Will Dollar weakness persist for the rest of 2017? Get a free DFX Q2 market forecast here

Talking Points:

- DXY Technical Strategy: DXY remains in a “sell the rips” mode

- Correlation to US Treasury yields have kept DXY under pressure and may continue

- EUR strength expected to continue per sentiment making DXY gains tough to come by

Relief has been short lived for most greenback bulls, who likely miss the collective wisdom that the dollar trade ever higher that was shared at the close of 2016. On Wednesday, traders got a bit of relief when reports came out that the ECB may drop their inflation forecast through 2019. However, a broader look could see Wednesday’s 0.25% pullback in EUR/USD as an opportunity and potential predecessor to a move above the November 9 resistance level of 1.13 and onto weekly closing resistance from late-2015 and 2016 near 1.1475/1550.

It would make sense for ECB to lower their forecast of inflation as evidenced by the global fall in sovereign bond yields. When inflation is forecasted and a credible threat, you don’t want fixed payments (like sovereign bonds provide,) instead, you want a market-linked floating rate to be received while paying a fixed rate that would ideally be below the market rate that you’re receiving.

When looking at sovereign debt, a clear trend has developed that has pressured the USD and could continue to do so. Recent reports and US Treasury data shows that China is ready to start buying Treasuries again (which would bring yields lower) now that the threat of unacceptable Yuan volatility has passed. Additionally, looking at helpful inflation measures like the US 10Yr Breakeven (the bond market’s inflation expectations) and the US 2yr-10yr spread, which marks a swap trade when a trader sells 2Yr Notes and Buys 10Yr notes, a common trend of lower inflation is expected as both measures sit at 6-month lows.

While you could argue this is bearish for the EUR, I would argue that a lot more optimism is baked into the USD due to recent Fed rhetoric. Put another way, the Fed would have to unwind their hawkish sentiment more aggressively than the ECB, whom could still lift their economic predictions, and that could lead to further DXY weakness. One market I have focused on acutely in the DailyFX Closing Bell webinar is the Eurodollar futures rate. Eurodollar Futures is a futures rate based on expectations of USD deposit rates in off-shore/ non-domestic accounts. Given that the global economy relies on the USD for ~40% of transactions as USD is the global reserve currency, this is a helpful way to see expectations from some pretty smart people down the road. As of June 7, 2017, there is a disagreement between the bond market and the Fed about where the rate will likely be when the Fed reaches their terminal rate or the level at which they will stop hiking rates within this hiking cycle by ~110bps. Even if the bond market is half-wrong, that could mean the Fed will need to back step their recent hawkish rhetoric that could see the greenback fall further still.

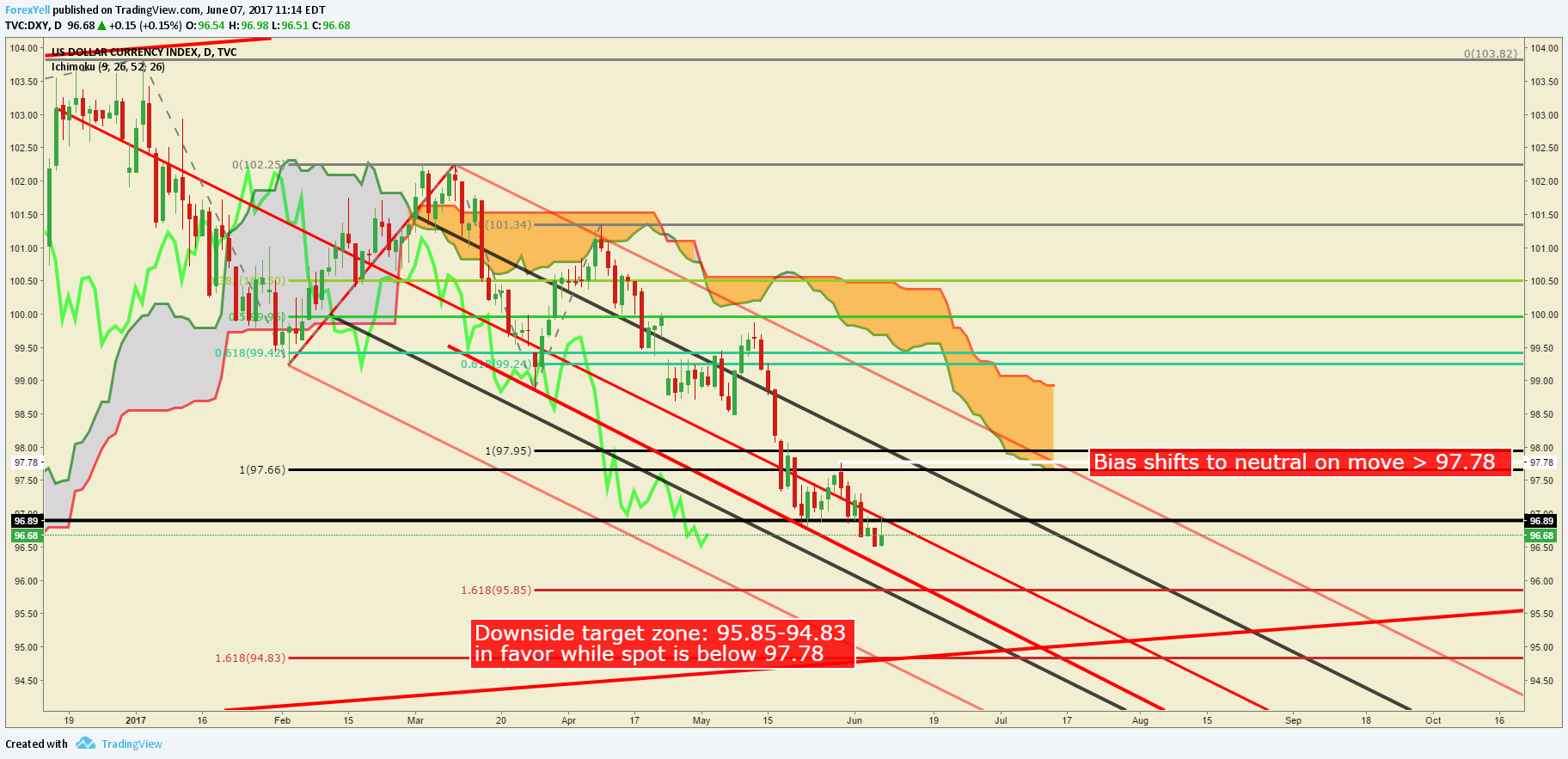

Looking at the chart, the clear level (to me) worth watching that would stop the bleeding would be an intraday move above 97.78. Given the expected volatility on Thursday, we could see an unwind of current market positioning that allows USD to get that lift. However, if the trends remain unperturbed, the Dollar decline could continue. Should the market remain below 97.78, I will keep targeting a zone between two 161.8% Fibonacci extensions between 95.85-94.83. Should price move above 97.78, I will need to close out some positions to take money of the table and recalibrate to see what the new weakest currency has become. For now, though, it’s safe to say on a relative basis, it’s the USD.

If you would be interested in seeing how retail traders’ are betting in key markets, see IG Client Sentiment here !

Join Tyler in his Daily Closing Bell webinars at 3 pm ET to discuss this market.

DXY trading below 97.78 keeps focus on downside extension targets

Chart Created by Tyler Yell, CMT

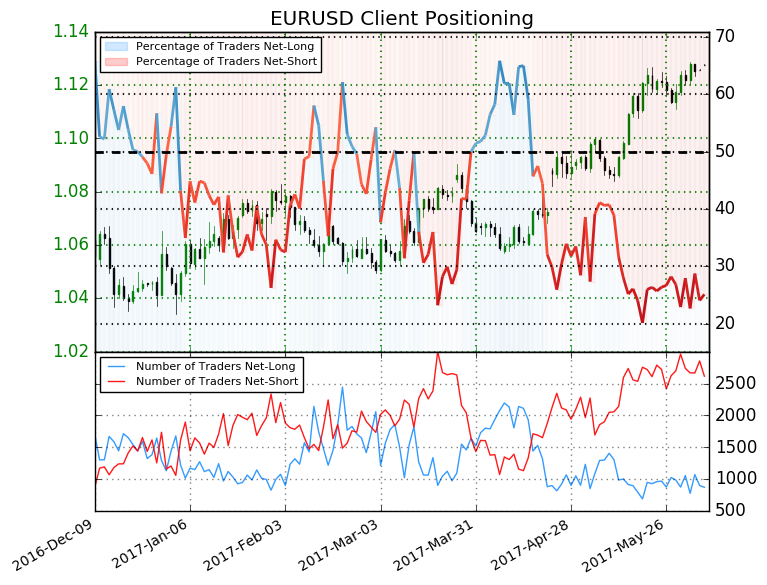

IG Client Sentiment Highlight: EUR (57.6% of DXY) Sentiment Favoring Further Upside

EURUSD: As of June 07, Retail trader data shows 25.1% of traders are net-long with the ratio of traders short to long at 2.98 to 1. In fact, traders have remained net-short since Apr 18 when EURUSD traded near 1.06045; theprice has moved 6.1% higher since then. The number of traders net-long is 27.3% lower than yesterday and 21.1% lower from last week, while the number of traders net-short is 3.2% lower than yesterday and 5.9% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests EURUSD prices may continue to rise. Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger EURUSD-bullish contrarian trading bias. (Emphasis mine)

---

Shorter-Term DXY Technical Levels: Wednesday, June 07, 2017

For those interested in shorter-term levels of focus than the ones above, these levels signal important potential pivot levels over the next 48-hours.

Written by Tyler Yell, CMT, Currency Analyst & Trading Instructor for DailyFX.com

To receive Tyler's analysis directly via email, please SIGN UP HERE

Contact and discuss markets with Tyler on Twitter: @ForexYell