Talking Points:

- Heavy speculation long ago priced in the Dollar's yield advantage, which undercut the response to the Fed's hike Wednesday

- Where USD carry gained little traction, the Fed's acceleration adds greater pressure on over-extended risk appetite

- The ECB is facing a policy decision more akin to the Fed's 2014 shift, but it too may connect more readily to risk trends

See how retail traders are positioning in EUR/USD, other key Dollar pairs and global equity indices as monetary policy adds to concern already stoked by trade wars. Find speculative positioning on the DailyFX sentiment page.

A Fed Rate Hike and Upgraded Forecasts Shakes the Wrong Market Pillar

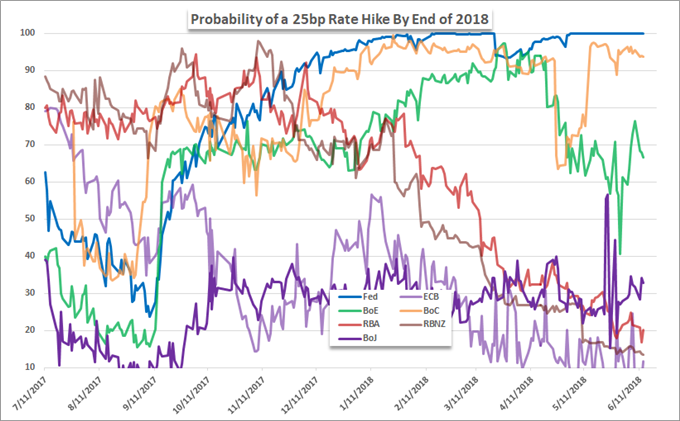

The Federal Reserve triggered a speculative response from the markets this past session, but it wasn't exactly the reaction from the Dollar and risk assets that most had anticipated. And, that is perhaps a sign of where the speculative tide is rising. Accounting for the US central bank's event Wednesday, the top line outcome was a 25 basis point hike to the target range bringing it to 1.75 to 2.00 percent. That was fully expected and thereby fully discounted by the broader market. That said, the greater nuance from the 'quarterly' events didn't disappoint. In the Summary of Economic Projections (SEP), the group modestly improved its forecasts for growth, inflation and employment. The figure that traders were looking at however was the outlook for interest rates. There, the median rate forecast rose by 25 basis points to 2.325 percent - or four full 25 basis point hikes through 2018. That is an unmistakable upgrade from the March assessment of three hikes. Yet, as hawkish as the headlines were from this event, the details offered reason for restraint. Though the forecast is now officially four full rate hikes versus three, the actual change from those members voting was slight - really a technicality or rounding error. What's more, where the Fed is leveraging an advantage for the Dollar, we see the market increasingly unsettled in its pursuit of risk trends and favoring short-term capital gains rather than long-term income.

Why a Fed Upgrade Earned the Dollar Limited Traction but Raises Capital Market Risk

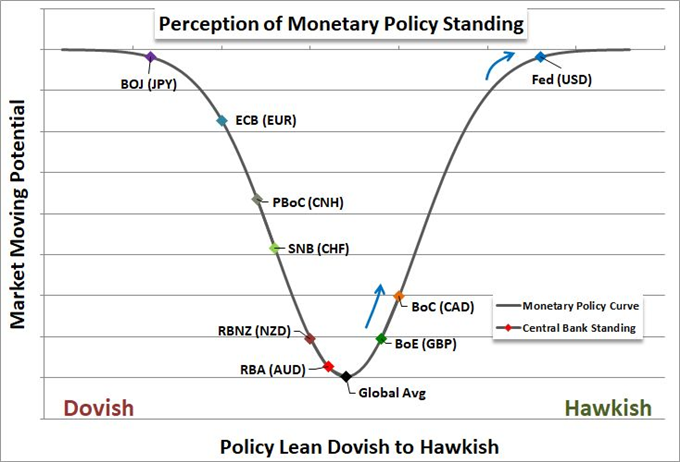

For those that have been trading FX or following interest rates for their investments over the past few years, it is no surprise that the Federal Reserve is the most hawkish major central bank - by a wide margin. The US central bank began tightening its monetary policy (actual rate hikes) back in December 2015 and has more or less maintained a gradual pace of tightening since. This put US policy in distinct contrast to all of its largest peers. In fact, in 2017, the Fed put in for three rate hikes when most of its global counterparts maintained or expanded accommodative monetary policy. And yet, the Greenback steadily lost ground through the year. Why is that? First the markets are forward looking. When the Fed moved to taper, it signaled their intention to start down a path or normalization that would contrast to the ECB, BoJ, BoE and others. This earned the Dollar remarkable gains starting in 2014, well before its first rate hike. This highlights another unique aspect of the market: there was greater appetite for capital gains versus 'income' (dividend, carry, yield, etc). In other words, the market valued the undervalued perspective where the start of rate hikes would start the flow of capital into the US, but there was little actual interest in holding long-term exposure to collect a 1.00 or even 2.00 percent annual carry. Slightly increasing the yield advantage doesn't overcome the serious limitation that yields globally are extremely low such that the risk-reward of long-term buy-and-hold is unprecedented in how unattractive it is. Add to that the implications of tighter monetary policy calling into question how far the markets have reached based on the low volatility and low yield supporting years of speculative stretch, and we undermine the whole reason the Dollar advanced in the first place.

The ECB Decision Is More Tuned to Speculation, A Greater Threat to Risk Trends

Ahead, the top event risk is the European Central Bank rate decision. Of the three major central bank rate decision this week, the ECB's arguably represents the bigger event for its own currency and can leverage a greater sway over speculative trends than the Fed's actual move to tighten. It may seem counterintuitive at first blush that a high probability hold in policy can lead to greater market response than a realized hike; but when we consider the market's penchant for looking ahead and the influence of changing tides for broad risk trends, the potential for the European authority is easier to understand. Through the remarks of key ECB officials over the past few weeks, anticipation for a definitive taper has hit reached levels of virtual certainty across the speculative rank. Of course, this expectation creates the same skew that the Fed faced whereby it is easier to disappoint than impress; but the impact of meeting or exceeding forecasts can more readily translate into market movement. The current situation for the Euro is similar to what the Dollar experienced in 2014. That said, 2017's remarkable rally likely signals the speculative anticipation has already found its way into the currency's pricing. Furthermore, if this well-known dove starts its long climb out of extreme accommodation, it can more definitively shift global monetary policy towards a hawkish bearing and definitively disrupts the monetary policy - speculation connection.

Keeping Tabs on 'Other' Themes

Between the Fed and ECB policy changes, it is easy to have our attention pulled into the influence of developed market monetary policy. However, we should also consider the other high profile events and themes that are set to define our course forward. For themes, trade wars has been conveniently shoved to the backdrop but it remains very much in flux and represents a prominent risk to risk exposure moving forward. As for event risk, the Pound has itself been remarkably active for headline fodder - it just so happens, there are offsetting fundamental winds to keep the Sterling from establishing a clear range. This past session, the run of May inflation data was headlined by a 2.4 percent headline CPI and 2.1 percent core figure which puts little pressure on the BoE to accelerate or abandon its early monetary policy shift. Meanwhile, the crunch votes in Parliament have rendered support for Prime Minister May's government with votes against requirement to stay in the single market and the PM to return to negotiation without a Brexit agreement. This not particularly encouraging for the outlook in the UK, but it does narrow the possible outcomes and thereby reduce 'risk'. We discuss all of this and more in today's Trading Video.

If you want to download my Manic-Crisis calendar, you can find the updated file here.