Talking Points:

- The Dollar's recovery effort was dealt a blow between downgraded wage growth forecasts and the IMF's US growth downgrade

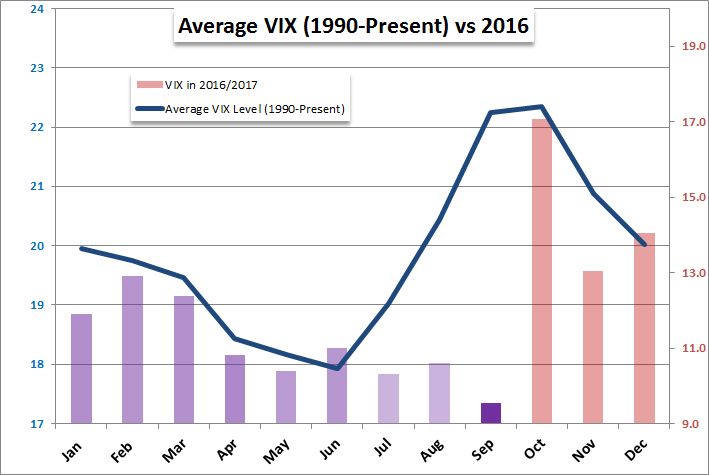

- Risk trends have leveled off from the past two week's surge as SPX levels out around 2,550 and VIX stands above 10

- Euro is best performing major despite Catalonia while the Chinese Yuan's surge seems to defy standard explanation

What are the DailyFX analysts' fundamental and technical forecasts for the Dollar, Euro, equity indexes and more through the fourth and final quarter of the year? Download the recently-released 4Q forecasts on DailyFX.

The Dollar's recovery effort for an otherwise terrible year was dealt a blow this past session. The promising but slow rebound from the Greenback this past month say a technical break on the DXY Index which translated into critical lost momentum for pairs like EUR/USD and USD/JPY. The currency's tumble through this past year has been predicated on a slide in strategic advantage which is difficult to quantify - other central banks closing the ever-widening gap left by the Fed is not exactly a black and white consideration. Yet, this also renders the subsequent Dollar recovery a struggle to sustain. Without some steady reaffirmation of fundamental tailwind, the lack of confidence of the bulls can quickly swamp the recovery effort. This past session, we were met with updates that cracked the delicate facade of the rebound. From the New York Fed's consumer survey, a rise in the three-year CPI forecast (to 2.8 percent) was offset by a sharp decline in expected household income growth (from 2.7 to 2.2 percent). Further, the IMF's generally positive update for the global economy in its semi-annual World Economic Outlook (WEO) actually presented a slight downgrade for the US. Confidence in the tax plan and infrastructure program continue to recede.

While the IMF's update for the world's largest economy wasn't particularly flattering, its projections for the globe was a 0.1 percent point update for both 2017 (3.6 percent) and 2018 (3.7 percent). The group remarked that this is the strongest and most evenly distributed expansion for the world since before the Great Recession. Yet, amid this robust update, we still have a number of points of stress to keep track of. In particular, the reach for return in the financial markets despite relatively low rates of yield has been a point of concern for both this group and investors alike. In fact, credit rating agency Standard & Poor's released a research report Tuesday that said corporate leverage is at a record - and it is reasonable to assume that excessive gearing is true of the speculative rank as well. We will see if the IMF's GFSR (Global Financial Stability Report) reflects on the same in the upcoming session.

Risk trends will be hanging on these updates, but they may disregard as they have so much other bad news over the years. Yet, with the S&P 500 leveling off around 2,550 and the VIX floating above 10, there is certainly room for concern to break down the increasingly stressed sense of optimism. In the meantime, there are some otherwise remarkable performances arising in other corners of the market. For example, the Euro was this past session's best performing major currency despite the persistent uncertainty fueled by the as-yet unresolved Catalonia referendum. Perhaps the ECB's preparation for a normalization of monetary policy can sustainably revive the shared currency - possible, but it would take more than what we have seen thus far. A more extraordinary performance was rendered from the Chinese Yuan. Here the motivations are atypically less likely the result of speculative interest and far more likely the influence of authorities. We discuss all of this and more in today's Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE