Italy Talking Points:

- Italy’s politicians continue to keep markets on edge as their budget indiscipline intensifies and talks about further debt issuance are re-ignited.

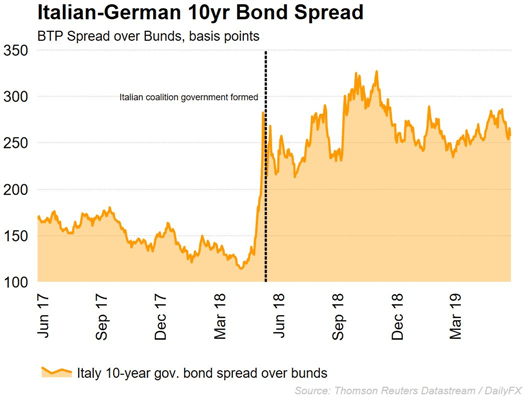

- Italian 10-year bond spreads continue to increase against the German Bund - financing will become more expensive as risk premiums increase.

- EUR could suffer further losses against major currencies as mini-BOT talks develop further.

Markets have remained cautious of Italy for most of the last year as the third largest economy in the monetary union has been running a large public deficit which has brought on conflict with the bloc’s leaders. In recent weeks, EU lawmakers have been edging closer to imposing sanctions on Italy over the State’s handling of public debt, and re-ignited talks about the Italian government issuing more debt to settle their current debt has meant that the Euro continues to remain sensitive to political developments in Italy.

Despite talk about mini-BOTs being around for some time, the victory of Matteo Salvini’s right-wing League party in the European Elections has captured the attention of the markets, as the League and the Five Star movement, which have led the country in a coalition for the last year, hint at the return of the Italian Lira during their national election campaign last year. The Euro suffered sold-off during the last quarter of 2018 as lawmakers in Italy said that most of Italy’s problems would be resolved if it regained monetary independency by re-introducing a national currency.

And recent developments in Italy’s Parliament have the Eurozone on edge, as a motion has been passed for the Italian Government to review how it pays its commercial debts, re-igniting concerns about the Premier’s intentions. Although issuing a parallel currency is illegal under EU laws, questions arise as to whether issuing mini-BOTs could be the tool Eurosceptics may use to facilitate Italy’s departure from the Eurozone.

What Exactly are Mini-BOTs?

The idea is that the Italian Government would issue short-term, interest-free, small-sized government securities to be used as an internal currency to pay for the government’s suppliers, taxes and social contributions. It would essentially be paying for its obligations through newly issued debt which could act as a debt multiplier, but the belief is that it would allow companies to receive their overdue arrears which would increase liquidity and boost the economy.

But, if these government securities were then enabled to change hands as a medium of exchange, creditors could see a reduction in their income as the settlement of payments in a fiscal currency other than the legal tender would have less value if exchanged between parties other than the State. A way for the Government to safeguard the value of the securities would be to accept them as a future tax payment, effectively acting as a fiscal stimulus and reducing tax revenues. Because of their nature, in paper form and small denominations, they would be expected to be spent locally, which would stimulate growth in the Italian economy with the expectation of an increase in short-term tax revenues to offset future tax losses. This would mean that Italy could achieve fiscal expansion without relying on the Euro.

Are Mini-Bots Illegal?

The issuance of mini-BOTs would not break any EU laws if they are simply issued as a security, but their use as a parallel currency would be inconsistent with the EU’s current legal framework. However, considering that Italy’s dispute with the EU over its budget indiscipline continues, the issuance of more public debt could make the EU question whether Italy’s policymakers are taking matters seriously. Issuing mini-BOTs would see risk premiums continue to increase, widening even further the gap between Italian debt and the benchmark German Bund.

Despite the likelihood of mini-BOTs materialising being low, the fact that they have captured EU lawmakers’ attention means that they are considered to be a threat to the stability of the Eurozone. Specifics about the securities have not yet been released but influential European figures have been quick to reject the idea that they would be welcomed by the ECB. As mentioned by Mario Draghi “They are either money – and then they’re illegal – or they’re debt, and then that stock goes up. I don’t see a third possibility”

But even more important than the specific characteristics of mini-BOTs would be the message that they send about “Italeave” if they are issued. Given remarks made by Italy’s politicians about the parallel currency, it may be that they would be used as the first step towards Italy’s departure from the Eurozone.

Regardless of whether mini-BOTs are illegal or not, their success as a means of exchange depends greatly on whether they are widely accepted by the marketplace. EU officials believe that if they were introduced they would not be accepted because of fears that Italy could leave the Eurozone which would lead to them trading at a discount to the Euro. And despite having the potential to increase purchasing power within the Italian economy, if sellers do not accept them as legal tender then their adoption and intended stimulus power is limited.

Past Evidence is Mixed

Most economists remain very wary about governments issuing parallel currencies as previous occasions where IOUs have been issued have not yielded the expected results. In 2002 the Argentinian government issued parallel currencies to overcome the limits on printing pesos, that were pegged to the US Dollar at that time. The peso was overvalued, and the introduction of alternative currencies was intended to devalue against the peso and stimulate growth in the economy. But the strong demand for the parallel currencies to overcome the shortage of pesos meant that the desired effect was not achieved, and the currencies were abandoned a short time later.

In 2009 the state of California suffered a revenue shortage which led to increased fiscal budgets and the issuance of interest-paying IOUs to pay short-term obligations. But the adoption of the IOUs as a means of exchange was limited because they were not widely accepted by merchants, which diminished their stimulus effect and were later bought back by the Government at par. Their lack of acceptance showed that a legal tender is deemed worthless if there is no trust in the creditworthiness of the issuing party. But, despite their lack of general adoption, the Californian Government managed to increase their revenues and pay back its fiscal obligations, which proved that although not permanent, IOUs can be used as means to overcome temporary difficulties.

How Will the Euro React?

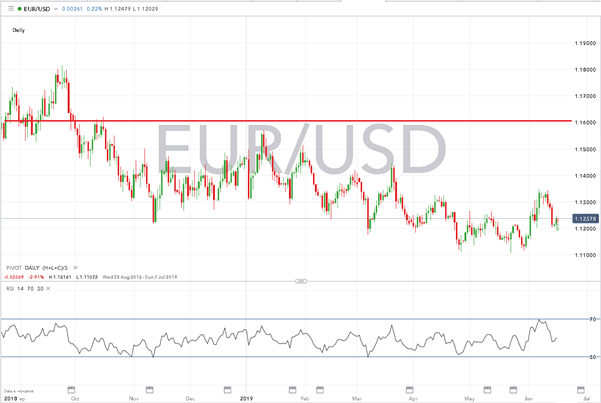

Judging by how the Euro has reacted to previous speculative mentions of mini-BOTs, we could see the Euro lose value against most major currencies as developments unfold. Back in October 2018 the single currency experienced increased sell-side pressure as Rome and the EU’s budget clashes intensified and Italian politicians re-introduced talks about min-BOTs. The Eurodollar fell below the 1.1600 handle, a level which it has not managed to overcome ever since.

EURUSD PRICE CHART DAILY TIME-FRAME (SEPT 2018 – JUNE 2019)

Even if mini-BOTs have no future in the Eurozone, traders will continue to focus on Italy as its budgetary indiscipline continues to unfold. It has emerged that the EU is planning to launch an Excessive Deficit Procedure (EDP) against Italy which could result in a fine of up to EUR 3.4 billion, the equivalent of 0.2% of the country’s GDP.

All in all, considering that populist sentiments are flourishing in Europe and secessionism is becoming an increased topic of discussion it is no wonder that the EU is feeling anxious about Italy’s rebellion. After all, we’re in the middle of Brexit and are staring down the barrel at a possible “Italeave”, the ECB must be wondering: WHO’S NEXT?

Recommended Reading

Eurozone Debt Crisis: How to Trade Future Disasters – Martin Essex, MSTA, Analyst and Editor

KEY TRADING RESOURCES:

- Just getting started? See our beginners’ guide for FX traders

- Having trouble with your strategy? Here’s the #1 mistake that traders make

- See our Q3 forecasts to learn what will drive FX the through the quarter.

--- Written by Daniela Sabin Hathorn, Junior Analyst

To contact Daniela, email her at Daniela.Sabin@ig.com

Follow Daniela on Twitter @HathornSabin