Talking Points:

- US equity indices extended their drive to fresh record highs despite political scandal, nuclear jawboning and yield curve fears

- The Dollar's effort at a reversal from a 10 day tumble ended after one day, showing consecutive drive reversals aren't good trades

- Top event risk ahead is the closely watched US NFPs, but cross traders should also keep tabs on the Canadian jobs report

Are you watching or trading the upcoming US NFPs release? Join the DailyFX Analysts as they cover the release and analyze the market reaction live. Sign up for the event on the DailyFX Webinar Calendar page.

Risk trends continue to rise with what looks like a sense of purpose. That purpose is not likely a renewed conviction in the outlook for economic potential or greater yields, but rather seems to reflect a need to reinvest capital that was sidelined either for the holiday illiquidity or for tax purposes. The outlook necessarily would be very different depending on what scenario we are dealing with. If there is a renewed sense of confidence and speculative appetite, stretched valuations and new red flags can be overlooked. If this is just an effort to re-establish trades that were temporarily withdrawn, complacency and concern will gain a greater foothold. As we evaluate the sentiment of the masses, there is no doubt that there is at least a robust sense of speculative opportunism for the here and now.

US equity indices continued to pace the capital markets with the S&P 500, Dow Jones Industrial Average and Nasdaq all moving to fresh record highs. Their percentage gains were much less impressive than some other speculative outlets but the level of the markets more than compensates for that shortfall. Global shares are more intense where the gains are showing up (like the DAX and FTSE 100) but they are in the process of recovering from recent stumbles rather than plotting out extensions of already max-out bull trends. Emerging markets keep the lead further out the risk curve, junk bonds are finally recovering and even Yen cross-based carry trades have joined in. Reinvestment is having a strong enough influence that it is at least offsetting a list of general worries that have at one time or another in the recent past put these same markets on the back foot. Renewed political scandals seem to only be growing in the United States, nuclear threats are being lobbed once again between American and North Korean leaders, and even the more arcane yield curve warning has once again made it into the top headlines.

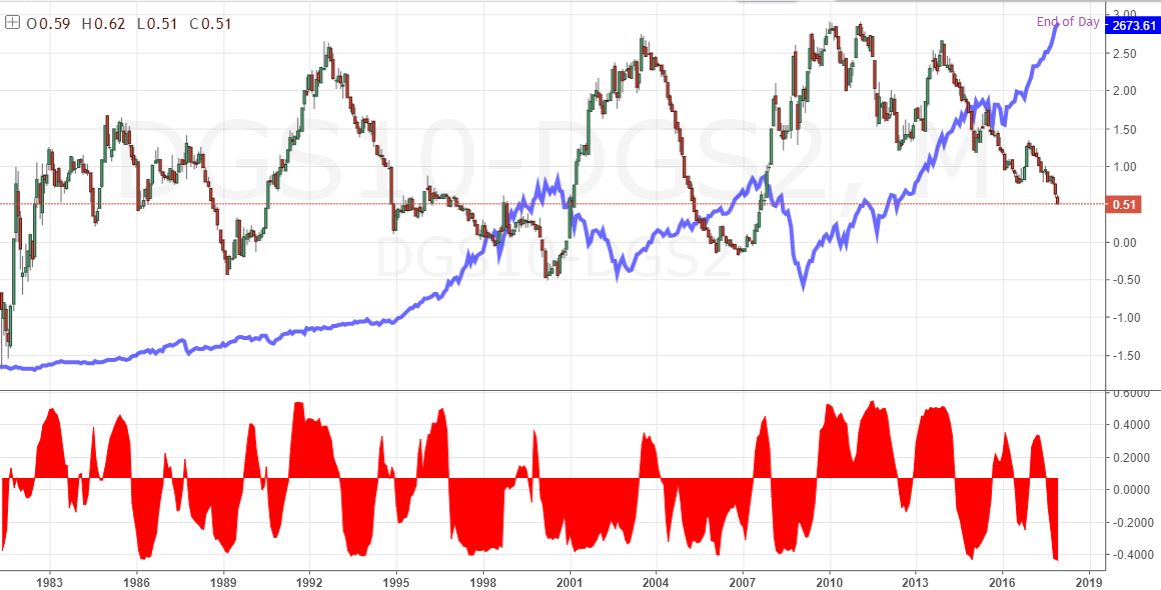

This past session, the Fed's Bullard made mention of the narrowing (US Treasury) yield curvy. He had remarked that the central bank should avoid contributing to its inversion. Historically, an inverted curve - typically of the 2 and 10 year duration - have signaled recessions. Yet, the current narrowing of the popular spread is a little different. Rather than an economically motivated contraction the slide in spread to 0.51 basis points has been primarily driven by the Fed's monetary policy actions. Risk trends may be over-stretched, but this is perhaps not the signal we should monitor for cues on more systemic influences. That said there is good evidence of historical correlation to both the S&P 500 and US Dollar. Whether Fed driven or not, the spread can pose an issue for the US Dollar which maintains a strong positive relationship over time. We will see whether traditional rate forecasts can draw out the markets attention in upcoming final session for the week. The December NFPs are due, and expectations are naturally set high. Yet, while implied rate forecasts through Fed Fund futures have progressed to near decade highs, the Greenback continues to flounder. And, while the US labor report may draw most of the attention, don't forget that the more consistent volatility spark in the Canadian jobs figure is also due for release at the same time. We discuss all of this and more in today's Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE