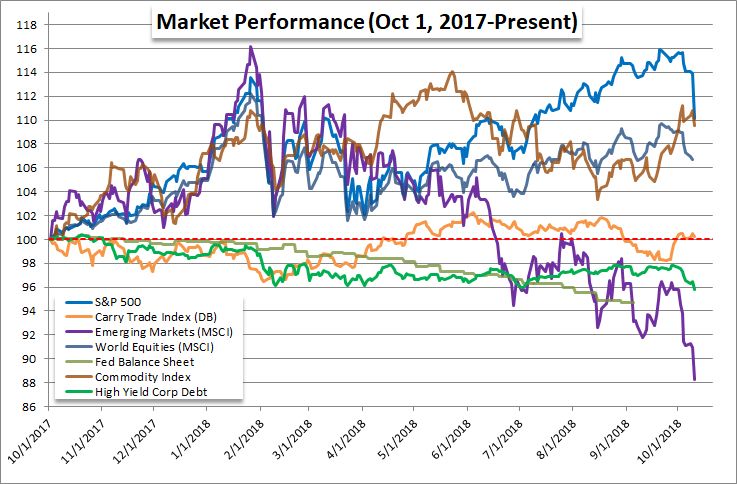

There were a number of meaningful and unrelated fundamental headlines this past session, but all of it was shoved to the side when US equities fell off a cliff through the second half of Wednesday's New York trading session. The selling pressure is not coming completely out of the blue. We have seen the speculative-oriented assets drifting for some time, and even the US indices have come under pressure over the past few weeks. However, the intensity of the decline was certainly something new. The Dow and S&P 500 dropped over 3 percent each - a plunge that ended the latter's 74 consecutive trading day streak without a 1 percent or greater loss in a single session. As severe as these moves were, they paled in comparison to the Nasdaq 100's more-than 4 percent collapse. While the percentages may seem to be splitting hairs, the more 'blue-chip' leaning indices were only registering their worst day since February. For the tech-heavy Nasdaq, the drop was the worst since 2011. The greater intensity highlights the speculative focus of the correction. US equities were the leading asset class over recent months as other markets like emerging markets, junk bonds and carry trade were stagnant or in outright retreat. They had more premium to burn through. Following the concentration one step further, the FAANG group of top market cap tech firms suffered a 6 percent collective drop on the day - the worst showing since I have data on it back to early 2014. The pain was most acute for the markets with the most to lose. The discomfort was there for other assets with a distinct connection to risk-reward, but was significantly less severe and the technical progress less remarkable. This has the capacity of being a scorched earth risk move, but we aren't there just yet.

Market Performance Chart (Oct 1, 2017 – Present)

President Trump Revives His Fed Complaint

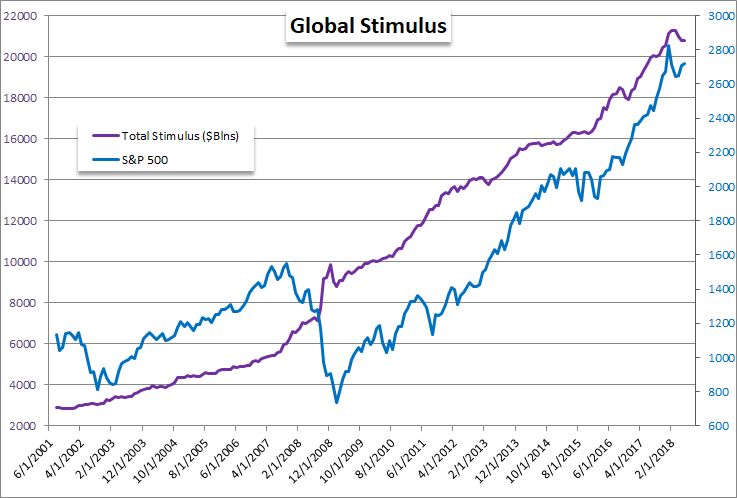

With such an exceptional move from benchmark assets - exacerbated by the return to abject complacency over recent months - it is natural for market participants and leaders to look for an explanation. Personally, I don't think this move develops from a particular spark, but is rather speculative weight coming to bear on a fragile dependency on quiet. From the headlines for the session, there were few data releases that would come close to the breadth or intensity of this move. There were headlines from the IMF (International Monetary Fund) that were of consequence, but their warnings have been met with blank stares so often that it would be a form of 'curve fitting' to place the day's losses at their feet. Following their downgraded growth forecasts Tuesday morning, the supranational group issued a warning over the financial health of global economy. This is not a novel update from Director Lagarde and her group, but it seems more timely with this update. After the dust settled following the New York close, US President Donald Trump reiterated his discontent with the Federal Reserve for their path of monetary policy normalization. This registers as blame being directed to the central bank. On one hand, this group alone is not responsible for the affairs of the past session. Investors have been adding risky assets to their portfolios and utilizing leverage to stretch even further despite an absence of fundamental support. That said, monetary policy withdrawal is likely a contributing factor. Years of zero rates and massive stimulus programs have not only encouraged unrealistic speculative activity, it has almost necessitated it. The rube is that keeping the excess in place would have only pushed the starting point for a tumble higher, not prevented it.

SPX 500 vs. Global Stimulus Chart

Euro's Position in the Risk Spectrum and Pound Focuses on Brexit

With the fireworks through the end of the day, it was clear that the other fundamental updates on the day would get shunted to the background. However, we should keep tabs should the collapse in sentiment not take or as an assessment of what contributing factors will amplify or dampen specific assets' roles in the systemic move. For Dollar, the update on producer inflation bears little weight for rate speculation - as the consumer alternative will similarly struggle with come tomorrow. The Fed's tempo will not be changed by inflation pressures as such economic trends do not change suddenly. However, financial market stability can suddenly alter the course of the Fed. The Greenback has been bolstered over recent years by the rate hikes that it has uniquely enjoyed, so it finds itself in a precarious position as that premium starts to come under pressure. If the Dollar is under pressure, the world's second most liquid currency should pick up the slack, right? The Euro is even more likely to come under pressure should fear increase globally as the troubled relationship between the Italian government and Euro-area leaders on the former's budget plans would be put to the test far more quickly than anticipated. For the Sterling, there is certainly a 'risk' connection but the Brexit is still a more consistent fundamental influence. In an unexpected turn, the EU's chief Brexit negotiator Michel Barnier offered a remarkably specific and optimistic outlook on the negotiations. He suggested a deal could be met as early as next Wednesday. Naturally, the Pound rallied on this news, but we have seen similar enthusiasm fall apart before.

GBP Index Chart (Daily)

The Canadian Dollar Drops Without Aussie and Kiwi, Gold's Appeal Warms

Another remarkable picture through the filter of risk trends is showing up in the 'majors' in the FX market. Historically, there is a separation of safe havens and return/carry currencies. The Dollar, Yen and Swiss franc have long played the role of the havens while the 'commodity currencies' (Australian, New Zealand, Canadian Dollars) were the high return options that were sacrificed when fear settled in. Yet, in a day with such a clear speculative drive, neither an equally-weighted measure of the Aussie or Kiwi Dollars registered a significant loss - certainly not the scale we would associate with carry unwind. That is likely owing to the absence of carry appeal they are presenting with their respective benchmark rates at record lows and the currencies already under significant discount following months of selling. Is this the absolute low? Probably not, but it does speak to the shifting tides and limits to simple labels against genuine speculative positioning. As for the Loonie, there was notable drop. That likely has more to do with the relief rally the currency enjoyed post NAFTA breakthrough. If that was the premium to work off, however, it is likely a limited retreat unless we see an utter speculative collapse. Meanwhile, as we gauge the intensity of sentiment across these various milestones, it is important to keep the most appealing outlets at the extreme of the sentiment spectrum in focus. Gold would only earn a modest bounce this past session but if risk aversion floods traders' subconscious and the limitations of monetary policy coupled with the excess exposure across the market is called into focus, there are few havens better positioned than the precious metal. We discuss all of this and more in today's Trading Video.

XAU/USD Chart (Daily)

If you want to download my Manic-Crisis calendar, you can find the updated file here.

Written by John Kicklighter, Chief Currency Strategist for DailyFX.com