U.S. Inflation Talking Points:

- This morning brought the release of CPI for the month of December.

- While starting last year in a rather tame manner, inflation climbed throughout 2021 to the point that it became a large issue for the FOMC.

- This morning’s inflation print was expected to come in at 7% with core inflation expected at 5.4%.

- The data released with headline inflation printing right at the 7% target and core posing a slight beat at 5.5% v/s 5.4% expected.

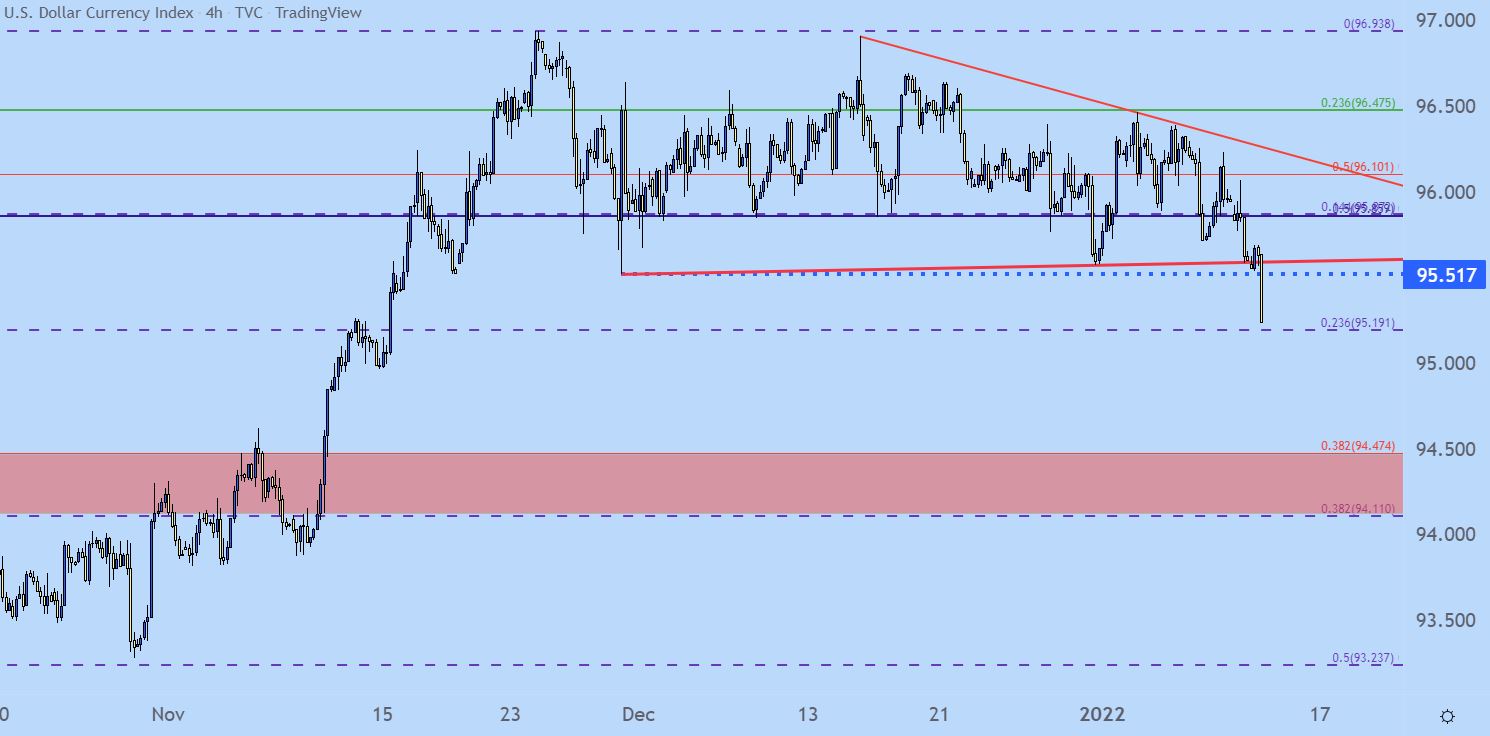

- The immediate result was US Dollar weakness as the currency broke-below a big spot of support.

This morning brought the release of U.S. CPI for the month of December and this print came out amidst an intense focus on inflation.

After coming into 2021 at 1.4%, inflation continued to climb throughout 2021 to the point that it became problematic for the Federal Reserve’s loose money policy. As we open the door into 2022, inflation remains elevated and the Fed is now at the point in which they appear ready to begin tightening policy. The big question now is when does it start and by how much?

This morning’s CPI print came in at an annualized read of 7%, right in-line with expectations; and core CPI printed at 5.5% v/s a 5.4% expectation.

US Dollar Breaches Support

Despite the massive inflation print, the US Dollar has fallen below support and now trades at fresh monthly lows with fresh two-month-lows now very nearby. This is likely because markets had become accustomed to strong beats on the headline figure and it seemed as though many were braced for a repeat again this morning. But, with headline inflation printing ‘only’ at 7%, it seems that markets may catch a temporary reprieve, somewhat driven by the fact that at least some of the inflation that’s being seen is partially transitory.

US Dollar Daily Price Chart

Chart prepared by James Stanley; USD, DXY on Tradingview

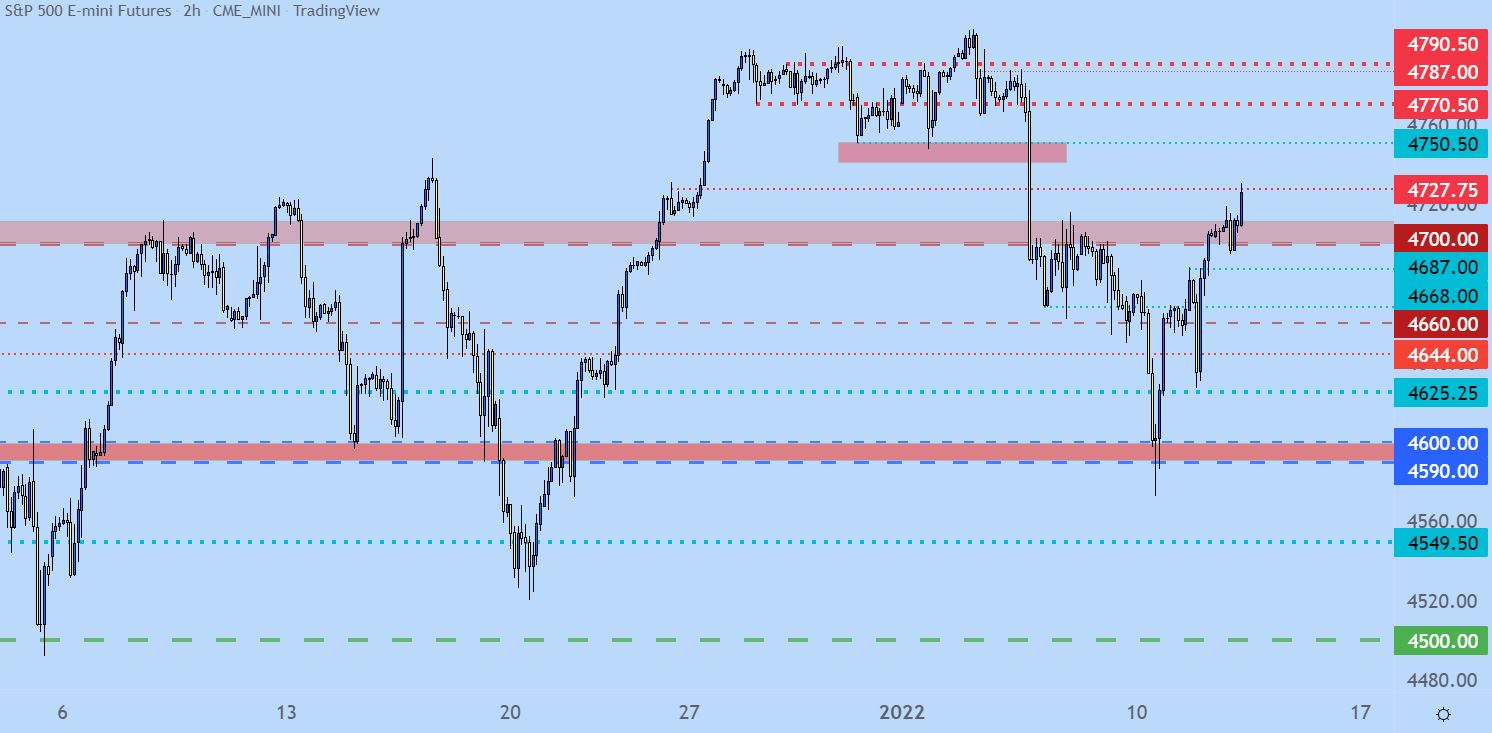

Stocks Jump

Another knock-on effect of inflation printing in-line with expectations has been a reprieve move in stocks. As markets began to gear up for more and more possible rate hikes, equities were on their back foot with a degree of vulnerability.

But, after Powell’s comments yesterday which came out fairly dovish, at least in my opinion, combined with this morning’s CPI release, equity markets have new rationale for backing the bid.

S&P 500 futures are jumping ahead of the open and there’s the appearance of an inverse head and shoulders pattern here, which can keep the door open for bullish breakout scenarios.

S&P 500 Two-Hour Price Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

--- Written by James Stanley, Senior Strategist for DailyFX.com

Contact and follow James on Twitter: @JStanleyFX