Talking Points:

- Google earnings released Monday evening helped leverage risk appetite, but the enthusiasm didn't hold this past session

- On the trade wars front, President Trump remarked 'tariffs are the greatest' and planned farmer aid suggests no relent

- Top event risk in Wednesday's session is the trade meeting scheduled between Trump and key EU officials

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2018? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

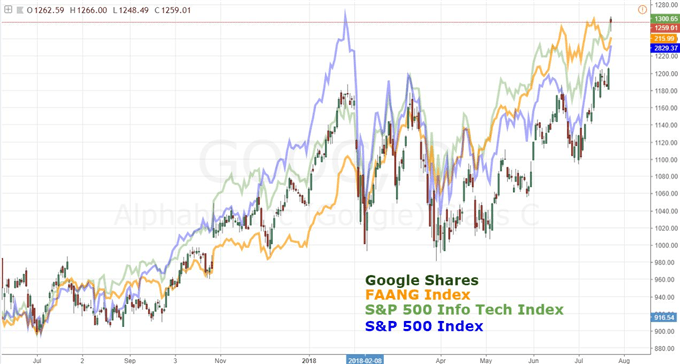

Google Offered Another Temporary Boost to Sentiment

We were offered another speculative litmus test this past session in the form of the Google 2Q earnings release. The tech giant reported robust numbers through the past quarter after the close Monday, and expectations were set. This particular stock is one of the storied 'FANG' or 'FAANG' members. These are the dominant tech firms on a market basis, while the tech sector itself is once again the leading segment of an otherwise exceptional bull phase for US equities. And, as those that join me regularly would recognize, I consider American stock benchmarks the ideal single signal for general risk trends. It isn't that US shares are exceptionally consistent with every rise and fall in general financial market sentiment. Rather, they have proven heavily biased in the over-indulgent speculative reach of the past decade (particularly the past four years) as the most familiar asset in the world's largest market as leverage has built up behind the asset du jour ETFs (such as SPY). This is the chain of speculation that places FAANG members at the 'tip of the spear'. The report certainly seemed to given an initial rise in confidence with Asian markets moderately buoyant and European showing even more pace. When the the ball was back in the US market participants' court, however, the drive stalled. When a market doesn't suffered a sustained drop on bad news (Netflix numbers, trade escalations) it can suggest a 'bullish market'. But when a market also refuses to carry a run on good news (Google, permanent tax cuts), there is anxiety and a lack of conviction.

Trade Wars Aren't Going to Go Away Suddenly

While there were certainly encouraging headlines for traders to digest this past session, there was also decisively worrying updates. Returning the focus back on a future troubled by growing trade wars, US President Donald Trump remarked that 'tariffs are the greatest' when trying to justify the need to push ahead with the trade wars to right perceived imbalances across the global economy. These comments are almost as extraordinary as his previously stated view that 'trade wars are good and easy to win'. Neither of these views are grounded in reason, but remind us that we should not assume this is a situation that will simply vanish into the backdrop so more passive appetites of speculative reach (FOMO, moral hazard) can return to power. It was also reported that the White House was planning short-term support to farmers - to the tune of $12 billion - which would be used to offset the impact the retaliatory tariffs China has put into place. This suggests the US has no plans to remove pressure. Another interesting weigh in on trade wars would come indirectly from the IMF which released its annual External Sector Report which evaluates exchange rates and current account surpluses/deficits. In it, the supranational group added to its assessment that the US stood to lose the most with its pursuit of trade wars by further suggesting the dollar was overbought. On China, the IMF said the yuan was fairly valued given fundamentals - but that was an assessment made up to the evaluation period through June 22.

Attention Turns Back to the More Troubling EU-US Trade Stand Off

Over the past weeks, the focus on the trade wars - itself one of the most open-ended, multi-variate and ominous fundamental threats - had fixed on the standoff between the US and China. And, for good reason. The rapid escalation of threats to the point the Trump warned they could impose tariffs on all Chinese imports poses an exceptional economic risk. However, as remarkable as this relationship is, there is innate buffer in the fact that China is not an open market and economy (which it still holds the 'emerging market' designation). If we were to apply the same scenario to the world's largest developed countries, we would have the makings of a more certain financial crisis and economic recession. With that in mind, we return to the pressure between the United States and European Union. We last left this tenuous relationship with the US President saying they were looking into the possibility of placing a 20 percent tariff on all imported European autos - an extreme move even for such an extreme environment. The EU said it was ready to retaliate with a $300 billion response should the US chose to go down that road. It is this high-risk standoff we expect the President Trump will address with the EU's Juncker and Malmstrom Wednesday. Favorable resolution would perhaps give the Euro and general risk trends some degree of relief, but opportunities to ease tensions have not been seized lately...

Volatility Versus Trend for: Pound, Aussie Dollar, Bitcoin and Commodities

While trade wars, rate decisions (ECB) and big ticket data prints (US GDP) are key milestones for trading this week, we should keep our attention open to other currencies and markets that are not certain headline drivers - if for nothing more than the over-abundance of high profile fundamental themes has led to more indecision than practical opportunity development. For the Pound, there is certainly a fundamental matter of heft - the Brexit - but its progress has been curbed recently. Prime Minister May announced she would take the reins on the negotiations moving forward which adds an interesting dynamic to a convoluted situation. Consider range conditions for this benchmark. From the Aussie Dollar, there isn't an on-going theme to follow, but the 2Q CPI figures will give volatility to a discounted currency. It is also worth noting remarkable developments for the cryptocurrency market as well as commodities given recent pace changes. For the former, Bitcoin has advanced 40 percent in the past month as we start to see one of the first steady speculative advances that falls more clearly from the bubble through the turn of the year. From commodities, a rebound from the Dow Jones Commodity Index is already facing struggle with oil, industrial metals and agricultures bowing to the uncertainties in economic activity. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.