Talking Points:

- News the US President offered support to Democrats' call for a 3-month extension on the debt limit offered little USD lift

- The Bank of Canada surprised markets with a back-to-back 25bp rate hike that sent the Canadian Dollar soaring, USD/CAD diving

- Has the ECB effectively deflated the volatility potential in its own meeting today with yet another leak?

See how retail traders are positioning in the FX majors, indices, gold and oil intraday using the DailyFX speculative positioning data on the sentiment page.

The past session delivered more than a few fundamental surprises, but he impact on the market proved uneven. The most high-profile news for the global market was the unexpected news that US President Donald Trump supported Democratic leaders' proposal to raise the debt ceiling and fund the government for three months to alleviate - albeit temporarily - the nerve-racking countdown to financial cliff original set around the end of this month. This is a material improvement in circumstance for speculative appetite as global and domestic political risk has proven particularly troubling for the global financial markets these past months. And yet, there was little in the way of refreshed appetite for risk assets following the news. Perhaps there is doubt over the GOP-led Congress' approval (which would insinuate a delayed climb) or the are too many additional issues at play (such as North Korea) or complacency may finally work as much against building speculative momentum as it does prevent it from faltering. Aside from the broader speculative implications however, the greater surprise in the aftermath of the debt ceiling news is the restrained response from US-based assets.

Looking to the sovereign debt market, there was a sharp response to the headline for President Trump's support from short-duration bonds (particular one month). These assets were the most directly at-risk, so this comes as little surprise. That said, further out the curve, the impact proved far less material. Beyond local capital markets floundering after the news, the US Dollar offered little-to-no response to the improved conditions. There is a deep reassurance afforded to the Greenback with the alleviation of the impending debt clock. While the Dollar no doubt found much of its 2017 tumble on the basis of its diminished monetary policy status, the more recent losses for the currency find considerable justification in the localized risk derived from the country's debt cliff. While it may seem the US currency enjoys permanent status as the primary reserve for the world, that is a station that is absolutely fluid and in real peril should the country technically default or even if the persistence of financial brinkmanship were to undermine global confidence. In the meantime, another major theme was in this past session - and will be so again through the next session: monetary policy. The Bank of Canada's (BoC) second rate hike upset the consensus and evoked a sharp rally for the Canadian Dollar. The real question however is the motivation for follow through.

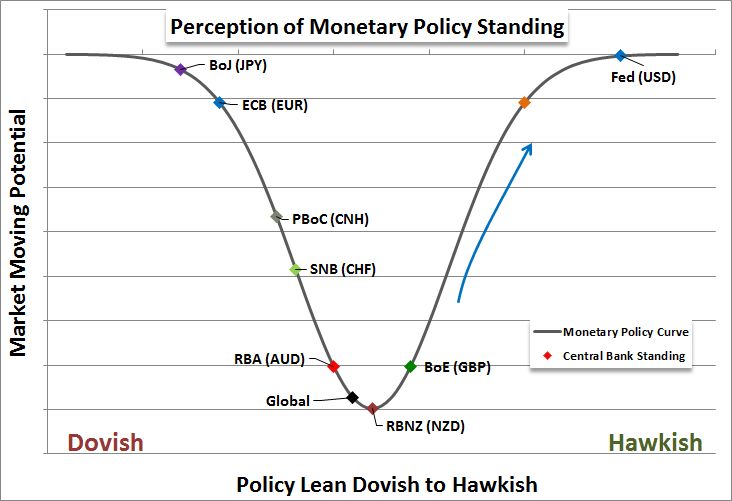

If we use overnight swaps to establish speculative preparation, 56 percent of the market was surprised when the BoC announced it would follow July's hike with another 25 basis points of tightening that brings Canada's benchmark rate up to 1.00 percent. This caught a lot of bears wrong footed, but it more broadly changed the monetary policy standings of the world's largest central banks. While I would label the Fed modestly more hawkish than the BoC, it is arguably more hawkish than the Reserve Bank of Australia and Reserve Bank of New Zealand. While both the Aussie and Kiwi Dollar support higher current rates (1.50 and 1.75 percent respectively), the real drive is in change rather than current rates. A 1.50 percent yield per annum is hardly something to bend over backward for. The Canadian Dollar can certainly extend its rally, but that will either necessitate speculation of further tightening or a strong groundswell of speculative appetite for competitive return. The former is the foundation of the Euro's charge through 2017, and that brings the ECB decision into focus. It seemed the European Central Bank attempted yet again to use an unofficial channel to issue a warning without putting their credibility on the line - they let leak last week that more officials at the bank were concerned about the level of the currency. A day before the decision, Bloomberg reported that unnamed sources with familiarity on the situation believed a decision on the QE reduction plan until at least the October meeting. The Euro initial slipped but EUR/USD and other major crosses would not cave under the way. We'll see if the market shows surprise and speculative retrenchment despite this advanced warning with the upcoming policy meet. We discuss all of this and more (including cryptocurrencies, the Dollar's policy bearings, crude, gold, etc) in today's Trading Video.

To receive John’s analysis directly via email, please SIGN UP HERE.