Nasdaq 100, Hang Seng, ASX 200 INDEX OUTLOOK:

- Dow Jones, S&P 500 and Nasdaq 100 closed -0.07%, -0.36%, and -1.07% respectively

- The US Dollar rebounded, reflecting rising fears about Fed tapering bond purchases

- President Joe Biden signed an executive order to banUS entities from investing in an expanded list of Chinese companies, weighing on the Hang Seng Index (HSI)

ADP, US Dollar, US-China Tension, Nonfarm, Asia-Pacific at Open:

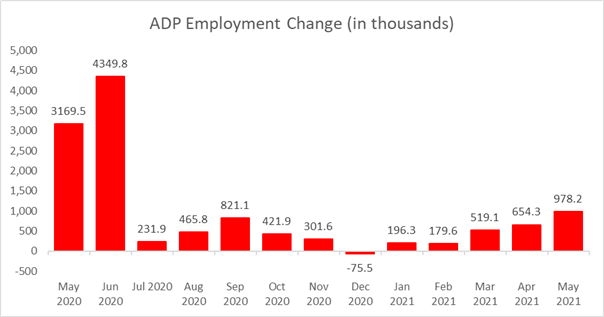

Wall Street stocks retreated on Thursday, dragged by the technology sector as fears about Fed tapering bond purchases geared up after a robust ADP private payrolls report. The private sector added 978k jobs in May, hitting an eleven-month high and also smashing the baseline forecast of a 650k increase (chart below). The pace of job creating appears to have accelerated over the past three months, underscoring a strong economic recovery. Meanwhile, weekly jobless claims fell to a fresh pandemic low of 385k, versus a 390k forecast.

The robust data hinted that tonight’s nonfarm payrolls data may deliver positive surprises, strengthening the prospect of Fed tapering. This came a day after Philadelphia Fed President Patrick Harker said it is appropriate “to slowly, carefully move back” on bond purchases at an appropriate time.

The market is indeed concerned about it. The DXY US Dollar index rebounded 0.65% to 90.49 overnight, and 10-year Treasury yields climbed to 1.625%. A stronger US Dollar sank gold prices and may weigh on commodities in general. Crude oil prices paused a rally and retreated from a two-and-half year high.

US ADP Employment Change – May 2021

Source: Bloomberg, DailyFX

Risk appetite tilted towards the cautious side for equities, with defensive sectors outperforming cyclical ones overnight. The risk-off sentiment could carry into the Asia-Pacific trading today, especially for the Greater China region. Futures in Japan, mainland China, Hong Kong, Taiwan, Singapore, Malaysia and India are in the red, whereas those in Australia and South Korea are in the green.

President Joe Biden signed an executive order on Thursday that bans US entities from investing in a widened list of 59 Chinese companies with alleged ties to defense or surveillance technology sectors. This move risks reigniting US-China tension, and may spook panic selling in those exposed companies.

As a result, Hong Kong’s Hang Seng Index (HSI) retreated 1.13% on Thursday. Selling looks set to carry on into the weekend, especially among the defense and surveillance technology sectors.

Looking ahead, traders will keep a close eye on Friday’s nonfarm payrolls data for clues about job market development and its ramifications for the Fed’s policy outlook. The figure is expected to come in at 650k, a big jump from previous month’s reading of 266k. Concerns about tapering renders the market vulnerable to heightened volatility if actual numbers deviate too far from baseline forecasts. Find out more from the DailyFX calendar.

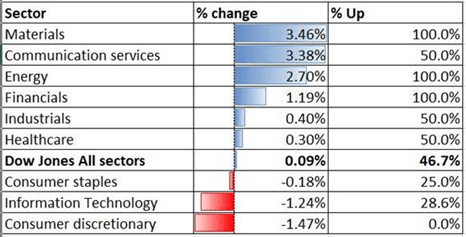

Looking back to Thursday’s close, 6 out of 11 S&P 500 sectors ended lower, with 52.1% of the index’s constituents closing in the red. Defensive-oriented utilities (+0.52%), consumer staples (+0.51%) and healthcare (+0.39%) outperformed, whereas consumer discretionary (-1.22%) and information technology (- 0.91%) were trailing.

S&P 500 Index Sector Performance 06-04-2021

Source: Bloomberg, DailyFX

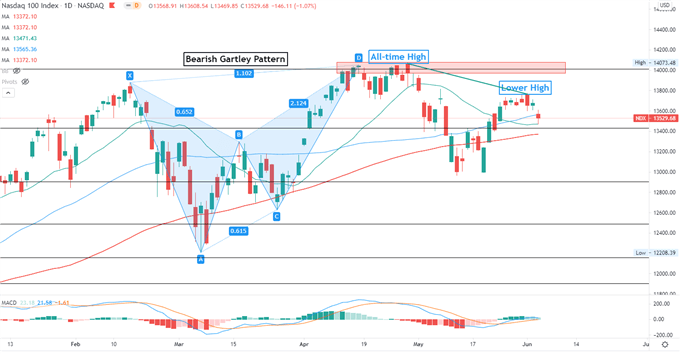

Nasdaq 100 Index Technical Analysis

The Nasdaq 100 index reversed lower this week, forming a “lower high” on the daily chart. This suggests that near-term trend may be reversing and further consolidation is likely. An immediate support level can be found at 13,430 (the 161.8% extension), while a key resistance remains to be 14,000 (200% Fibonacci extension). The MACD indicator is about to form a bearish crossover, suggesting that upward momentum is fading.

Nasdaq 100 Index – Daily Chart

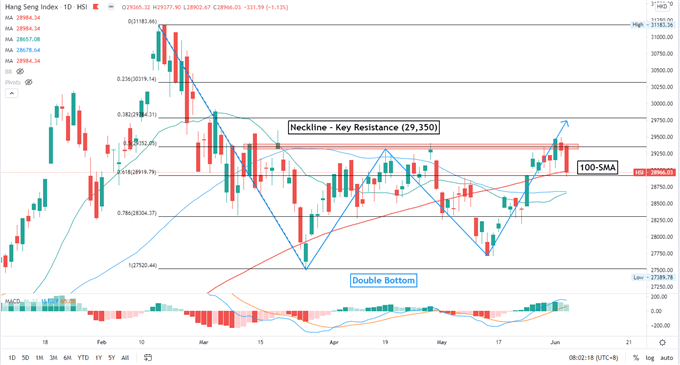

Hang Seng Index Technical Analysis:

The Hang Seng Index (HSI) failed to breach the “neckline” of the “Double Bottom” chart pattern formed since early March and retreated to the 100-day SMA line looking for near-term support. An immediate resistance level remains to be 29,350 – the 50% Fibonacci retracement. Breaching below a near-term support of 28,920 may open the door for further losses with an eye on 28,300 – the 78.6% Fibonacci retracement.

Hang Seng Index – Daily Chart

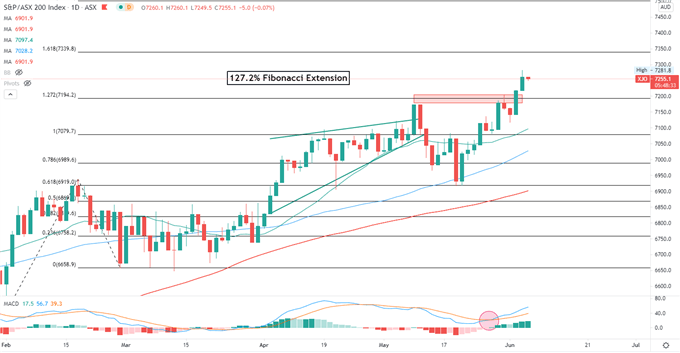

ASX 200 Index Technical Analysis:

The ASX 200 index hit an all-time high of 7,260 and breached above the 127.2% Fibonacci extension level. Recent surge in prices pulled the RSI oscillator close to the overbought territory, rendering it vulnerable to a technical pullback. The MACD indicator formed a bullish crossover and trended higher, suggesting that bullish momentum may be dominating.

ASX 200 Index – Daily Chart

--- Written by Margaret Yang, Strategist for DailyFX.com

To contact Margaret, use the Comments section below or @margaretyjy on Twitter