Fundamental Forecast for the US Dollar: Neutral

- US Dollar ends 7-week losing streak after impressive labor-market data

- Improving service-sector ISM survey data might offer additional support

- RBA, RBNZ and BOE rate decision outcomes likely to be trend-defining

Find out here how recent price moves have matched up with our first-quarter US Dollar forecast !

The US Dollar ended a seven-week losing streak – the longest in over 13 years – to post an advance against its major counterparts. A cautiously hawkish FOMC policy announcement helped cool selling pressure but the bulk of the advance came courtesy of a January’s impressively strong employment data.

The report showed the economy added 200k jobs last month, topping forecasts for a 180k increase. December’s result was also revised higher, pointing to a gain of 160k versus the 148k originally reported. Perhaps most importantly however, wage inflation unexpectedly jumped to 2.9 percent.

The greenback’s rally was tellingly accompanied by a rise in Treasury bond yields and a steepening of the priced-in 2018 rate hike implied in Fed Funds futures. That marks something of a return to form: the currency has been unable to capitalize on a hawkish shift in policy bets since early November.

More interestingly still, news of a stronger than expected US labor market – a seemingly supportive development for domestic and global growth – was accompanied by aggressive risk aversion. In fact, the benchmark S&P 500 stock index accelerated downward after the data crossed the wires.

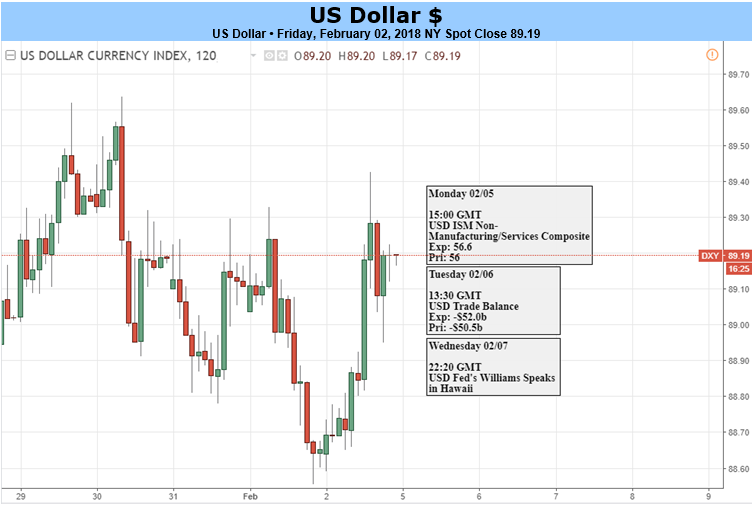

Looking ahead, top tier domestic news flow will be dispensed with early in the week as the service-sector ISM survey cross the wires on Monday. A pickup in the pace of activity growth is projected. If the Dollar is recoupling with the Fed outlook in earnest, that has scope to give it a lift.

The bulk of the week will be spent looking abroad however, with rate decisions from the RBA, the RBNZ and the BOE taking top billing. No changes are expected but traders will be combing the accompanying policy statements for signs of a hawkish tone shift in officials’ forward guidance.

The US currency’s plunge over the past three months has mostly owed to speculation that a broadening pickup in global growth will see top central banks following the Fed’s hawkish lead, eroding its yield advantage. Last month, the BOC, BOJ and ECB all pushed back against this narrative.

If the trio of incoming policy announcements follow suit, the Dollar seems likely to continue higher. In fact, gains may be had not just against the currencies in question, with a broader-based recovery developing as the central thesis driving recent weakness losses its appeal to investors.