Fundamental Forecast for the US Dollar: Neutral

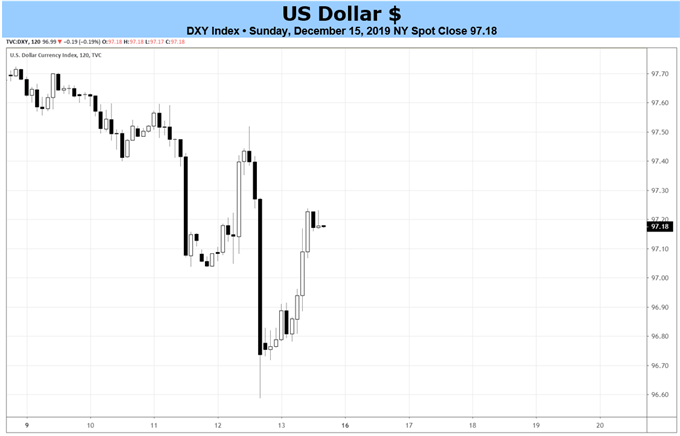

- The US Dollar (via the DXY Index) struggled into the end of the week thanks to a dramatic swing in GBP/USD following the UK general election.

- The forex economic calendar will do little by way of helping the US Dollar in the last full week of the year.

- The IG Client Sentiment Index shows that retail traders are getting long the US Dollar during its decline.

See our long-term forecasts for the US Dollar, Euro, Gold, Crude Oil, and more with the DailyFX Trading Guides.

US Dollar Rates Week in Review

The US Dollar had a rough week, losing ground against six of its seven major counterparts. With the UK general election yielding a resounding majority for UK Prime Minister Boris Johnson, GBP/USD rates climbed by a significant 1.45%. The European currencies in total performed well, with USD/CHF dropping by -0.68% and EUR/USD rallying by 0.55%. Amid a rise in global equity markets, the Japanese Yen was jettisoned in favor of higher yielding currencies; USD/JPY was the lone USD-pair in positive territory, adding 0.73%.

US Economic Calendar Thin in Last Full Week of the Year

It’s the final full week of the year (and the decade): next week will be split in two due to Christmas; the following week will be partitioned thanks to New Years. With federal reporting agencies entering this vacation period, data releases over the coming weeks will be thin at best.

This coming week, there are only two ‘high’ rated US economic releases worth paying attention to, both set to be released on Friday, December 20: the final Q3’19 US GDP report (due in at 2.1% annualized) and the November US PCE Core (the Fed’s preferred gauge of inflation is due in at 1.5% y/y). Neither should move the needle all that much in terms of price action.

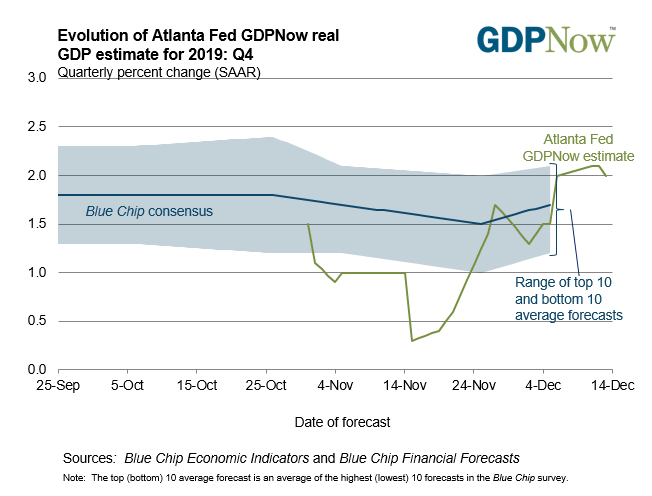

Atlanta Fed GDPNow Q4’19 Growth Estimate (December 16, 2019) (Chart 1)

Based on the data received thus far about Q4’19, the Atlanta Fed GDPNow forecast is looking for growth at 2.0% annualized. Q4’19 US GDP expectations have ranged between 0.3-2.0% since tracking began at the end of October. The next update to the Q4’19 forecast will be released on Tuesday, December 17 following the November US housing starts and industrial production data.

US-China Trade War Phase 1 Talks Finished

The Phase 1 deal of the US-China trade war is complete. What’s in the exact deal remains largely unknown; targets for Chinese purchases of US agricultural products simply don’t make sense mathematically, nor should they be perceived as a victory. Nevertheless, as the US-China trade war albatross is slowly removed from the market’s collective neck, there’s been less of an impetus for the Federal Reserve to aggressively cut interest rates.

Federal Reserve on Hold for a While

Rates markets have evolved in a manner that should be theoretically supportive of a stronger US Dollar: interest rate cut expectations have plummeted as the US-China trade war phase 1 deal came into focus. Yet Fed Chair Jerome Powell made clear that the Fed was very much in a wait-and-see mode.

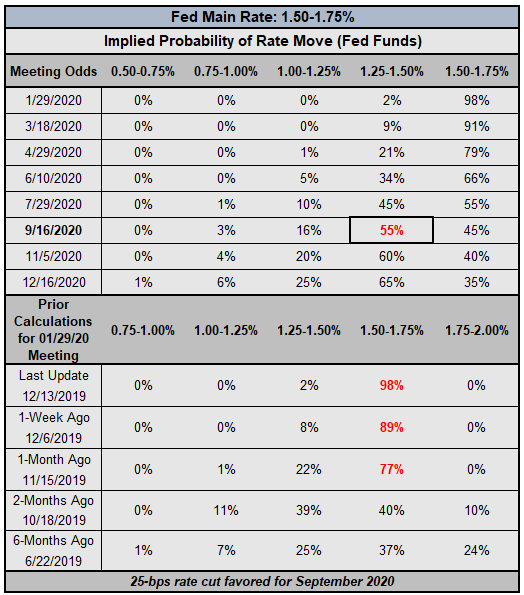

Federal Reserve Rate Expectations (December 16, 2019) (Table 1)

According to Fed funds futures, there is still less than a 10% chance of a 25-bps rate cut by the March 2020 Fed meeting. September 2020 is the first month that sees an implied probability greater than 50%, while a full rate cut is basically discounted by December 2020 (the current effective Fed rate is 1.55%; the forward rate for December 2020 is 1.31%, or -24-bps lower).

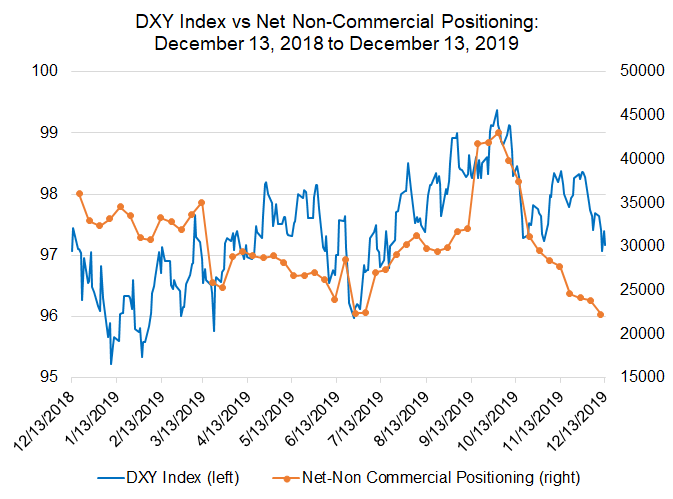

US Dollar Net-Long Futures Positioning Plummets, DXY Index Does Not (Chart 2)

Finally, looking at positioning, according to the CFTC’s COT for the week ended December 10, speculators decreased their net-long US Dollar positions to 22.3K contracts, down from the 23.9K net-long contracts held in the week prior. Net-long US Dollar positioning has dropped meaningfully in recent weeks, down by 48% since the 43K contracts held during the week ended October 1; during this time, the DXY Index fell by -2.25%.

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist

To contact Christopher, email him at cvecchio@dailyfx.com

Follow him in the DailyFX Real Time News feed and Twitter at @CVecchioFX