Talking Points:

- Somehow the trade war tenor continues to grow with President Trump threatening tariffs on all of Chinese imports ($500bln)

- Despite the White House's efforts to play down the President's critique of the Fed and Dollar, Trump doubled down Friday

- Top scheduled event risk ahead includes US GDP, FANG earnings, an ECB rate decision, G20 meeting and Australian CPI

What do the DailyFX Analysts expect from the Dollar, Euro, Equities, Oil and more through the 3Q 2018? Download forecasts for these assets and more with technical and fundamental insight from the DailyFX Trading Guides page.

Trade Wars are Growing to a Scale of Inevitable Instability

At any other time in modern financial history, it would seem extraordinarily unlikely that a global financial and economic power would press the world closer and closer to the edge of an economic and financial cliff to achieve an unclear a vague rebalancing. That said, we are presently navigating an unprecedented era for global relations and its influence on citizens and investors. One particular avenue of uncertainty that can no longer be played down as simple bluster is the progress in trade wars. From an uneven application of metals tariffs (though China was immediate) to duties on $50 billion of Chinese goods due to intellectual property theft to last week's threat of $200 billion; US President Donald Trump managed to push the stakes even higher to close out this past week. Ratcheting up the threat by magnitudes rather than percentages, the Trump suggested he was prepared to place import taxes on all Chinese imports (the equivalent of $500 billion). Given the actions to back previous threats, these warnings cannot simply be brushed off. Furthermore, the moves by the United States' trade partners show that there is a definitive effort to circumvent and retaliate against the instigator. We will see what comes of the US-China stand off next week, but we will also check in on other undetonated fronts of this trade war with key EU officials (Juncker and Malmstrom) due to meet President Trump while the Mexican economy minister meets with the US trade representative next week.

President Trump Refuses to Back of the Dollar and Adds USDCNH to the List

The US President's effort to push ahead with a global trade war represent a systemic risk not just for global risk trends, but for the Dollar and US assets in particular. If the engagement were kept to China, the repercussions would 'only' be economic blowback and the possibility of inadvertently touching off a Chinese financial crisis which would readily spill over to the US and the rest of the world. However, the pressure on so many of its key trade allies continues to foster the probability that the world retaliates in concert to have a greater effect - whether to hedge their own risk, dissuade further provocation or simply to penalize. This is no longer an abstract nor distant risk, but a mainstream and fast tracked fear. Yet, just to make sure that the Dollar did not escape this complex threat, Trump's interest in the Fed and currency increase the threat of a wholesale reversal. The President criticized the Fed's hawkish path Thursday saying it made the country uncompetitive owing to the level of the currency and the cost of debt. The White House attempted to sooth concerns that he was targeting the central bank or currency directly, but Trump doubled down Friday to make sure his intention was clear. It wasn't necessary ultimately as the market increasingly takes his warnings at face value. The administrations further turned its attention to the Chinese Yuan Friday evening suggesting it was watching for manipulation. This may just be pretense to delve into currency wars to compliment the trade actions.

Top Scheduled Event Risk to Compete with Systemic Themes

There is little doubt that open-ended and complex themes (like trade wars and the flippancy of risk trends) are the greatest threat/potential for volatility and trend development through the coming week. However, as we await a clear drive from these chaotic fundamental winds, there is high level and scheduled event risk on the docket over the coming week. Top billing for the week ahead is the ECB rate decision. Monetary policy has not proven particularly effective as a general market catalyst in recent months, but this particular groups is at a critical juncture as it decides when to transition from a progressively dovish policy to a tentative hawkish one. The last policy update set the course, but now the watch is on for a definitive commitment. The US 2Q GDP is of considerable importance amid trade wars as we evaluate how the world's largest economy was performing before trade wars began and as they tentatively set in. Expect this data to be evaluated in the context of a more controversial backdrop. Two other events worthy of our attention - but less certain to trigger distinctive volatility - are the FANG earnings and Australian CPI due. Following Netflix's disappointment this past week, we are due Google's, Facebook's and Amazon's updates in order. The Aussie inflation figures will speak to the AUD's lost carry appeal, but can the data return it to its standard role and will carry even matter amid such uncertainties.

If You're Looking for Options Without Overbearing Uncertainty

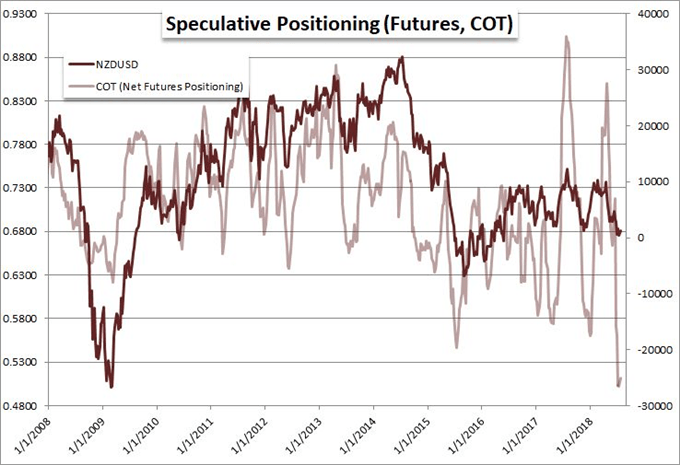

Volatility from the aforementioned dynamic themes and key event risk is probable, but anticipation and consistency for direction is a crap shoot. If you are looking to for better probabilities for market development - even if that comes via more restrained activity levels - there are certain currencies that should be considered. The Canadian Dollar generated some heat through the end of this past week with a strong CPI figure which registered some interesting technical response from USDCAD and NZDCAD. There is little Loonie-specific mines in the week ahead. Though the British pound is being consistently jostled by Brexit, there is little anticipation of a key event for this long-running uncertainty for the UK and the docket is rather clear. If you are looking for a more refined fundamental drive, the Sterling can be a good counterpart to utilize. The Kiwi is in a similar vein, but its speculative bearing is in some ways more extreme than most of its counterparts. Speculative futures positioning in the NZDUSD is rounding up from a record net short which can support yet another trend reversal in the underlying spot rate. We discuss all of this and more in this weekend Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.