Fundamental Forecast for the US Dollar: Neutral

- Interest rate differentials have narrowed among the major currencies, undercutting a key source of US Dollar strength in recent months.

- Incoming US economic data won’t do any favors for the ‘US recession’ calls, but key US labor market figures will likely remain strong.

- According to the IG Client Sentiment Index, the US Dollar has a bearish bias heading into the first week of June.

US Dollar Week in Review

The US Dollar (via the DXY Index) fell for the second consecutive week, dropping by -1.35%, as Fed rate hike odds continued to pullback. Coupled with chatter from other major central banks that faster rate hike cycles will emerge elsewhere, and a rebound in risk appetite, the US Dollar has some seen its competitive edge erode. EUR/USD rates added +1.66% while GBP/USD rates gained +1.07%. The decline in US Treasury yields weighed on USD/JPY rates, which slipped by -0.63%.

A Full US Economic Calendar

The turn of the calendar to a new month will bring about the typical flurry of significant data releases over the coming days. Several speeches by Federal Reserve policymakers will also prove influential for markets, given how Fed rate hike expectations have receded recently.

- On Tuesday, May 31, the March US house price index is due at 13 GMT, followed by the May US Conference Board consumer confidence report at 14 GMT.

- On Wednesday, June 1, weekly US MBA mortgage applications figures will be released at 11 GMT. The May US ISM manufacturing PMI will be reported at 14 GMT, as will April US construction spending figures. NY Fed President Williams will give a speech at 15:30 GMT, then St. Louis Fed President Bullard will give remarks at 17 GMT. The Fed’s Beige Book is due out at 18 GMT.

- On Thursday, June 2, the May US ADP employment change report will be released at 12:15 GMT. Shortly thereafter, at 12:30 GMT, weekly US jobless claims figures will be published. April US factory orders are due at 14 GMT. NY Fed Vice President Logan will give a speech at 16 GMT, while Cleveland Fed President Mester will talk at 17 GMT.

- On Friday, June 3, the May US nonfarm payrolls report and US unemployment rate are due at 12:30 GMT. The May US ISM non-manufacturing (services) PMI will be released at 14 GMT. Fed Vice Chair Brainard will give remarks at 14:30 GMT.

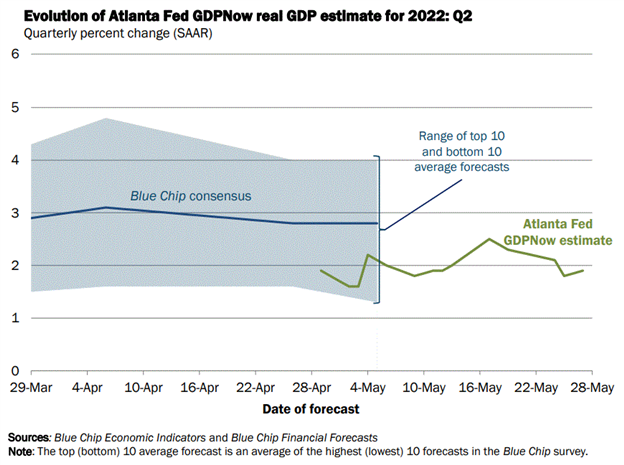

Atlanta Fed GDPNow 2Q’22 Growth Estimate (May 27, 2022) (Chart 1)

Based on the data received thus far about 2Q’22, the Atlanta Fed GDPNow growth forecast is now at +1.9% annualized, up from +1.8% on May 25. The upgrade was due to “an increase in the nowcast of second-quarter real net exports was partially offset by a decrease in the nowcast of second-quarter real gross private domestic investment.” The next update to the 2Q’22 Atlanta Fed GDPNow growth forecast is due on Wednesday, June 1.

For full US economic data forecasts, view the DailyFX economic calendar.

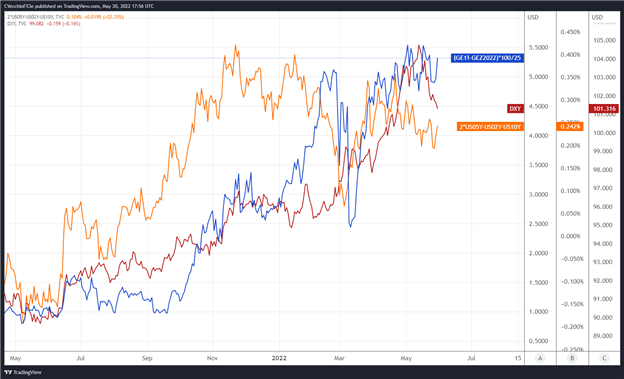

Several Rate Hikes Priced-In, But…

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the May 2022 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (May 2022-December 2022) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Timeframe (May 2021 to May 2022) (Chart 1)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

There are currently five 25-bps rate hikes discounted through the end of 2022; no rate hikes are priced-in for 2023. The 2s5s10s butterfly has narrowed in recent weeks, suggesting that the market interpretation of the near-term path of Fed rate hikes has become less hawkish.

Read more: Central Bank Watch: Fed Speeches, Interest Rate Expectations Update

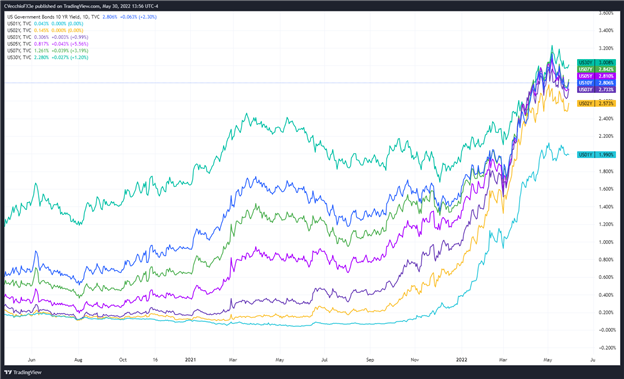

US Treasury Yield Curve (1-year to 30-years) (May 2020 to May 2022) (Chart 3)

The shape of the US Treasury yield curve coupled with declining Fed rate hike odds is acting as a headwind for the US Dollar. While the rebound in US real rates (nominal less inflation expectations) has not abated, other major currencies are seeing their own real rates rise, narrowing the gap that the US Dollar built up over the past few months, eroding the US Dollar’s relative advantage.

While markets are expecting the Fed to raise rates in 50-bps increments in each of the next few meetings, the chasm between expectations among the Fed, European Central Bank, and other central banks is shrinking.

CFTC COT US Dollar Futures Positioning (May 2020 to May 2022) (Chart 4)

Finally, looking at positioning, according to the CFTC’s COT for the week ended May 24, speculators increased their net-long US Dollar positions to 38,003 contracts from 36,179 contracts. US Dollar positioning is now the most net-long since mid-January.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

--- Written by Christopher Vecchio, CFA, Senior Strategist